HDB Resale Prices Had the Highest Quarterly Increase in 9 Years: What This Means for Homebuyers

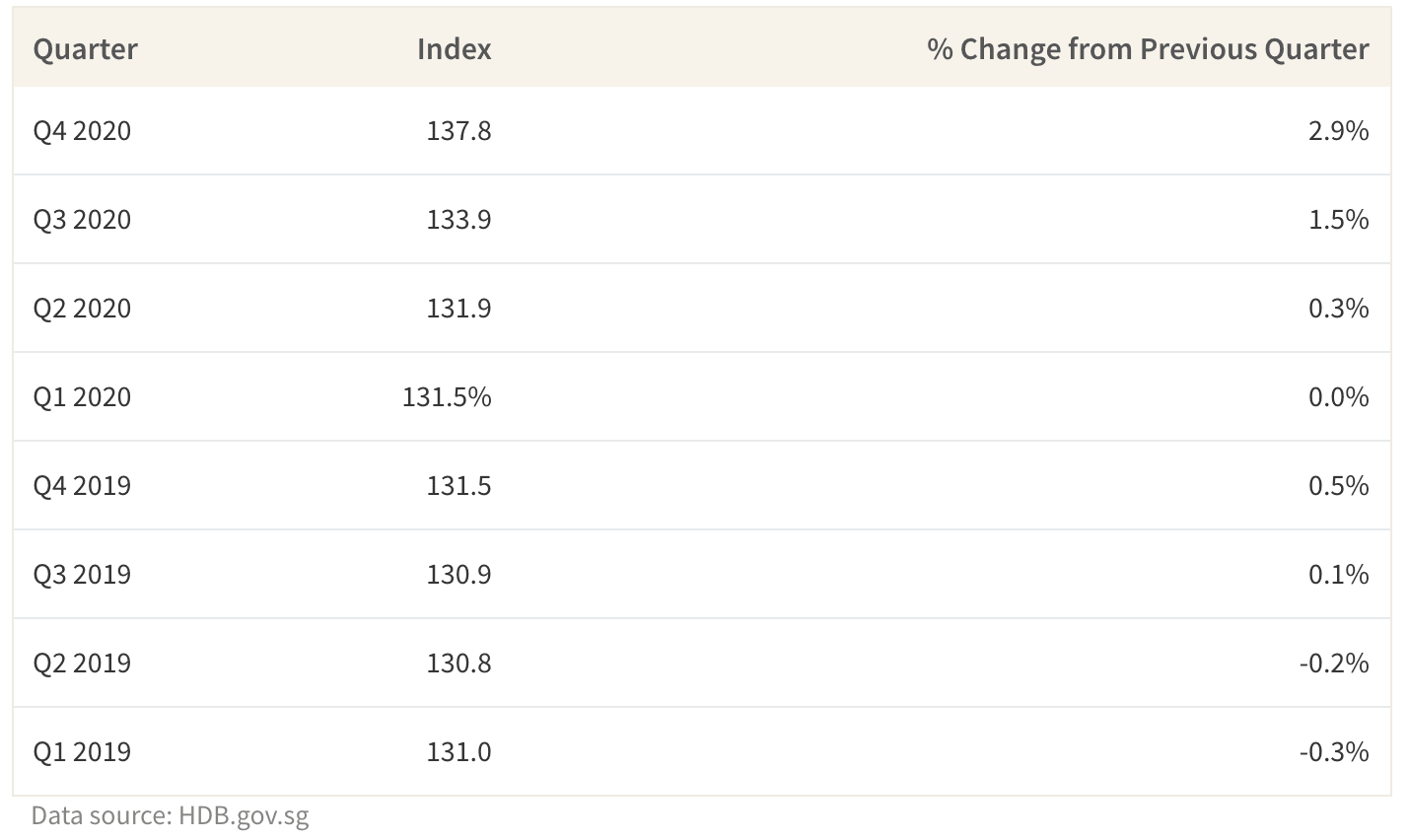

Despite the financial recession brought on by Covid-19 HDB Resale property prices have seen surprising increases in the second half of 2020, with estimated Q4 price increases projected to be one of the highest in almost a decade. However, while HDB resale prices climbed 4.8% in 2020, Singaporeans were still reeling from the financial after effects of COVID-19 and many put their long-term buying and selling plans on hold. So how can we reconcile the stark contrast between the healthy real estate market and a hesitant population? With housing prices predicted to continue increasing into 2021, we discuss what hopeful and current homeowners should consider before buying or selling a property this year.

