Exploring Singapore’s Real Estate Market - 2017

Find the Cheapest Home Loans in Singapore

Here is the problem in simple terms: the human population is growing exponentially while land is in limited supply. Any market that has significantly higher demand than supply experiences price inflation. This principal of economics is at the core of the explosion in real estate prices in Singapore during the modern era.

Singapore, in many ways, is an extreme case of demand for land outpacing the supply. In a city-state of just 719 square kilometers, land has always been a valued commodity. With a population of 5.4 people now inhabiting these 719 square kilometers, Singapore is the 29th most densely populated city in the world. Adding to the simple desire of Singaporeans to own real estate has been significant interest from foreign investors.

We will take a historic look at real estate values in Singapore and explain several new developments which every consumer should be aware of.

A Look Back – A Surging Market

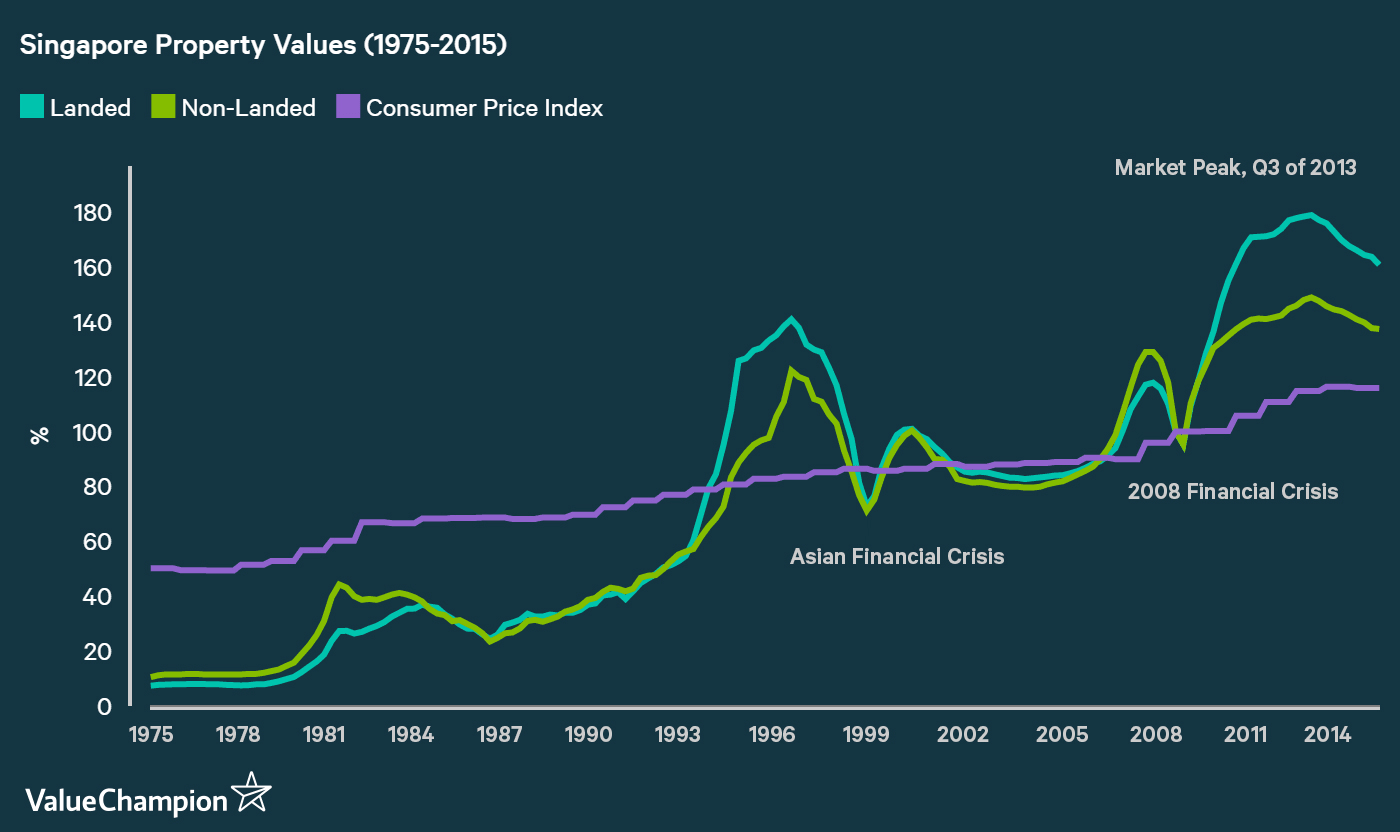

The chart below shows an index of real estate values in Singapore from 1975 to 2016. This index uses 2009 prices as the “base year”, meaning that the average price in 2009 is shown as 100 on the chart. In 1992, when the index was valued at 50, this means that prices were half of prices in 2009. When the index reached 180 in 2013, real estate values were 180% of 2009 values.

