Car Insurance Discounts: Top Ways You Can Save on Your Auto Insurance

Get the Best Car Insurance in Singapore

Car insurance is a necessary evil: we know we need it, but we sure don't enjoy paying for it. Fortunately, there are many ways you can get discounts on your premium. We've compiled a list of the main ways you can save big on your car insurance to make sure those payments are as painless as possible.

Table of Contents

- Third-Party Only Plans and Third Party, Fire & Theft Plans

- No-Claim Discount

- Certificate of Merit

- Off-Peak License Plate

- Other Discounts

Major Types of Car Insurance Discounts

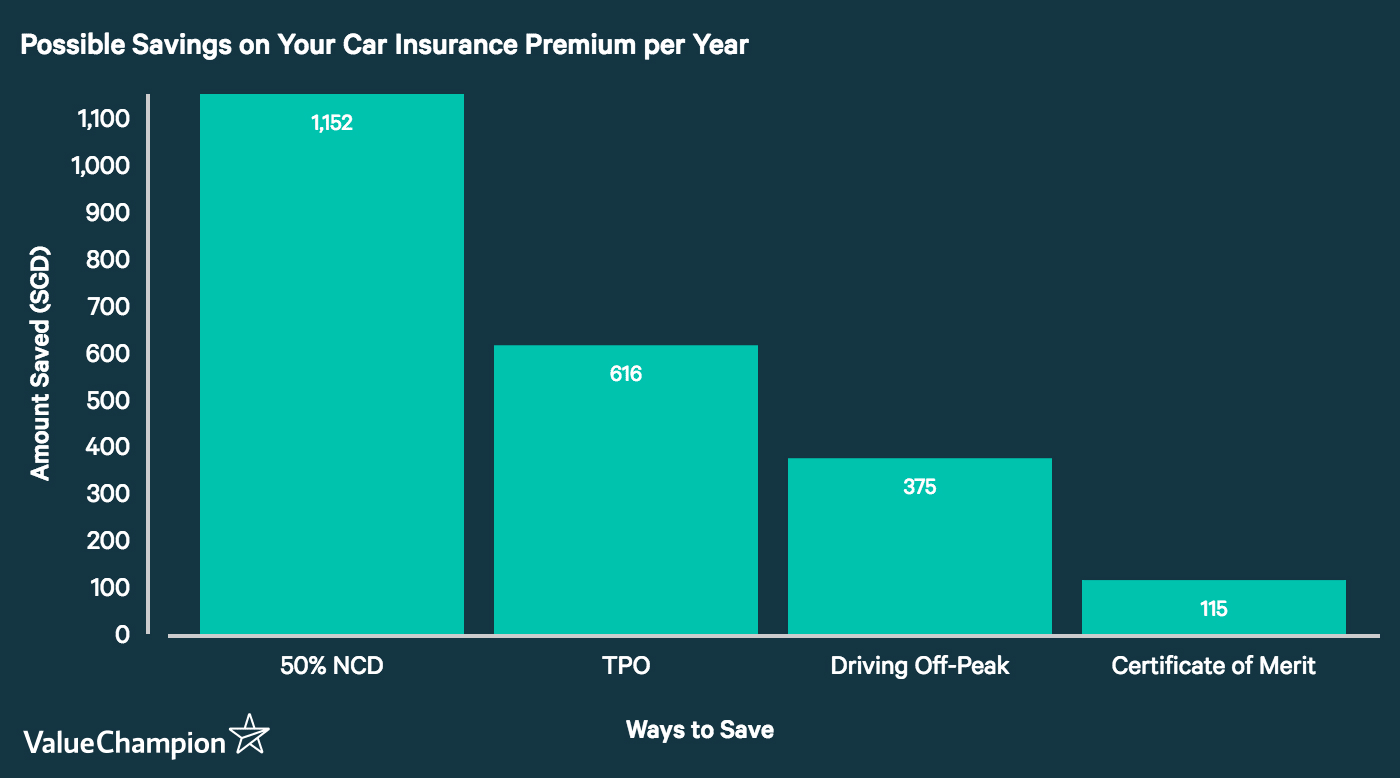

There are four main ways of substantially decreasing the amount you owe on your car insurance beyond taking advantage of promotions: buying a Third Party Only policy, maximising your No-Claim Discount, obtaining a Certificate of Merit from the Singapore Traffic Police, or registering your car as off-peak. The following graph shows approximately how much you may be able to save on your car insurance for each method. The dollar amount in savings reflects the driver profile of an unmarried 30-year-old male with 2 years' driving experience. Without any of the below options, he would be paying a premium of S$2,304 per year.

