MSIG Home Insurance: Should You Get It?

MSIG Home Insurance: Should You Get It?

ValueChampion Rating ![]()

Pros

- Market-leading coverage & benefits

- Above average per item limit for valuables (S$6,000)

- Offers rare benefits like hospitalization allowance and home security system coverage

Cons

- Can be pricey for cost conscious tenants

- Minimum premium of S$119.88 for renters and landlords

Despite the lackluster value for money, MSIG offers some of the most well-rounded features in their comprehensive plans that can give homeowners great peace of mind. Furthermore, the flexibility to add coverage makes it easy to make sure you are getting the exact amount of coverage you need. However, despite MSIG's strengths, there are drawbacks concerning its value for landlords and tenants, as well as its rather high premiums for cost-conscious homeowners.

| Summary of MSIG Home Insurance |

|---|

| Above average premiums but below average value |

| Offers above average 3rd party liability and medical coverage |

| Above average per item limit of S$6,000 for valuables |

| Expensive for tenants, landlords and cost-conscious consumers |

Table of Contents

MSIG Enhanced HomePlus Highlights

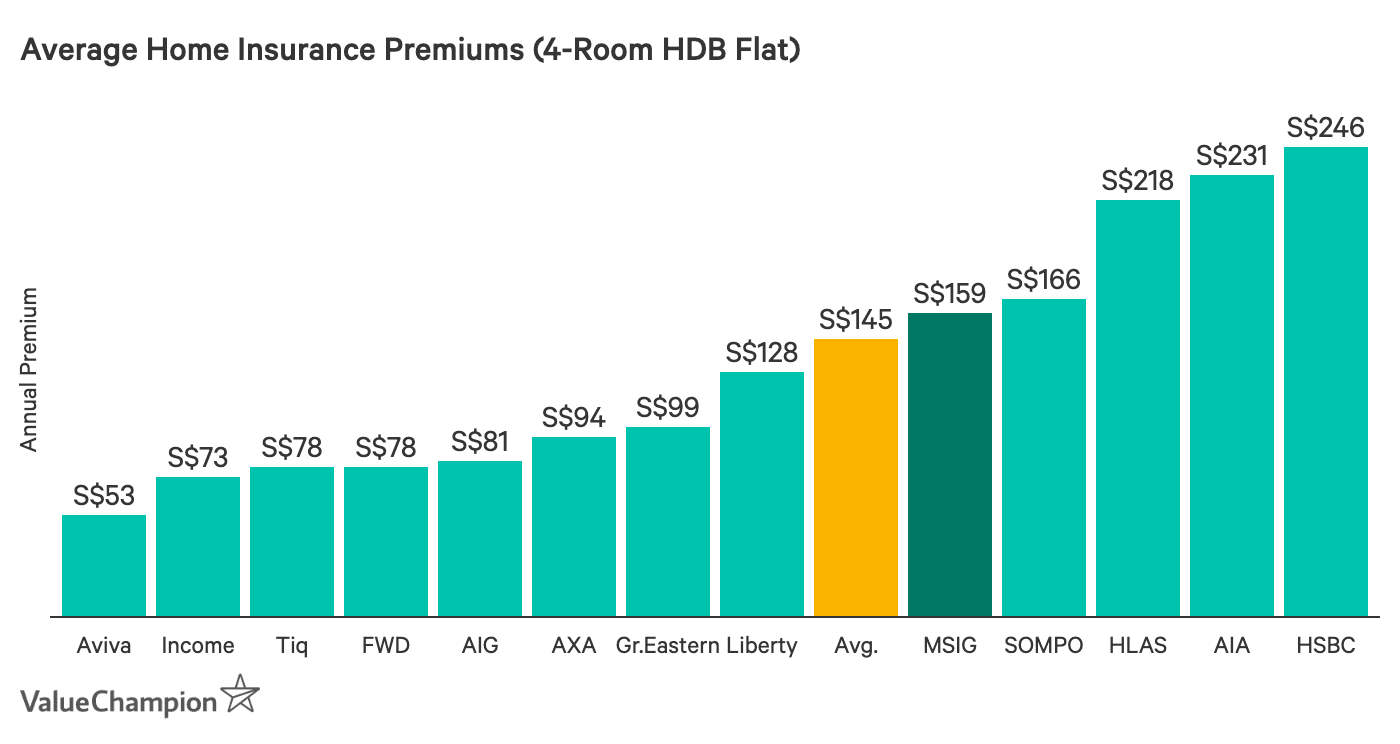

MSIG Enhanced HomePlus home insurance plans will benefit homeowners care less about price and more about coverage. The plan comes in three tiers, Standard, Superior and Ultimate, with increasing levels of contents and renovation coverage. The combined coverages are S$125,000 for the Standard tier, S$195,000 for Superior, and S$270,000 for Ultimate. To estimate which plan is most suitable for you, our home renovation and home contents article will provide you with guidelines. MSIG's premiums generally fall around the average, with the exception of the Standard plan that costs 12% above the average of plans with similar coverage. Thus, due to the rather uncompetitive premiums, MSIG's value suffers compared to other insurers with cheaper premiums for the same levels of coverage.