What is clear from looking at the chart is these property values are impacted by economic boom and bust cycles. When the global economy is surging higher – real estate values in Singapore are as well. When the global economy is in crises, real estate values in Singapore collapse. This is because Singapore real estate’s demand is heavily influenced by investor appetite. During booms, investor mania drives up the real estate prices. During busts, the excess demand from investors disappears as they tighten their wallets while their investments are declining in value. In the recent years, Singapore’s real estate market has seen significant volatility. During the 2008 financial crises, landed real estate values dropped by 17.6%. As the global recovery was underway, however, property prices again increased by 87.7%. With Singapore’s real estate prices reaching record highs in 2013, the government has been enacting measures to slow down growth and help provide a “soft landing” to current prices.

The Current Market

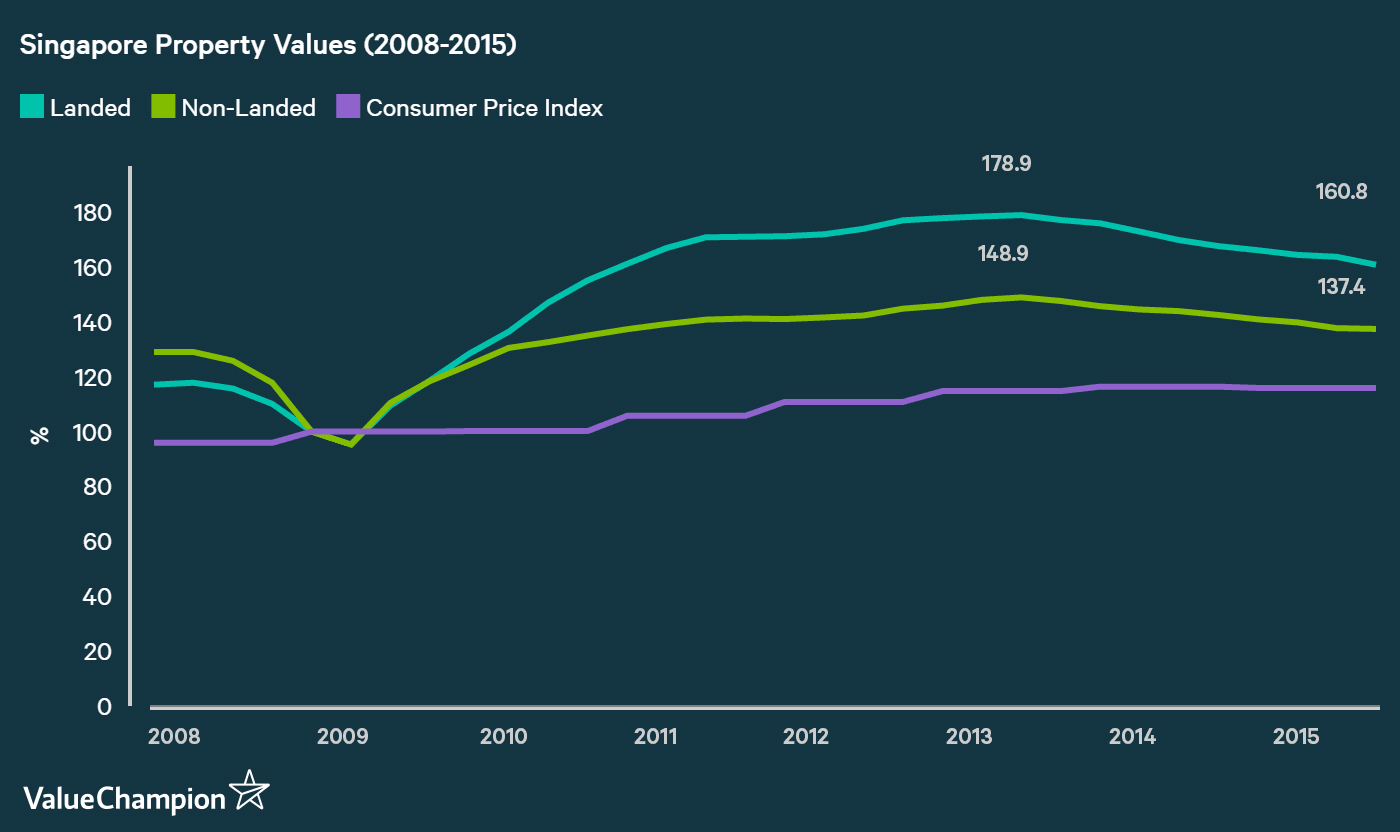

Since reaching a peak in the third quarter of 2013, real estate values within Singapore have been on the decline. This represents the longest continual slide in real estate prices in Singapore, with landed and non-landed property values down 10% and 8% respectively over the last 13 consecutive quarters. This has resulted in a slowdown of growth in mortgage loans for Singaporean households.

In many ways, this is a good thing. As discussed previously, the Singapore real estate market was heavily impacted by the Asian Financial Crises of the late 1990’s and again in the 2008 Financial Crises. With property prices nearly doubling since 2009, many observers have been concerned that the real estate market in Singapore is forming a bubble. If the government can enact measures that gradually rein in real estate prices – rather than cause a collapse in real estate prices – it could help both investors and home owners by providing some stability in their balance sheets.

For context of a collapsing real estate market, just look at the United States during the 2008 decline. During this time period the Case-Shiller Home Price Index, which tracts real estate values, declined by more than 32%. The majority of home owners did not see this decline coming, and as a result were quickly in a position where the resale value of their home was significantly less than their mortgage value. When this happens, selling a property can still leave a homeowner with substantial debt. This is a worst-case scenario, and one which can be avoided if prices can decline slowly.

Government Actions – What Consumers Should Know

The government has enacted several measures or “property cubs” in recent years in an effort to cool down real estate prices. Some of the most impactful and important curbs are listed below:

- Debt repayment costs may not exceed 60% of a borrower’s monthly income

