Bukit Batok Fire and Home Insurance

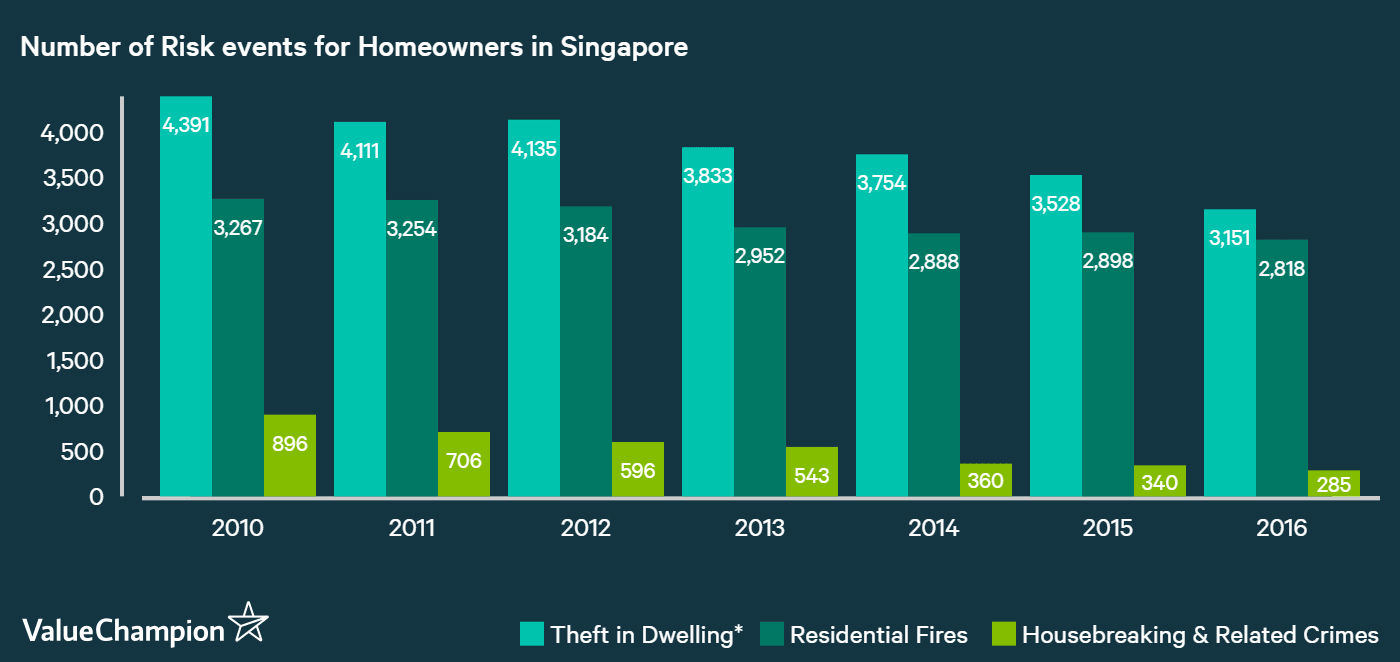

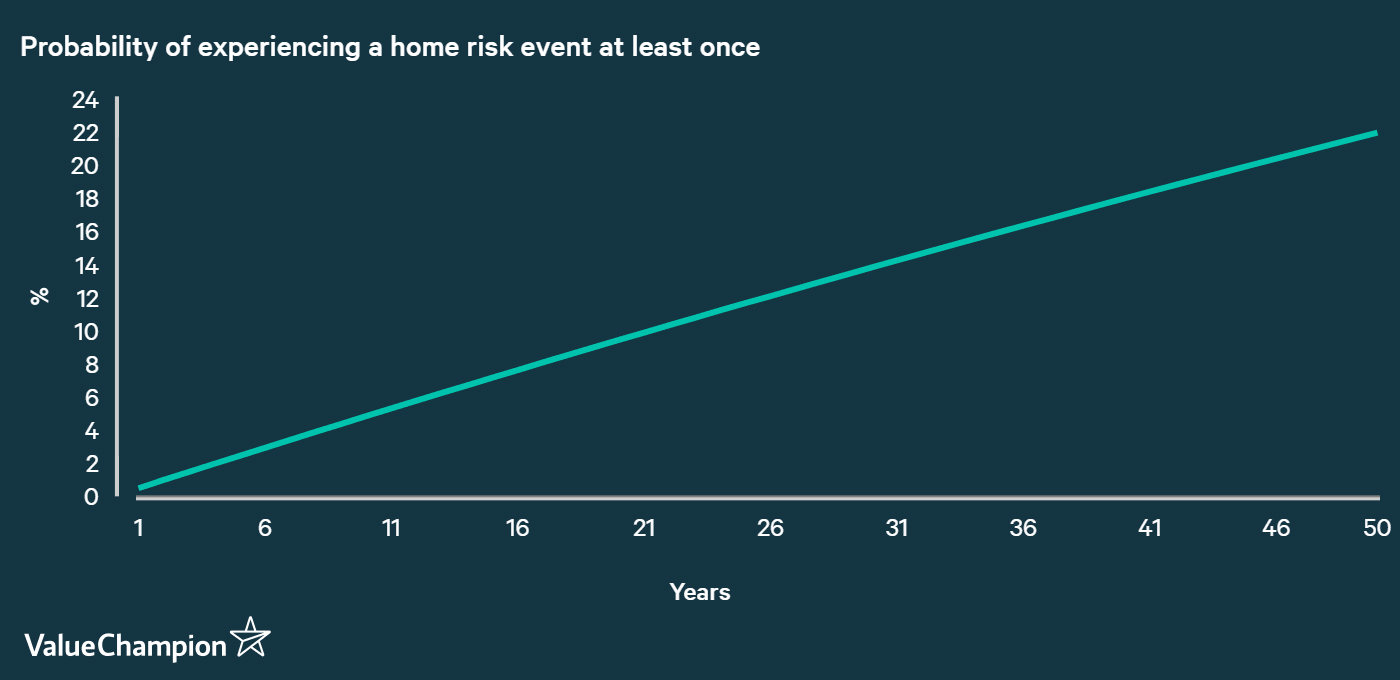

Last night's fire in Bukit Batok is a sober reminder of how bad things can happen to anyone. True, residential fires only occur about 3,000 times a year. While this may sound low in context of 1.3mn households living in Singapore, this can actually translate to about 10% probability that one could suffer a fire accident at least once over his adulthood (i.e. 50 years). Given that such an accident can practically wipe out everything you own in your flat, a 10% chance is too high to completely disregard. While many people may believe that merely having a fire insurance policy for their flat provides sufficient level of protection against such a risk, we will show here that this is actually not quite true.

Why home content insurance is important

Most Singaporean homeowners should already have a fire insurance policy for their residences. However, fire insurance itself is actually not adequate to provide full protection on your home. For instance, while fire insurance should cover both the fire and smoke damage on the building itself, it actually doesn't cover any of one's personal belongings. Rather, it will only pay to restore the most "basic" parts of your flat, like this family experienced here. Without a home content insurance, therefore, a homeowner of a typical 4-room flat could easily lose S$80,000 worth of furniture, appliances, personal belongings and renovation work.

On the other hand, some home content insurance policies that reimburse you for your damaged personal belongings cost as little as S$30 to S$50 per year. Even if you were to pay this for 50 years, the total cost would sum up to around S$2,500. This seems like a cheap way of protecting your home, especially in comparison to the S$8,000 of expected loss (S$80,000 x 10%) one could experience. This math would actually be even more favorable if you account for other potential risks that a home faces like theft.

Emergency accommodations

When your flat gets burned down, you likely won't have a place to stay until it is restored. You might not even have any emergency cash lying around to pay for some immediate needs like clothing. This is another area where having purchased a home insurance policy pays off. Many insurance companies like Etiqa and NTUC Income provide alternative accommodation coverage of around S$10,000 so your family can afford a place to sleep. Not only that, Etiqa goes the extra mile to even provide a few hundred dollars of emergency cash for food and other immediate needs.

Survey and document any damage, save records and receipts

Thankfully, the family in Bukit Batok whose flat was burnt yesterday escaped safely with only minor injuries, according to the press. Their belongings, on the other hand, weren't so lucky. If they had purchased a home content insurance policy before the accident (hopefully they did), they should be able to jump back on their feet soon, right? Actually, it's not that simple. There's one last caution that you must exercise.

If your home actually does catch fire, it's important to keep record of everything you can. Even if you have a home insurance policy, you still need to provide a record of all items that are destroyed or damaged along with their purchase price in order to qualify for reimbursement from your insurance company. While it may be difficult to record every article of clothing you owned, you should still try to list all of the major furniture and appliances that cost the most. Of note, it's generally a good idea to save receipts of your major purchases and renovation works online to ensure you don't lose it in the fire.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.