MSIG's Enhanced HomePlus has 15 additional benefits that are great value-adds to people who are looking for peace of mind coverage. While its value ratio is slightly below the industry average, MSIG offers alternative accommodation (10% of contents and reno sum) and also comes with rare-to-find features like hospitalisation allowance (up to S$6,750) and S$1,000,000-third party liability coverage.

However, MSIG Enhanced HomePlus does have drawbacks. First, it may not benefit tenants who only need contents coverage, as all 3 of its plans include renovation coverage. Likewise, it won't benefit landlords who are renting out unfurnished flats. Instead, tenants and landlords have the option of opting for MSIG's Home Insurance plan which only offers contents and contents-related coverage if they want to stick with MSIG. However, with the minimum premium set at S$118.70, it is already considerably more expensive than many other tenant or landlord-specific plans on the market.

MSIG Enhanced HomePlus for HDB Homeowners

HDB Homeowners who aren't restricted by price and care more about miscellaneous peace-of-mind coverage may find MSIG's home insurance plans a good buy. All 3 plans offer 14 additional benefits, although the Standard plan's benefit limits are 30% lower than the Superior and Ultimate options. While these benefits can be valuable to everyone, MSIG offers particular benefits that can be especially beneficial for HDB owners, such as conservancy charge coverage, damage to security systems and fire extinguishment expenses.

However, the amount of value these plans will bring HDB homeowners will vary depending on the homeowner's price sensitivity. For instance, MSIG Enhanced Home Plus plans won't benefit owners of small to average HDB flats due to their above average premiums. Its Standard and Superior plans, which provide the best coverage for 3 to 4-room HDB flats, cost 11-12% more than other plans on the market that provide similar coverage. Furthermore, even larger flats that will be insured with the Ultimate plan only cost a few dollars less than similar plans on the market and won't entice homeowners looking for considerable savings. In this case, MSIG will be worth purchasing only for owners who aren't price sensitive and value benefits over cost-saving.

