Best Personal Accident Insurance in Singapore 2024

Our insurance experts analysed over 100 personal accident insurance policies on the market from 16 different insurers to find the best plans in Singapore based on price and benefits offered. Because the best personal accident plan depends not just on your budget but also whether it matches your lifestyle, our top picks below offer a great combination of value-for-money for a variety of consumers.

- Best Plans for Comprehensive Coverage

- FWD Personal Accident: Great option for people who want to maximise their accident & disease coverage

- Income Personal Assurance: Good fit for families looking for comprehensive disability and childcare coverage

- Cheapest Personal Accident Plan

- Singlife with Aviva Personal Accident Lite: Cheapest PA plan, premiums are 30-37% below industry average

- Personal Accident Plans for Hazardous Occupations

- FWD Personal Accident Insurance: Cheapest plan for individuals working in high-risk occupations; premiums are 27% below average

- Income PA Assurance: Cheapest option for people looking for at least S$1,000,000 of coverage; offers physiotherapy benefit

- Best Personal Accident Plans for Elderly

- FWD Personal Accident: Good option for elderly consumers on a budget; offers elderly-friendly benefits like home modification, physiotherapy & mobility aids

- Tokio Marine TM 365: Best plan for long-term retirement coverage as it lets you renew the plan until you turn 85; S$50,000 coverage plan costs 10% below average

- Best for Personal Transportation Users

- Etiqa eProtect Personal Mobility Insurance: Good option for recreational cyclists; offers damage protection for their bike

- Income Personal Mobility Guard: Good option for bicycle, hoverboard, or electronic skate/scooter riders who use these devices for commuting

- Best Plans for Comprehensive Coverage

- FWD Personal Accident: Great option for people who want to maximise their accident & disease coverage

- Income Personal Assurance: Good fit for families looking for comprehensive disability and childcare coverage

- Cheapest Personal Accident Plan

- Singlife with Aviva Personal Accident Lite: Cheapest PA plan, premiums are 30-37% below industry average

- Personal Accident Plans for Hazardous Occupations

- FWD Personal Accident Insurance: Cheapest plan for individuals working in high-risk occupations; premiums are 27% below average

- Income PA Assurance: Cheapest option for people looking for at least S$1,000,000 of coverage; offers physiotherapy benefit

- Best Personal Accident Plans for Elderly

- FWD Personal Accident: Good option for elderly consumers on a budget; offers elderly-friendly benefits like home modification, physiotherapy & mobility aids

- Tokio Marine TM 365: Best plan for long-term retirement coverage as it lets you renew the plan until you turn 85; S$50,000 coverage plan costs 10% below average

- Best for Personal Transportation Users

- Etiqa eProtect Personal Mobility Insurance: Good option for recreational cyclists; offers damage protection for their bike

- Income Personal Mobility Guard: Good option for bicycle, hoverboard, or electronic skate/scooter riders who use these devices for commuting

What is personal accident insurance?

Personal accident insurance can protect you from large medical expenses if you get into an accident or develop an infectious disease. We found that the best personal accident (PA) plans in Singapore came from insurers such as Singlife with Aviva, FWD, Income and Tokio Marine. These plans proved to not only offer a high value of coverage per dollar of premium, they offered above average coverage and highly competitive premiums. Below, you'll find our analysis of why we chose these plans out of the 70+ options we compared.

Best Personal Accident Plans for Comprehensive Coverage

The personal accident plans below offer the best and most comprehensive set of benefits when it comes to personal accident protection. Whether they offer unique coverage for infectious diseases or comprehensive disability benefits, you'll be well protected with any of these plans.