Resale Price Index for 2020

With HDB Costs Rising Rapidly, How Can You Save When Buying a Home? Home?

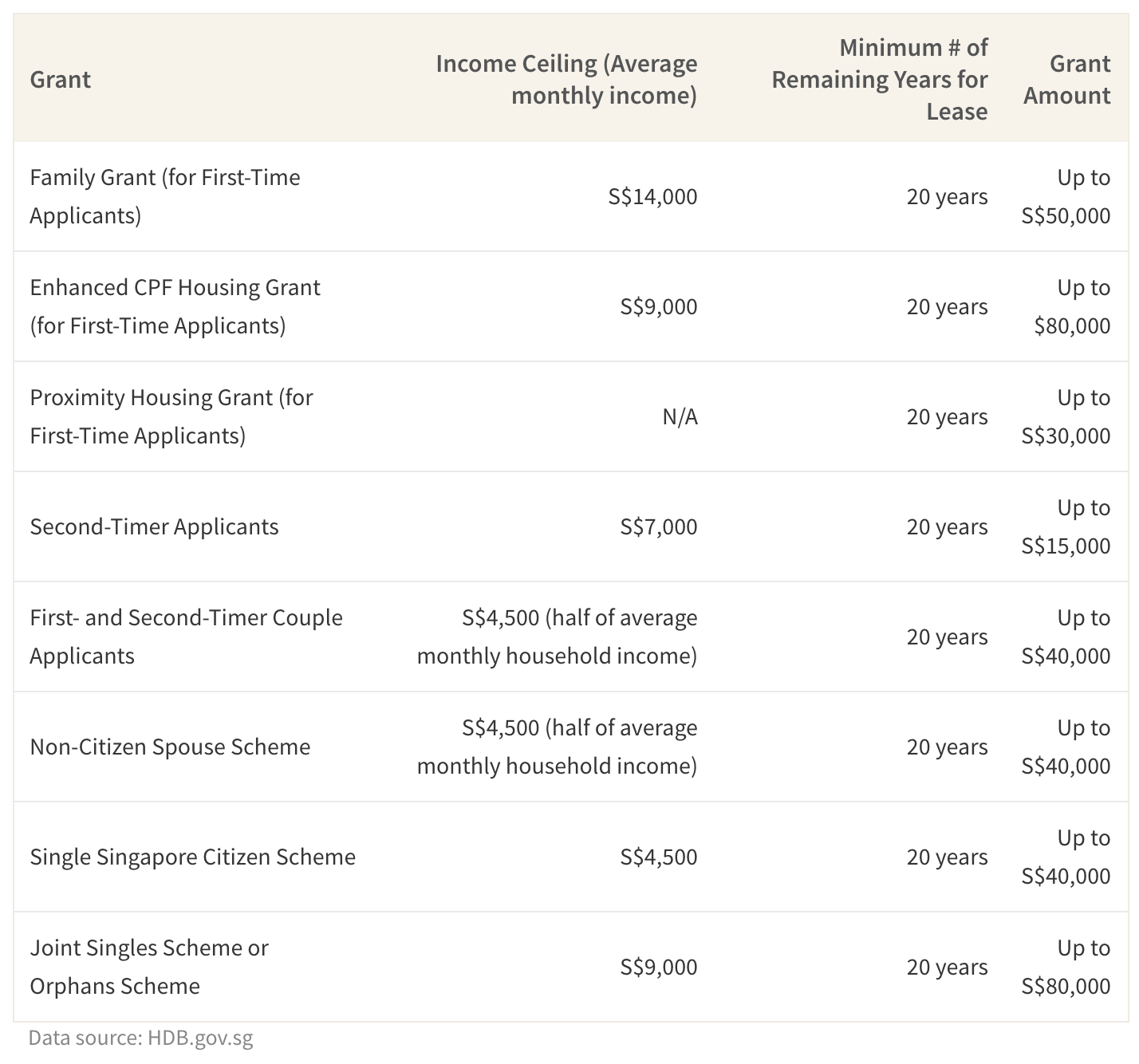

Despite HDB housing price increases, there are still plenty of ways to afford HDB Resale flats. For instance, first-time home buyers can get up to S$160,000 in grants, which is around 22-47% of the cost of a typical 4-room HDB. This cash will be deposited to your CPF Ordinary account and you will be able to use it to offset the flat's initial purchase or to reduce the housing loan amount. However, you should note that if you sell your flat, you will need to return that grant money (with interest included) back into your CPF account.

CPF Housing Grants for HDB Flats

If you can't afford to pay for your flat in cash and you aren't eligible for substantial grants, then you will need to take out a mortgage. You should be aware that most home loans typically have lock-in periods from 0-3 years and charge either floating or fixed interest rates. Depending on which loan you get, the interest rates will be decided either by the bank's board of directors or the Singapore's Interbank Offered Rate (SIBOR). There are advantages and disadvantages to having your interest rates determined by each, so it's advisable to compare different home loans prior to choosing the one which will charge you the least amount.

What if Prices Increased Past Your Budget?

Even an incremental price increase of 3% on a S$339,000 (the lower end median price of a 4-room HDB flat) results in a S$10,170 increase in the overall flat price. If 2020's price increases have put previously affordable properties out of reach, then, you may have to compromise on a smaller home or different neighborhood or wait and see until better deals hit the market. If you are a homeowner who's on the fence about moving, you could look into remodeling your home first to see if all you needed was a refresh. This process can be cheaper and less of a hassle than selling your home and could actually increase your property value when you later go to sell the flat.

