Average Cost of Home Insurance 2024

A typical home insurance policy in Singapore provides protection on the policyholder's home contents (i.e. TV, sofa, laptops, and other valuables in the property) and interior renovations (i.e. fixtures and fittings that you’ve added to the original house). This is different from a fire insurance policy, which only protects the original structure of your flat and is typically purchased with your home loan. Home insurance's price and coverage may differ based on the size and type of the property, ownership status, and appraisal of your actual home value. Below, we discuss the average cost of home insurance for prospective buyers to help them make a more educated decision.

Table of Contents

- Cost of Coverage for HDB Flat Owners

- Cost of Coverage for Private Homeowners

- Cost of Coverage for Landlords

- Cost of Coverage for Tenants

- How to Choose the Best Home Insurance

Average Cost of Home Insurance for HDB Flat Owners

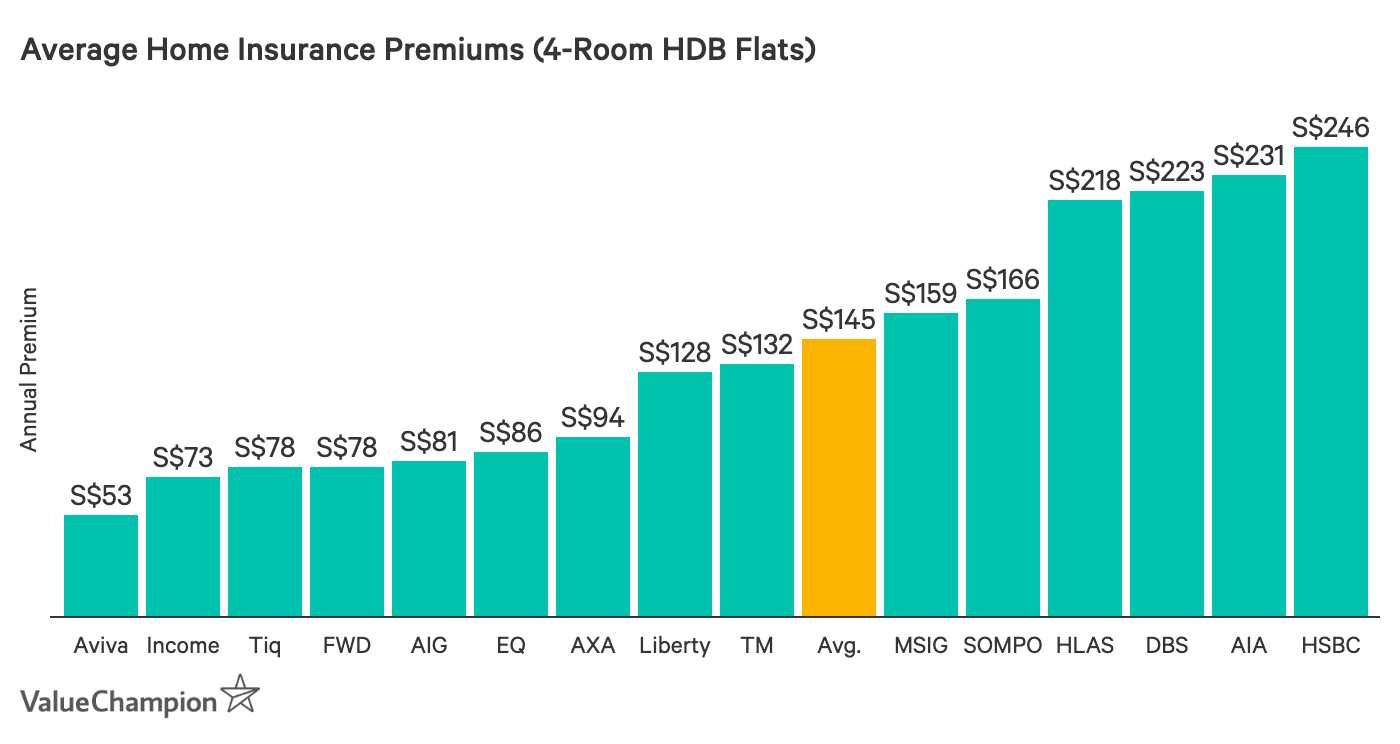

According to our study of 16 companies that offer home insurance, we found the average price of home insurance to be about S$145 a year for a 4-room HDB flat owner in Singapore, the most common type of housing in the country. These policies represent the more "basic" offerings in the market that only cover "named perils," meaning you are able to recover the loss to your personal properties resulting from fire, earthquakes, typhoons, theft, and other events designated by the insurer. Premiums ranged from S$53 to around S$270, but on average these policies covered around S$45,000 of home contents and S$111,000 of home renovation costs, which should be sufficient for an average household's basic needs.