Best Personal Accident Insurance for Infectious Diseases (Coronavirus & Dengue)

- Region of Coverage

- Worldwide

- Total Disability Coverage

- 100% of Sum Assured

| Benefits | Limits |

|---|---|

| Accidental Death & Disability | S$1,000,000 |

| Medical Expenses | S$15,000 |

| Medical Expenses (Infectious Disease) | S$7,500 |

| Hospital Income | S$500/day |

| Home Modification | S$50,000 |

| Weekly Income | S$500/week |

| Child Support Benefit | S$500,000 |

If you are looking to maximise your personal accident coverage regardless of cost, FWD's Personal Accident plan with S$1 million dollars of accidental death and disability coverage can be a good fit. For instance, the base plan automatically includes ambulance fee, daily taxi allowance, personal liability and a S$500,000 child support benefits. It also offers S$50,000 of home modification coverage—the highest on the market. This is quite unique as other plans make you pay extra to get these benefits. Though it is slightly pricier compared to other PA plans that provide S$1 million worth of coverage, all the extra benefits could very well be worth the price.

FWD's Personal Accident insurance also covers the maximum number of infectious diseases, including COVID-19 and Dengue. By adding the overseas medical expense rider, you'll also get up to S$15,000 of medical coverage for infectious diseases while abroad, which is a great feature for people who have to travel frequently. The COVID-19 benefit additionally provides coverage for for medically necessary expenses in the event of hospitalisations that arise from the vaccination. It is applicable to side effects occuring up to 30-days after each does of the vaccine and the benefit will last until the end of 2021.

- Region of Coverage

- Worldwide

- Total Disability Coverage

- 100% of Sum Assured

| Benefits | Limits |

|---|---|

| Accidental Death & Disability | S$1,000,000 |

| Medical Expenses | S$15,000 |

| Medical Expenses (Infectious Disease) | S$7,500 |

| Hospital Income | S$500/day |

| Home Modification | S$50,000 |

| Weekly Income | S$500/week |

| Child Support Benefit | S$500,000 |

If you are looking to maximise your personal accident coverage regardless of cost, FWD's Personal Accident plan with S$1 million dollars of accidental death and disability coverage can be a good fit. For instance, the base plan automatically includes ambulance fee, daily taxi allowance, personal liability and a S$500,000 child support benefits. It also offers S$50,000 of home modification coverage—the highest on the market. This is quite unique as other plans make you pay extra to get these benefits. Though it is slightly pricier compared to other PA plans that provide S$1 million worth of coverage, all the extra benefits could very well be worth the price.

FWD's Personal Accident insurance also covers the maximum number of infectious diseases, including COVID-19 and Dengue. By adding the overseas medical expense rider, you'll also get up to S$15,000 of medical coverage for infectious diseases while abroad, which is a great feature for people who have to travel frequently. The COVID-19 benefit additionally provides coverage for for medically necessary expenses in the event of hospitalisations that arise from the vaccination. It is applicable to side effects occuring up to 30-days after each does of the vaccine and the benefit will last until the end of 2021.

- Region of Coverage

- Worldwide

- Total Disability Coverage

- Up to 150% of Sum Assured

| Benefits | Limits |

|---|---|

| Accidental Death & Disability | S$1,000,000 |

| Medical Expenses | S$20,000 |

| Hospital Income | S$400/day |

| Home Modification | S$25,000 |

| Weekly Income | S$500/week |

| Child Support Benefit | S$35,000 |

Income's PA Assurance Plan 4 can be a good fit for families looking for comprehensive disability and childcare coverage. It offers S$1 million of accidental death coverage, 150% of the sum assured should you get a total and permanent disability, above average coverage for your child's education should you pass away from your accident, weekly income benefits and a daily hospital income benefit. If you purchased this plan with the infectious disease add-on, you'll also receive COVID-19 coverage, which includes a death benefit and a daily hospitalisation cash benefit. There is no waiting period before you can make COVID-19 related claims, but you should be aware you won't be covered if you purchased the policy after you tested positive.

Furthermore, PA Assurance covers miscarriage, food poisoning and hand, foot and mouth disease (HFMD) and diagnostic tests for broken/fractured bone procedures. It also costs just slightly under the average of other PA plans that offer S$1 million of coverage and offers a 40% discount on premiums for your children, making it a high value plan.

