Do You Really Need Mortgage Insurance?

Homes are an incredibly expensive investment and will make up a large portion of your expenses. In most cases, financial stress is limited if you bought a home you can afford and your mortgage payments are manageable. However, what happens when an emergency strikes and you are no longer able to afford your monthly home loan? In these cases, insurers came up with a product called mortgage insurance (also known as Mortgage Reducing Term Assurance (MRTA)) that will be able to cover your remaining mortgage expenses if you die, become totally and permanently disabled or suffer a terminal illness. But while the allure of the plan may be clear, it is an added expense that you will have to add to your monthly bill. In that sense, it is important to find out—when does your current situation really require you to get mortgage insurance?

Useful If: If You Are Looking to Move Frequently, Have Dependents and Co-Own

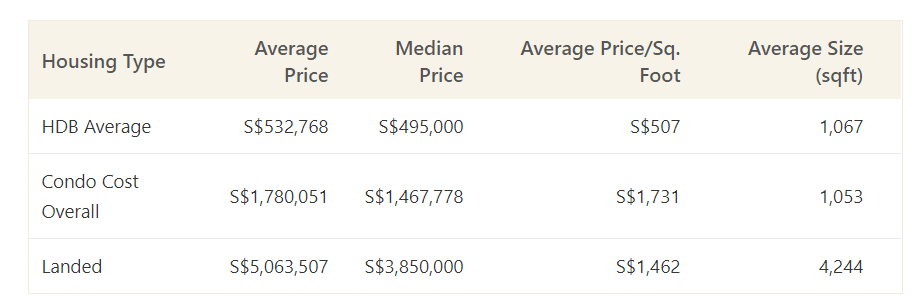

The most important reason why you should be looking into getting an MRTA is if you have dependents who are not financially independent. Considering the median price of an HDB flat in Singapore in 2020 was S$495,000, the typical 25-year mortgage of 80% of the home price would amount to S$1,490-S$1,694 per month. This is roughly 37-42% of the median monthly take-home salary, which is a hefty sum to be responsible even for the average full-time worker. In this case, it could be very beneficial to have an MRTA so if you do pass away or become totally and permanently disabled, your dependents won't struggle to make payments and risk losing their home.

Average and Median Cost of Homes in 2020

A mortgage insurance plan may also be worthwhile if you plan on moving, either from one HDB flat to another or if you move to a private property. This is because while HDB flats are insured under the Home Protection Scheme (HPS) if you are paying for your home with your CPF funds, the HPS does not carry over if you buy a new home, which means you'll need to reapply. However, an MRTA will let you move your coverage from one flat to another and will give you the option to top up coverage if your new home is more expensive. Furthermore, you won't be subject to the higher premiums a new policy will cost you due to the increase in your age.

Lastly, you may also need an MRTA if you bought the property with your partner and are splitting the mortgage costs. In this case, if you were to pass away or become disabled and your partner can't handle the costs on their own, the MRTA payout will help them considerably by providing a payout that they can use to fund the payments.

Pass If: You Bought the Property in Cash, Have Life Insurance, Are Not Looking to Move From HDB Flat, Your Family Can Afford the Mortgage

The most obvious reason why you don't need a mortgage insurance plan is if you bought your property in cash. Since there's no mortgage to pay off, you won't need to worry about your family making payments or losing their home. Similarly, you won't really need an MRTA if your family is able to make the monthly mortgage payments. However, if you want to absolve them of the burden, an MRTA may still be a good fit provided you can afford it.

Another reason why you may not need an MRTA plan is if you are committed to living in the same HDB property and you are using your CPF to pay for your home. In this case, mortgage insurance will be redundant since you are already required to be insured under the Home Protection Scheme. Similarly, if you already have a life insurance or endowment insurance plan, you can be exempt from the HPS and you may not need an MRTA since your life insurance coverage should be enough to cover the mortgage payments should you pass away or become permanently disabled.

How to Get the Most Out of Your Mortgage Insurance Plan

If you decide that an MRTA is the right option for you, then there are several benefits you should consider when looking for a plan. The first is to look for plans that provide a premium refund if you reached the end of your policy term without making a claim. These are good options if you don't want to feel like you "wasted" money paying for protection you didn't end up needing. That said, they are typically more expensive than other types of MRTAs. Additionally, you can look at MRTA's that offer other types of coverage, like critical illness coverage or personal accident coverage. These types of plans will be useful and can even save you money since you are bundling different types of coverage into one plan rather than buying them separately.

At the end of the day however, what's most important is that you can afford both your mortgage and your MRTA premiums. This is why it's imperative that you speak to a financial advisor you trust and compare premiums across different insurers.

More Resources From ValueChampion

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.