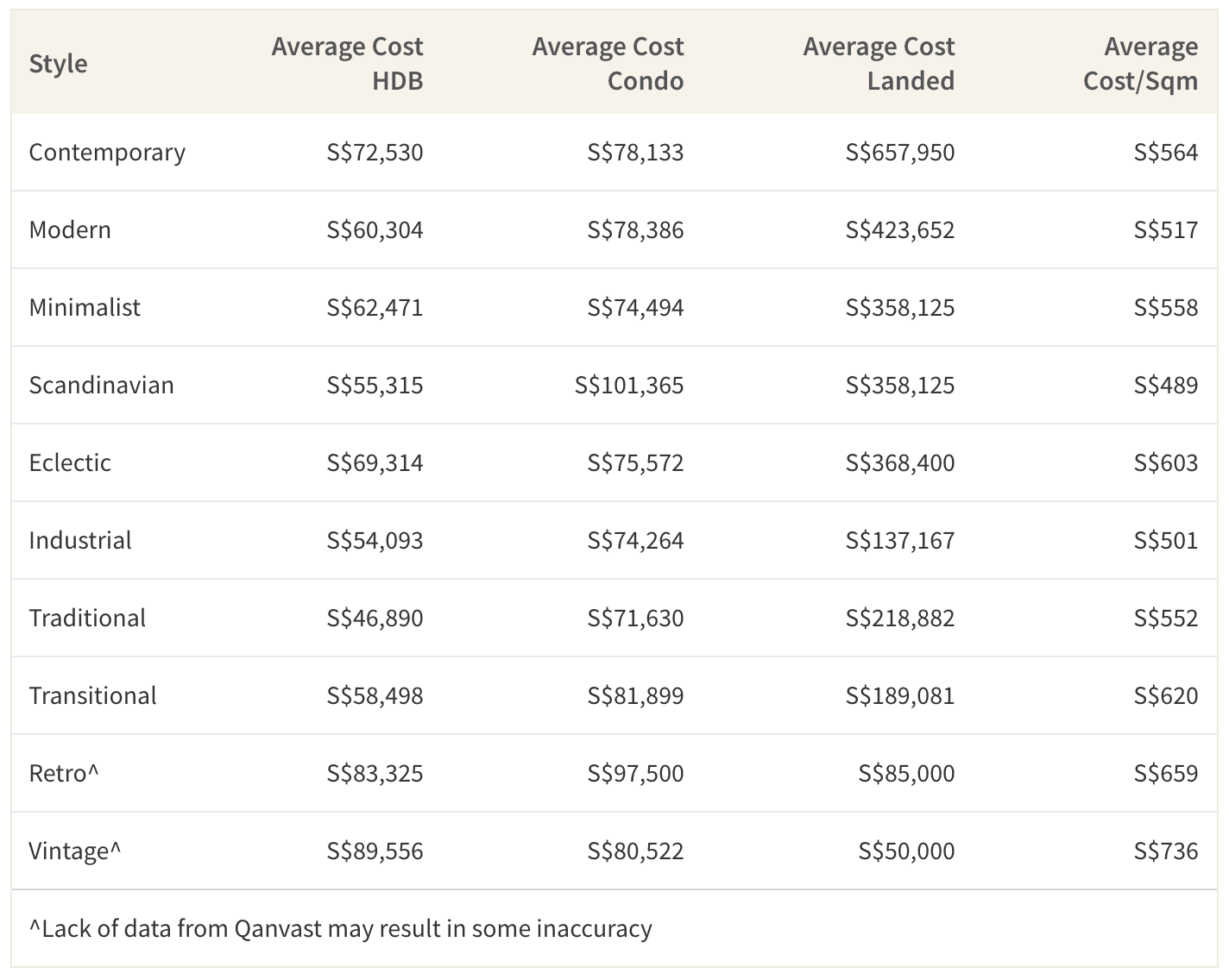

Average Cost of Home Renovation Depending on Style

However, before you get started on renovating your home, you should make a budget and include leeway in case things don't go as planned. If you haven't saved for it and need some extra cash, we recommend taking out a renovation loan will offer you much lower rates than a personal loan. For example, a renovation loan can range from 2%-5% per annum, whereas a personal loan is 3.48%-10.80% per annum. This could save you hundreds of dollars on your monthly payments, and near thousands on the total interest paid (assuming a 5-year loan of S$10,000). Of course, you should consider the length of the loan and the total amount you will pay, otherwise known as the effective interest rate.