- Region of Coverage

- Worldwide

- Total Disability Coverage

- Up to 150% of Sum Assured

| Benefits | Limits |

|---|---|

| Accidental Death & Disability | S$1,000,000 |

| Medical Expenses | S$20,000 |

| Hospital Income | S$400/day |

| Home Modification | S$25,000 |

| Weekly Income | S$500/week |

| Child Support Benefit | S$35,000 |

Income's PA Assurance Plan 4 can be a good fit for families looking for comprehensive disability and childcare coverage. It offers S$1 million of accidental death coverage, 150% of the sum assured should you get a total and permanent disability, above average coverage for your child's education should you pass away from your accident, weekly income benefits and a daily hospital income benefit. If you purchased this plan with the infectious disease add-on, you'll also receive COVID-19 coverage, which includes a death benefit and a daily hospitalisation cash benefit. There is no waiting period before you can make COVID-19 related claims, but you should be aware you won't be covered if you purchased the policy after you tested positive.

Furthermore, PA Assurance covers miscarriage, food poisoning and hand, foot and mouth disease (HFMD) and diagnostic tests for broken/fractured bone procedures. It also costs just slightly under the average of other PA plans that offer S$1 million of coverage and offers a 40% discount on premiums for your children, making it a high value plan.

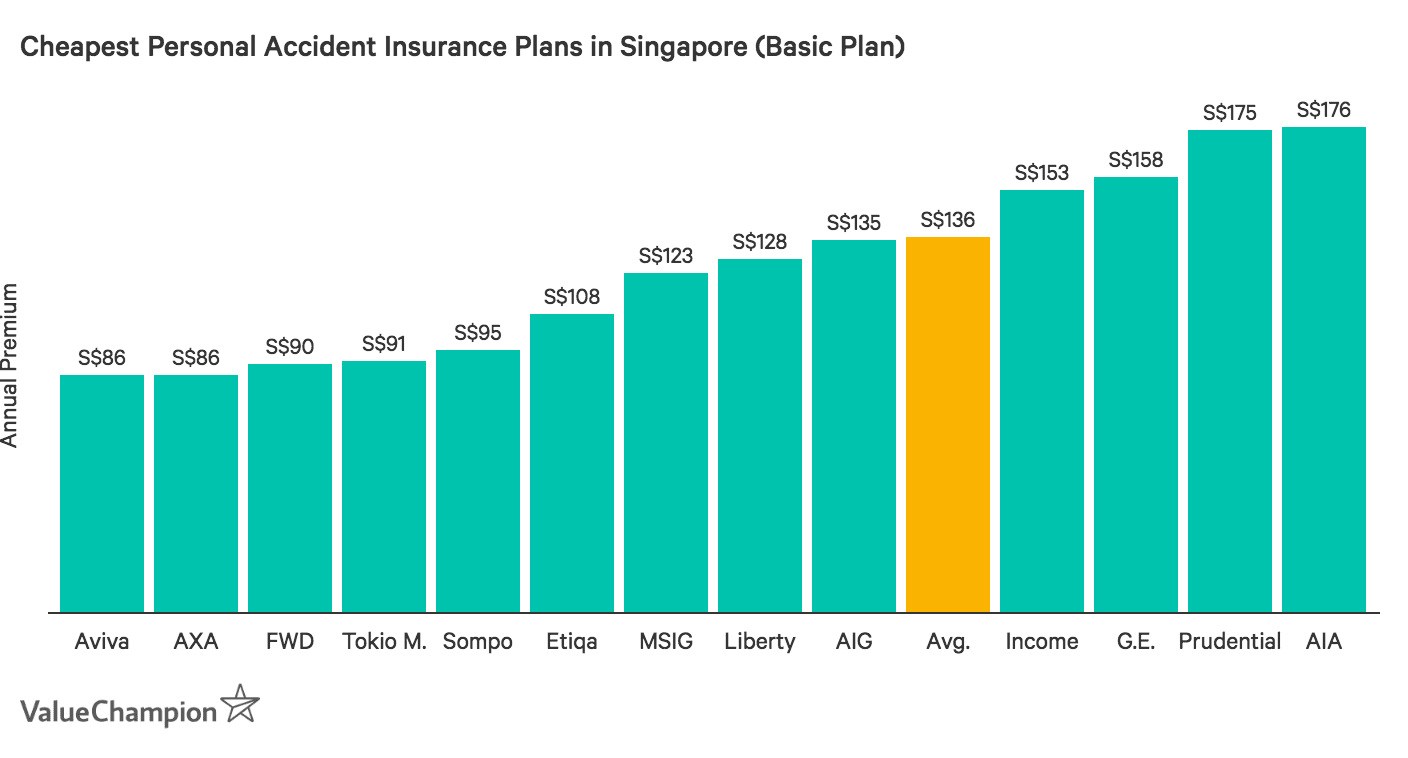

Cheapest Personal Accident Insurance Plan

The personal accident plans below are the most competitively priced. However, while they are cheap, they don't skimp on coverage and will provide you with substantial personal accident benefits.

Cheapest Personal Accident Plan for Accident Coverage

- Region of Coverage

- Worldwide

- Total Disability Coverage

- 100% of Sum Assured

| Benefits | Aviva Lite | Basic Plan Avg. |

|---|---|---|

| Accidental Death & Disability | S$100,000 | S$86,842 |

| Medical Expenses | S$3,000 | S$2,211 |

| Hospital Income | S$50/day | S$61/day |

| Personal Liability | S$100,000 | 83,333 |

| Disability Coverage | 100% of Sum | 100% of Sum |

| Coverage Region | Worldwide | N/A |

One of the cheapest personal accident insurance plans is Singlife Personal Accident Insurance Lite plan, with premiums costing 30% below average for basic personal accident plans. Additionally, its coverage includes S$100,000 of death or disablement coverage and S$3,000 of medical expense coverage, which is significantly higher compared to other basic-tier plans. There is also liability coverage, which can be beneficial if your accident involved another person.