Third Party Only Plans (TPO) and Third Party, Fire and Theft Plans (TPFT)

The first decision you'll need to make when buying car insurance is which kind of plan you should get: Third Party Only (TPO); Third Party, Fire and Theft (TPFT); or Comprehensive. Each type of plan offers a different level of coverage, and are priced to reflect that. Depending on your needs, your level of comfort with risk, and the vehicle you are planning to insure, you may be able to save on your car insurance by buying a cheaper type of plan. Keep in mind that your insurance plan only comes into play when you are deemed to be at fault for an accident; if you aren't, the other party's insurance must pay for costs incurred.

Comprehensive Plans

Comprehensive plans have the widest coverage, and are therefore the most expensive. Though they're the most expensive, comprehensive insurance policies are actually the most common type of car insurance plan in Singapore: most people usually can't buy cars without a car loan thanks to the costliness of vehicles, and car loans typically require comprehensive plans. Comprehensive plans include coverage for loss or damage to your vehicle up to the market value of your car at the time of the crash, coverage for medical expenses, personal accident benefits, windscreen damage, and towing.

TPFT Plans (30% Cheaper)

The Third Party, Fire and Theft (TPFT) plan is the second-cheapest type of car insurance. It insures you for any liability against a third party (property damage or death or injury to other parties), as well as any accidental damage to your car resulting from fire or theft. However, like the TPO plan, it does not generally include coverage of loss or damage to your vehicle, windscreen damage, medical expenses, personal accident benefits, loss of use, car accessories, etc. As such, it is more expensive than the TPO plan, but less expensive than the more expansive Comprehensive plan. TPFT policies can be a good option for owners of older cars whose market value has significantly depreciated, as this type of policy will enable them to pay a lower premium more proportional to the remaining value of the car.

TPO Plans (40% Cheaper)

The cheapest option of these three is the TPO plan. It covers you only for any liability against a third party (i.e., anybody who's not you), meaning it will only cover the cost of any death or injury that occurs to the third party as a result of the accident, as well as any damage done to a third party's property. It also means that you would have to pay yourself out of pocket for any damage done to your vehicle for any reason (accident, fire, theft, flood, etc.) or any medical expenses you might have due to an accident. As the minimum amount of coverage you require to be legally permitted to drive your vehicle, TPO plans are the cheapest and the riskiest. If you are still financing your car, however, you usually cannot insure it with this kind of plan.

No-Claim Discount (10-50%)

A No-Claim Discount, or NCD, is a discount on your car insurance premium that you can earn for consecutive years of safe driving that could save you as much as 50% on your car insurance. For each year that you drive without making a claim, you earn a 10% discount when you renew your insurance policy up to a cap of 50%. So after 1 year of having car insurance without having to file a claim, you have an NCD of 10%. At 5+ consecutive years without getting into an accident, your NCD would be 50%, meaning your premium would be cut in half. Clearly, driving safe can pay huge dividends.

Fortunately, your NCD will not automatically drop to 0% if you do get into an accident and have to make a claim. First, it depends on how much responsibility you are objectively judged to bear for the accident, as determined by the Barometer of Liability Agreement (BOLA). As long as you are determined to bear 20% or less of the responsibility for an accident, nothing will happen to your NCD. But if your liability is determined to be over 20%, your NCD may drop by as much as 30%. If you were to make two claims in one year, it would drop to 0%. Singlife with Aviva is one exception to this general market-wide practice, as it will reduce your NCD by only 10% for each claim.