Home insurance for smaller HDB flats cost about S$90 on average, while policies for 5-room and executive flats cost around S$220 on average. These policies provide different levels of coverage for home contents and renovations; below, we've demonstrated the most typical amount of coverage for each below.

| HDB Flat Type | Average Price | Estimated Coverage Needs for Contents | Estimated Coverage Needs for Renovations |

|---|---|---|---|

| 3-room or below | S$90 | S$20,000 | S$30,000 |

| 4-room | S$145 | S$30,000 | S$50,000 |

| 5-room or above | S$220 | S$50,000 | S$70,000 |

Average Cost of Home Insurance for Private Homeowners

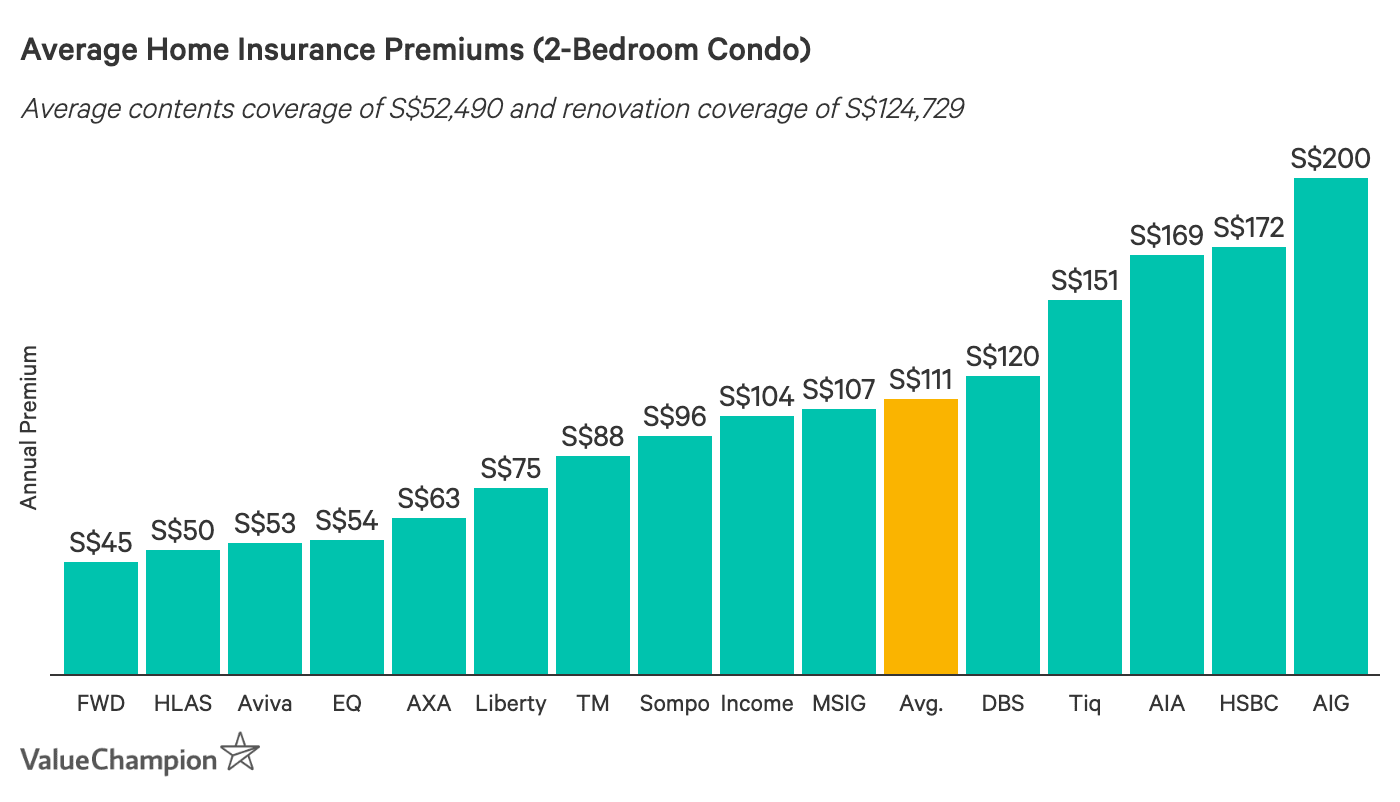

Average cost of home insurance for a 2-bedroom private property was S$105 for policies that cover approximately S$27,000 of home contents and S$70,000 of home renovation costs. However, prices of individual policies ranged from S$45 to S$200, with some variations in coverage as well. We think this level of policy is probably sufficient for the average household living in a 2-bedroom condo. Also, it is worth noting that your building itself should already be covered by the fire insurance provided by the condo's management corporation strata title.

If you are looking for higher level of coverage for your home, you should expect to pay anywhere between 50%-150% extra for your home insurance policy, depending on the insurer that you are purchasing from. Also, there are even more expensive policies available for purchase for those living in landed properties that require additional protection for their buildings. For instance, the average cost of a landed property in Singapore costs around S$498 per year for around S$1,000,000 of total coverage.

| Private Home Tier | Average Cost | Estimated Content Coverage Needs | Estimated Renovations Coverage Needs |

|---|---|---|---|

| 2-Bedroom | S$105 | S$30,000 | S$80,000 |

| 3-Bedroom | S$170 | S$50,000 | S$130,000 |

| 4-Bedroom | S$265 | S$80,000 | S$200,000 |

| Landed (Bungalow) | S$498 | S$77,500 | S$1,000,000 (inc. building) |

Average Cost of Home Insurance for Landlords