Furthermore, this plan's competitive price means you can top off your coverage by purchasing one of its riders and still end up with premiums that are 20% below average for basic personal accident plans. Due to the low cost and simple coverage, this plan could be a good fit for the average consumer working in a low-risk, skilled or semi-skilled profession.

- Region of Coverage

- Worldwide

- Total Disability Coverage

- 100% of Sum Assured

| Benefits | Aviva Lite | Basic Plan Avg. |

|---|---|---|

| Accidental Death & Disability | S$100,000 | S$86,842 |

| Medical Expenses | S$3,000 | S$2,211 |

| Hospital Income | S$50/day | S$61/day |

| Personal Liability | S$100,000 | 83,333 |

| Disability Coverage | 100% of Sum | 100% of Sum |

| Coverage Region | Worldwide | N/A |

One of the cheapest personal accident insurance plans is Aviva's Personal Accident Lite plan, with premiums costing 30% below average for basic personal accident plans. Additionally, its coverage includes S$100,000 of death or disablement coverage and S$3,000 of medical expense coverage, which is significantly higher compared to other basic-tier plans. There is also liability coverage, which can be beneficial if your accident involved another person.

Furthermore, this plan's competitive price means you can top off your coverage by purchasing one of its riders and still end up with premiums that are 20% below average for basic personal accident plans. Due to the low cost and simple coverage, this plan could be a good fit for the average consumer working in a low-risk, skilled or semi-skilled profession.

Best Personal Accident Plans for Hazardous Occupations

It may be difficult to find a personal accident plan if you work in a risky or heavy machinery-involved occupation (class 4 occupation) since most insurers don't provide coverage for you. These jobs include oil-rigging, police work, firefighting, construction and unskilled labor. However, there are a few personal accident plans that will still allow you to purchase coverage even if you work these occupations. We found FWD and Income to be the best insurers for individuals working in these occupations.

Best High Coverage Personal Accident Insurance for Hazardous Occupations

- Region of Coverage

- Worldwide

- Total Disability Coverage

- Up to 150% of Sum Assured

| Benefits | Plan 4 | Top-Tier Plan Avg. |

|---|---|---|

| Accidental Death & Disability | S$1,000,000 | S$537,500 |

| Medical Expenses | S$20,000 | S$7,975 |

| Hospital Income | S$400/day | S$280/day |

| Mobility Prosthetics/Aids | S$2,000 | S$1,880 |

| Personal Liability | N/A | S$433,333 |

| Disability Coverage | 150% of Sum | 100% of Sum |

| Coverage Region | Worldwide | N/A |

Here is why FWD Personal Accident Plan is the best personal accident plan in Singapore in providing high coverage for hazardous occupations.