This means that if a consumer earns SGD 10,000 each month, the interest payment on a home loan may not exceed SGD 6,000 per month. While the interest rate of home loans in Singapore is largely influenced by SIBOR and SOR interest rates, the total interest payment is also impacted by how much money one borrows. By limiting the latter factor, this policy is meant to reduce people's ability to buy multiple properties by borrowing money to speculate on market trends.

This measure, established in June 2013, has slowed the number of home loans being taken out and helps prevent consumers from taking loans which they cannot afford to pay back. The effectiveness of this policy is apparent in the aforementioned decline in real estate prices that has been ongoing for the last 13 quarters since 2013.

- Higher stamp duties on purchased properties

When a buyer takes possession of a property, they are now required to pay higher stamp duties (taxes) on this purchase. The current table for calculating this stamp duty is shown below.

| Purchase Price or Market Value (whichever is higher) | Buyer's Stamp Duty |

|---|---|

| First S$180,000 | 1% |

| Next S$180,000 | 2% |

| Remaining Amount | 3% |

This means that a $500,000 property, the buyer immediately owes the government $9,600 in stamp duties. The overall effect of this policy is to discourage new home purchases, especially expensive homes, and lower prices.

- Higher stamp duties for short-term holders of property

For the average consumer, buying a home is a long-term decision. However, property investors or speculators purchase properties in order to “flip it” in just two or three years. To discourage short-term buyers of property, the government has enacted several seller stamp duties (taxes) which only impact sellers who hold a property for less than four years.

The following table shows how this seller duty varies by the number of years a property is held for.

| Real Estate Holding Period | Seller's Stamp Duty |

|---|---|

| Up to 1 Year | 16% |

| 1-2 Years | 12% |

| 2-3 Years | 8% |

| 3-4 Years | 4% |

| +4 Years | 0% |

Final Thoughts

Singapore’s government has taken a number of steps to slow down the rapid growth of the real estate market in recent years. Overall, these measures have been very successful. Many observers expect real estate prices to continue lower into 2017, as the government has been unwilling to budge on these recent measures. If prices can continue decline, it may make home purchase more affordable for young professionals or families who are looking for their first home, and may even create a great buying opportunity as an investment if prices become low enough

Disclosure: The information in this article has been taken from IRAS.GOV.SG and is provided as a resource. This information should not be construed as legal or tax advice. Before making any property or tax decision – please consult an attorney or tax professional.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.