Other Costs To Consider Before Buying an HDB Resale

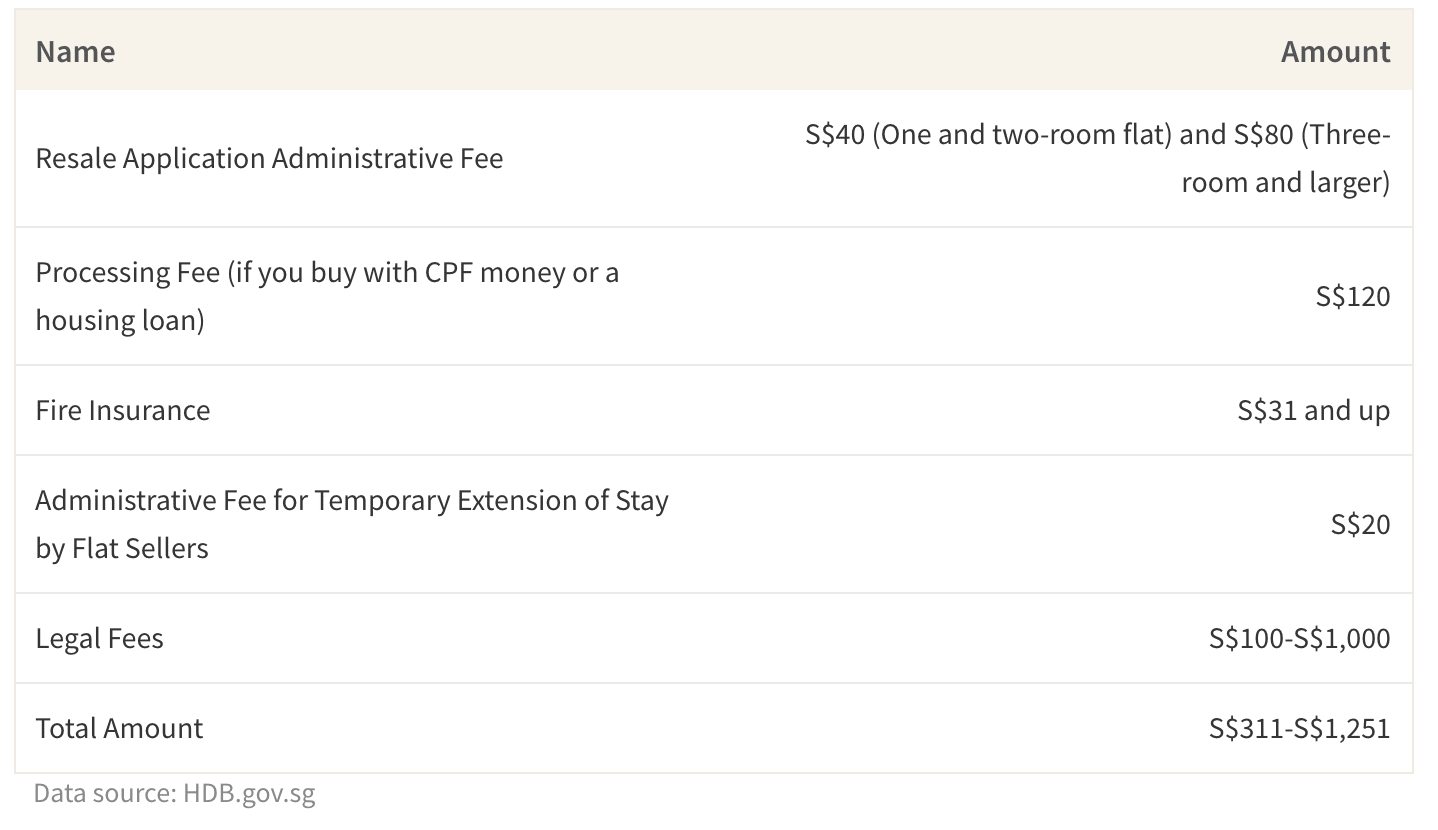

Let's say you found a great property and are ready to take out a mortgage. While you may be approved for a necessary amount of money to buy the Resale, don't forget about the additional costs you will have to pay. For example, you may have to pay for a booking fee (0%-5% of the property price) and a signing sale and purchase agreement (1%-3% of the property price). Even after you successfully acquire the property, you'll need to get home insurance to protect your belongings. Below are other fixed charges you should factor in for a home purchase.

Costs and Fees for HDB Resale Flats

Those getting a home loan will be charged monthly installments over several years to pay it back. If you default on your monthly payments, your credit rating will fall and it will be harder to acquire a loan in the future. Thus, you may have to sell your house or borrow more, so it's worth seriously planning out repayment schedules before you sign a home loan agreement.

If You're Thinking of Selling, Now May Be a Good time

Since the prices of HDB resale flats have been rising, those interested in selling might find now to be an advantageous time to do so. To get the best value for your home, you'll have to hire someone to evaluate your property, which typically costs about S$200-S$500. While it's true the housing market is currently strong, you should still keep up-to-date with the state of the economy before you decide to put your house on the market.

Please note that if you've not yet fulfilled your minimum occupation period of 5 years, you won't be able to sell. Moreover, if you're selling an HDB property in order to buy another one, you can take advantage of the Enhanced Contra Facility to reduce cash outlay needed for your resale HDB flat and reduce the mortgage loan needed and its subsequent payments

No Matter the Conditions, Prioritise Your Budget

With several grants offered to first- and second-time buyers, you might be tempted to move into your dream home now. Especially as businesses and schools are moving towards longer-term stay-at-home solutions, being comfortable where you live is of the uppermost importance. That being said, residential real estate prices are currently rising. Therefore, you should make it your priority to know what you can afford and what you're willing to borrow. If you're selling, you could factor in how the market might temporarily inflate your current property's price as well. With these in mind, you will be one step closer to finding your desired home.

Anya is a Research Analyst for ValueChampion who focuses on loans and investments in Singapore. Previously, she assisted global consultancies, hedge funds and private equities with primary research at a high-growth fin-tech based in London. A graduate of the University of Oxford and King's College London, Anya is currently interested in applying quantitative research to help consumers make better financial decisions.