While FWD is the cheaper option for individuals working in hazardous occupations who are looking for lower levels of death and disability coverage, Income's PA Assurance Plan 4 becomes the cheapest option if you are looking for coverage of at least S$1,000,000. Out of the 4 plans that offer million dollar coverage for class 4 occupations, Income's Assurance plan costs about 10% less (S$1,900 versus industry average of S$2,105).

Furthermore, it offers a S$5,000 physiotherapy benefit, a weekly income if you suffer temporary disablement and can't work, a daily hospital income that gives you a small daily stipend while you are hospitalised and up to S$25,000 for the purchase mobility or prosthetics aids. One potential drawback is that the Income Assurance plan does not offer liability coverage, meaning you won't be covered for legal liabilities if a third party was involved in your accident.

- Region of Coverage

- Worldwide

- Total Disability Coverage

- Up to 150% of Sum Assured

| Benefits | Plan 4 | Top-Tier Plan Avg. |

|---|---|---|

| Accidental Death & Disability | S$1,000,000 | S$537,500 |

| Medical Expenses | S$20,000 | S$7,975 |

| Hospital Income | S$400/day | S$280/day |

| Mobility Prosthetics/Aids | S$2,000 | S$1,880 |

| Personal Liability | N/A | S$433,333 |

| Disability Coverage | 150% of Sum | 100% of Sum |

| Coverage Region | Worldwide | N/A |

Here is why FWD Personal Accident Plan is the best personal accident plan in Singapore in providing high coverage for hazardous occupations.

While FWD is the cheaper option for individuals working in hazardous occupations who are looking for lower levels of death and disability coverage, Income's PA Assurance Plan 4 becomes the cheapest option if you are looking for coverage of at least S$1,000,000. Out of the 4 plans that offer million dollar coverage for class 4 occupations, Income's Assurance plan costs about 10% less (S$1,900 versus industry average of S$2,105).

Furthermore, it offers a S$5,000 physiotherapy benefit, a weekly income if you suffer temporary disablement and can't work, a daily hospital income that gives you a small daily stipend while you are hospitalised and up to S$25,000 for the purchase mobility or prosthetics aids. One potential drawback is that the Income Assurance plan does not offer liability coverage, meaning you won't be covered for legal liabilities if a third party was involved in your accident.

Best Personal Accident Insurance for the Elderly

As you get older, insurance usually becomes more expensive while the risk of a medical emergency or accident increases. In this case, you may want to forego very expensive private health insurance plans and instead opt for a personal accident plan to fill any gaps in your hospitalisation coverage. For those cases, we found FWD and TokioMarine to provide the best coverage for seniors, provided that they enroll before age 65.

Cheapest Personal Accident Insurance for Seniors

Promotion:

- Region of Coverage

- Worldwide

- Total Disability Coverage

- 100% of Sum Assured

| Benefits | Limits |

|---|---|

| Accidental Death & Disability | S$100,000 |

| Medical Expenses | S$2,000 |

| Daily Hospital Income | N/A |

| Mobility Aids/Prosthetics | S$500 |

| Home Modifications | S$10,000 |

| Max. Age Covered | 75 (policy must be purchased before age 65) |

| Disability Coverage | 100% of Sum |

| Coverage Region | Worldwide |

Here is why FWD Personal Accident Plan is one of best personal accident plan in Singapore for the elderly in terms of affordability.

FWD's Personal Accident plan with S$100,000 of coverage is a good option for consumers on a tight budget. This is because its premiums cost 35% below the basic accident plan average. While it only provides coverage up until age 75, its benefits make it a good option for older consumers looking for post-accident benefits. For instance, its home modification installation, mobility aids/prosthetics and physiotherapy coverage make this plan a good option for seniors who live alone, since home modifications are a costly but necessary endeavour to make mobility easier after an accident.