Secondly, some car insurance policies offer the option to add an NCD Protector feature, which protects your NCD from dropping at all when you make a claim. The NCD Protector usually costs an additional 10% on your premium, and generally will only apply to the first claim made within a year. But there are exceptions: FWD, a relatively new insurer in the market, will protect your NCD for life if you have a 50% NCD, even if you have multiple accidents in one year.

If you get a new car or switch to a different insurance company, you can transfer your NCD. It cannot, however, be applied to two vehicles at the same time. So if you buy an additional car, that second car's NCD will start at 0%. You should note that if you don't own a car for more than 12 months, your NCD will reset back to 0% and you'll have to build it back up again over time.

Certificate of Merit (5%)

If you are an especially safe driver, you may also qualify for a Certificate of Merit (COM) from the Singapore Traffic Police, which will entitle you to an extra 5% discount on your car insurance premium from participating insurers on top of your NCD. To apply, you just have to maintain a continuous demerit-point-free driving record for 3 continuous years. You can be assigned demerit points for a wide variety of minor to major traffic violations such as failing to wear a seatbelt, exceeding the speed limit, failing to respect right-of-way, crossing double white lines, running red lights, etc.

If you are eligible for the COM, it's a very simple process to obtain one. All you have to do is log in to EDDIES (the Electronic Driver Data Information and Enquiry System) through either the eCitizen website or the Singapore Police Force's website with your NRIC/FIN or SingPass. EDDIES will generate the COM automatically. If your insurance company participates, it can log on to EDDIES itself to verify that you've received it. The following table lists participating insurers as shown on EDDIES.

| Participating Insurers in Certificate of Merit Discounts | ||||

|---|---|---|---|---|

| AXA | Budget Direct | Singlife with Aviva | ||

| Etiqa | FWD | Sompo | ||

| HL Assurance | Liberty Insurance | MSIG | ||

Off-Peak License Plate (25%)

If you don't need to use your car to get to work and can agree not to drive it during the busiest hours of the day, you can save big on your car insurance premiums by registering your car as off-peak. We calculated that all else being equal, an 45-year-old male driver registering his vehicle as off-peak received premiums 25% cheaper on average than he would otherwise. Off-peak drivers can also receive a rebate of up to S$17,000 and a S$500 discount on the annual road tax (subject to a minimum road tax of S$70 per year).

As to be expected, off-peak drivers, who identify themselves by wearing red license plates on their vehicles, face fairly strict constraints on the extent of their driving. They cannot drive their cars from 7 am to 7 pm on weekdays unless they get a special electronic Day License (e-Day license) to drive during those hours. Under the Revised Off-Peak Car (ROPC) Scheme, which applies to cars registered or converted into the scheme since January 25, 2010, there are no restrictions on driving on weekends and religious or public holidays. While cars under the old Off-Peak (OPC) or Weekend Car (WEC) Scheme cannot be driven on Saturdays and some religious holidays from 7 am to 3 pm, they can easily be converted into the newer ROPC system.

Other Discounts

We've detailed the major ways you can cut a hefty chunk out of your car insurance premium. However, you should also keep your eyes out for smaller discounts and promotions that individual insurers may offer. For example:

- By "going green" and receiving all policy documents through email, Singlife with Aviva will discount your premium by S$25 and DirectAsia will discount your premium by S$15 plus GST.

- Etiqa is currently running a "TGIF" promotion that will discount your premium if you buy it on Friday..

- AIG offers "age condition" discounts, which increase for drivers who qualify as being 30 and up, 35 and up, and 40 and up.

- AXA will discount your premium if you agree to double your standard and windscreen excesses.

- Some companies will discount your premium if you "bundle" your car insurance purchase with purchasing affiliated insurance plans. For instance, Singlife with Aviva will discount your premium by 15% if you purchase MINDEF and MHA Group Insurance as well and Income will give you a 5% discount if you are an existing customer.

- If you don't put a lot of miles on your car, you may be able to save even more by purchasing a low-mileage plan. NTUC Income and DirectAsia are two examples of companies that offer this kind of policy.

- Some insurers run promotional discounts around holidays or other special occasions. For example, FWD ran a discount of up to 30% for International Women's Day.