Because fire insurance policies only cover the building, it is a good idea for landlords to insure the fixtures and fittings that they've added to their rental properties in case they get damaged. A few insurers offer landlord plans that that feature just renovation coverage and some landlord-specific benefits like loss of rent and liability coverage. Overall, the average cost of a landlord policy is S$156, but some insurers let you customise the amount you need which can reduce your cost to as low as S$35-S$55 for up S$70,000 worth of coverage. You should also be aware that while certain insurers may offer very low pricing for small amounts of renovation coverage, there is usually a minimum premium in place. From our research, we found that the average minimum premium is S$65.70.

| Average Renovation Coverage | Average Premium |

|---|---|

| S$66,500 | S$94.78 |

| S$147,500 | S$150.05 |

| S$273,600 | S$216.10 |

Average Cost of Home Insurance for Tenants

For tenants, the cost of home insurance really depends on how much personal belongings you have in the property, since there’s no need for you to insure the building structure and built-in fixtures. The average cost of a tenant plan that only covers contents is S$111. Tenants who are renting out small flats or rooms in a flat can find home insurance plans for as cheap as S$35. On the other hand, tenants who are renting out larger condos and need more than S$70,000 of coverage can expect to pay between S$170 and S$180. In addition to contents coverage, home insurance plans for tenants also feature renter-friendly benefits like tenant liability coverage, alternative accommodation coverage (if you need to stay elsewhere during repairs to the flat), and mover's damage.

| Average Contents Coverage | Average Premium |

|---|---|

| S$32,700 | S$71.00 |

| S$52,700 | S$99.00 |

| S$83,000 | S$158.00 |

How to Choose the Best Home Insurance

Home insurance policies contain lots of caveats that make it hard to choose the overall “best”. One rule of thumb is that you should never under-insure your property and contents. If you do, you will get paid substantially below the value of your properties. Therefore, you should always try to find the cheapest policy that provides sufficient amount of coverage for your properties. Also, it’s important to carefully investigate your policy and understand its various sub-limits within the home content coverage. There are items like cash, jewellery, bikes, and pedigree pets that the insurer will compensate only up to a certain limit. Lastly, some policies cover your legal liability to your tenants, landlords, or a third party, so this should be taken into consideration when choosing the best deal.

Read More:

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.