Promotion:

- Region of Coverage

- Worldwide

- Total Disability Coverage

- 100% of Sum Assured

| Benefits | Limits (100K Plan) |

|---|---|

| Accidental Death & Disability | S$100,000 |

| Medical Expenses | S$2,000 |

| Daily Hospital Income | N/A |

| Mobility Aids/Prosthetics | S$500 |

| Home Modifications | S$10,000 |

| Max. Age Covered | 75 (policy must be purchased before age 65) |

| Disability Coverage | 100% of Sum |

| Coverage Region | Worldwide |

Here is why FWD Personal Accident Plan is one of best personal accident plan in Singapore for the elderly in terms of affordability.

FWD's Personal Accident plan with S$100,000 of coverage is a good option for consumers on a tight budget. This is because its premiums cost 35% below the basic accident plan average. While it only provides coverage up until age 75, its benefits make it a good option for older consumers looking for post-accident benefits. For instance, its home modification installation, mobility aids/prosthetics and physiotherapy coverage make this plan a good option for seniors who live alone, since home modifications are a costly but necessary endeavour to make mobility easier after an accident.

Best Personal Accident Insurance for Long-Term Retirement Coverage

- Region of Coverage

- Worldwide

- Total Disability Coverage

- Up to 150% of Sum Assured

| Benefits | Limits |

|---|---|

| Accidental Death & Disability | S$50,000 |

| Medical Expenses | S$2,000 |

| Daily Hospital Income | S$50/day |

| Mobility Aids/Prosthetics | S$1,500 |

| Home Modifications | S$2,000 |

| Max. Age Covered | 85 |

| Disability Coverage | 150% of Sum |

| Coverage Region | Worldwide |

Here is why Tokio Marine's TM 365 is the one of the best personal accident plan in Singapore for long-term retirement coverage.

On the other hand, Tokio Marine's TM 365 Plan A lets you renew your plan until you turn 85, making it a good option for those who want coverage for a longer period of time. It is one of the cheaper options on the market, costing 10% below average for S$50,000 sum assured PA plans. The TM365 A plan also includes a couple of notable benefits. For instance, it offers trauma support coverage for when you need counseling after your accident.

TM 365 also offers up to 150% of the sum assured for certain types of permanent disability. Lastly, the TM 365 A plan provides a weekly income benefit and daily hospital income income, which can be a beneficial benefit for seniors who are still working and would like a small stipend while hospitalised or temporarily disabled.

- Region of Coverage

- Worldwide

- Total Disability Coverage

- Up to 150% of Sum Assured

| Benefits | Limits |

|---|---|

| Accidental Death & Disability | S$50,000 |

| Medical Expenses | S$2,000 |

| Daily Hospital Income | S$50/day |

| Mobility Aids/Prosthetics | S$1,500 |

| Home Modifications | S$2,000 |

| Max. Age Covered | 85 |

| Disability Coverage | 150% of Sum |

| Coverage Region | Worldwide |

Here is why Tokio Marine's TM 365 is the one of the best personal accident plan in Singapore for long-term retirement coverage.

On the other hand, Tokio Marine's TM 365 Plan A lets you renew your plan until you turn 85, making it a good option for those who want coverage for a longer period of time. It is one of the cheaper options on the market, costing 10% below average for S$50,000 sum assured PA plans. The TM365 A plan also includes a couple of notable benefits. For instance, it offers trauma support coverage for when you need counseling after your accident.

TM 365 also offers up to 150% of the sum assured for certain types of permanent disability. Lastly, the TM 365 A plan provides a weekly income benefit and daily hospital income income, which can be a beneficial benefit for seniors who are still working and would like a small stipend while hospitalised or temporarily disabled.

Best Personal Accident Insurance for Personal Transport Users

- Region of Coverage

- Singapore

- Total Disability Coverage

- 100% of Sum Assured

| Benefits | Limits |

|---|---|

| Accidental Death & Disability | S$200,000 |

| Medical Expenses | S$2,500 (S$100 Excess) |

| Personal Liability | S$1,000,000 |

| Disability Coverage | 100% of Sum |

| Region of Coverage | Singapore |

Here is why NTUC Income Personal Mobility Guard Insurance is one of the best personal accident plan in Singapore for personal transport users.

Income's Personal Mobility Guard plan can be a good option for bicycle, hoverboard or electric skate-scooter riders who want tailored protection for them and their two-wheeled vehicles. It offers S$200,000 of personal accident coverage and S$2,500 for medical expenses due to the accident. It also offers up to S$1,000,000 of personal liability coverage, should your accident involve a third party.

However, unlike other personal accident plans it doesn't offer miscellaneous benefits such as a weekly income benefit (payment while you're out of work) or mobility aids/prosthetic benefits. Furthermore, it is important to mention that this plan does not cover injuries not related to you riding your bicycle or personal mobility device, nor does it cover motorcycles. Nonetheless, it can still be beneficial for consumers who utilise their bike or electric scooter for daily commuting.

- Region of Coverage

- Singapore

- Total Disability Coverage

- 100% of Sum Assured

| Benefits | Limits |

|---|---|

| Accidental Death & Disability | S$200,000 |

| Medical Expenses | S$2,500 (S$100 Excess) |

| Personal Liability | S$1,000,000 |

| Disability Coverage | 100% of Sum |

| Region of Coverage | Singapore |

Here is why NTUC Income Personal Mobility Guard Insurance is one of the best personal accident plan in Singapore for personal transport users.

Income's Personal Mobility Guard plan can be a good option for bicycle, hoverboard or electric skate-scooter riders who want tailored protection for them and their two-wheeled vehicles. It offers S$200,000 of personal accident coverage and S$2,500 for medical expenses due to the accident. It also offers up to S$1,000,000 of personal liability coverage, should your accident involve a third party.

However, unlike other personal accident plans it doesn't offer miscellaneous benefits such as a weekly income benefit (payment while you're out of work) or mobility aids/prosthetic benefits. Furthermore, it is important to mention that this plan does not cover injuries not related to you riding your bicycle or personal mobility device, nor does it cover motorcycles. Nonetheless, it can still be beneficial for consumers who utilise their bike or electric scooter for daily commuting.

What Is Personal Accident Insurance?

The best personal accident insurance can protect you from large medical expenses if you get into an accident or develop an infectious disease. In the case of death, a PA insurance plan will provide a lump sum payout to the insured's beneficiaries.

What Does Personal Accident Insurance Cover?

Personal accident insurance are optional plans that can be bought alongside your general health insurance plan to extend your range of coverage. A PA plan will cover the following:

- Temporary or Permanent Disability (TPD): A PA plan provides a lump sum payout to you and your family in the case that you are disabled by an accident. This can help offset the high costs of treatment and rehabilitation, as well as provide a financial safety net for your family in the case that you were the main breadwinner of the household.

- Death: If you die from an accident, your beneficiaries will receive a lump sum payout. This payout is an added benefit to any other types of plans that you have, like a life insurance or endowment plan.

- Infectious Disease: Many personal accident plans include coverage for medical expenses incurred from infectious disease like Dengue Fever and COVID-19. With some providers, you can add an additional overseas rider that covers you in the case that you contract an illness outside of your country of residence.

Do I Need Personal Accident Insurance?

Personal accident insurance acts as an extra layer of financial protection against accidents and disease. While your general health insurance plan may cover basic medical expenses, it does not provide a lump sum payout in the case of death or disability.

You may then ask: do I need a personal accident plan if I already have a life insurance plan? While a life insurance plan does provide a lump sum payout in case of death, they are designed to cover natural deaths, not accidental deaths. Thus, if your work or hobbies are on the riskier side, then it might be a good idea to consider buying a personal accident plan to protect you and your family.

How to Choose the Best Personal Accident Plan

Personal Accident Insurance is an optional insurance plan, which means you should only purchase it if you believe you will truly benefit from the coverage it offers, and you will be able to afford the annual premiums. With that being said, choosing the right plan depends on several factors including your occupation, your desired benefits and your budget.

First, your occupation plays a key role in choosing the best personal accident insurance plan. For instance, if you are the average office worker and the sole provider for your family, you may want to look for plans that have a weekly income benefit and a child support benefit in order to keep your children financially protected. Luckily, because all plans cover this occupation, you will have the most choice, and it will be slightly easier to find a plan based on your budget and desired coverage. On the other hand, retirees who have a higher risk of slips and falls should look for plans that provide coverage well after age 65 and that offer post-accident recovery benefits such as home modifications and mobility aid coverage.

Furthermore, you should carefully read what occupations fall under which category for different insurers because they are not standardised across all insurers. For instance, one insurer may consider a nurse as a Class 3 occupation, while another may consider a nurse to be a Class 2 occupation, resulting in an average annual premium difference of around S$200. However, if you have a class 4 occupation (e.g. police officer, construction worker, paramedic and other occupations that are hazardous or require use of heavy machinery) you first need to find plans that will provide you suitable coverage. This is because we found that most plans do not offer coverage for these types of occupations, making it less likely to have a wide range of options to pick from.

Lastly, it is important to consider your coverage needs and budget regardless of your occupation. You should carefully review your current coverage to see if a personal accident plan would add new coverage or simply act as an expensive duplicate. If you find that most of the coverage would be a duplicate, it may be worth skipping it. However, should you really need the coverage a PA plan provides, you should consider whether you can afford to pay for the plan. In some cases, you may have to sacrifice the amount of coverage you want for a simpler, but more budget-friendly alternative. This means you should carefully compare multiple personal accident insurance plans in Singapore to see which one offers the coverage you need for the price you can afford.

Frequently Asked Questions

If you are interested in learning more about personal accident insurance in Singapore, check out some frequently asked questions below.

Yes, some of the best personal accident insurance policies cover overseas bills. In fact, most policies have global coverage, meaning that no matter where you are located, you are covered by your insurance policy. Some policies, however, have a limit to the amount of days that an individual can be outside of the country before the coverage expires.

All premiums that you pay for your personal accident insurance are tax deductible. According to the IRAS, an individual is allowed to claim their insurance premiums on their taxes as long as those costs are paid out of pocket by that individual.

No, having a personal accident insurance policy is not mandatory in Singapore . However, it is recommended to have a policy as it can help reduce the out of pocket costs that come from an unexpected injury or death. More specifically, personal accident insurance can be useful for people who participate in a lot of sports or don't have worker's compensation coverage.

Most personal accident insurance policies do not cover heart attacks, as they are deemed a type of sickness rather than a type of accident. However, there are certain circumstances in which a heart attack would qualify. More specifically, some insurers may cover a heart attack if it is caused by an accidental injury.

Methodology

To get to our decision, we analysed over 100 personal accident policies on the market from 16 different insurers. We took into consideration the benefits offered, the premiums for each occupation class and any miscellaneous benefits consumers would find to be a valuable addition to their coverage. We then looked at the ratio of benefits offered per dollar premium paid. This helped us see which plans would give consumer the best value. Next, we tried to segment plans based on the demographics they would fit best. For instance, knowing that seniors are mostly retired and have a limited income, we looked at plans that not only provide benefits seniors would need such as mobility coverage and home modifications, but that are also affordable.

| Insurance Companies Sampled | |||

|---|---|---|---|

| Income | FWD | Aviva | Etiqa |

| AXA | Sompo | MSIG | AIG |

| Tokio Marine | Prudential | AIA | Great Eastern |

| China Taiping | India International Insurance | Ergo | Liberty Insurance |

Protected up to specified limits by SDIC. This is only product information provided. You may wish to seek advice from a qualified adviser before buying the product. If you choose not to seek advice from a qualified adviser, you should consider whether the product is suitable for you. Buying an insurance product that is not suitable for you may impact your ability to finance your future financial needs. If you decide that the policy is not suitable after purchasing the policy, you may terminate the policy in accordance with the free-look provision, if any, and the insurer may recover from you any expense incurred by the insurer in underwriting the policy.

Read More:

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.