| Home Size | Contents Coverage | Renovation Coverage | Premium |

|---|---|---|---|

| 3-Room (Standard Plan) | S$50K | S$75K | S$119.88 |

| 4-Room (Superior Plan) | S$80K | S$115K | S$178.20 |

| 5-Room (Ultimate Plan) | S$120K | S$150K | S$235.44 |

| Industry Average | S$50,623 | S$125,989 | S$157.00 |

| Home Size | Contents Coverage | Renovation Coverage | Premium |

|---|---|---|---|

| 3-Room (Standard Plan) | S$50K | S$75K | S$118.77 |

| 4-Room (Superior Plan) | S$80K | S$115K | S$176.55 |

| 5-Room (Ultimate Plan) | S$120K | S$150K | S$233.26 |

| Industry Average | S$50,623 | S$125,989 | S$157.00 |

MSIG Enhanced HomePlus for Private & Landed Property Owners

Owners of private properties like condos will find MSIG to be valuable if they need a plan focused renovation and individual item coverage. While the premiums for MSIG Enhanced are lackluster, averaging around or slightly above the average, the coverage is generous enough to entice some condo owners who own expensive items. In particular, MSIG offers a S$6,000 valuable item limit, which is one of the highest individual item limits on the market. Furthermore, you'll receive coverage not only for your contents that are in your home, but they'll be covered if they get damaged by movers, stored in a temporary location and even if they get stolen by your domestic worker. Furthermore, unlike other insurers who combine security systems, keys and locks coverage, MSIG offers them separately. This makes it a good option for condo owners who have expensive security systems in place as well.

We recommend MSIG HomePlus with additional building top-up for homeowners who have relatively small (less than 200 square metre) landed properties. Along with affordable rates on renovation and content protection, MSIG gives landed property homeowners great peace of mind when it comes to ample benefits such as high jewellery & watches coverage (30% of total sum insured vs. market average of under 9%). However, it may be more worthwhile to consider other insurers like AXA for larger landed properties for a couple of reasons. First, the building coverage limit is S$1,000,000, so owners of large bungalows will end up underinsured. Second, even if you require less than S$1,000,000 of coverage, you will be able to find cheaper premiums with other insurers since you can only add additional cover to the Ultimate plan.

| Home Size | Contents Coverage | Renovation Coverage | Building Coverage | Premium |

|---|---|---|---|---|

| 2-Bed | S$50K | S$75K | N/A | S$119.88 |

| 3-Bed | S$80K | S$115K | N/A | S$178.20 |

| 4-Bed | S$120K | S$150K | N/A | S$235.44 |

| Landed (Bungalow) | S$120K | S$250K | S$1M | SS$725.76 |

| Industry Average | S$54,896 | S$136,695 | N/A | S$186.00 |

| Home Size | Contents Coverage | Renovation Coverage | Building Coverage | Premium |

|---|---|---|---|---|

| 2-Bed | S$50K | S$75K | N/A | S$119.88 |

| 3-Bed | S$80K | S$115K | N/A | S$178.20 |

| 4-Bed | S$120K | S$150K | N/A | S$235.44 |

| Landed (Bungalow) | S$120K | S$250K | S$1M | SS$725.76 |

| Industry Average | S$54,896 | S$136,695 | N/A | S$186.00 |

MSIG Home Insurance for Landlords and Tenants

MSIG's Essential plan won't benefit landlords or tenants due to its automatic inclusion of both renovation and contents coverage. Even landlords who rent out furnished flats may end up paying for coverage that they won't use such as loss of pet loss coverage, domestic worker clothing coverage, accidental death coverage for you and your spouse. Instead, we recommend landlords who are renting out furnished flats to look for insurers that offer home insurance plans that provide basic contents coverage, such as Income.

We also don't particularly recommend MSIG's alternative "Home Insurance" plan for tenants or landlords. Despite its flexibility that allows the policyholder to insure any amount (in the multiple of S$10,000) of building or contents coverage, the minimum premium of S$85.60 limits the choice of many non-homeowners. Landlords must get at least S$200,000 of building coverage, while renters must get at least S$60,000 of contents coverage in order to be eligible in the first place, which may be too much for certain consumers. In our opinion, Income offers a cheaper alternative for landlords, and AXA or Tiq offer a better-value protection scheme for renters.

Policy Excess

An excess is the amount you have to pay before your insurance company steps in to pay your claim. MSIG has a S$100 excess for each loss to contents, building or renovation that is caused by water, such as hurricanes, cyclones, floods, windstorms and water overflowing from leaking or bursting pipes.

Claims Information

MSIG lets you submit your home insurance claims online. As soon as you are aware that loss or damage occurred, you should notify MSIG as soon as possible. While awaiting news from MSIG, you should do whatever you can to minimise the loss or damage. You should submit the online home insurance claim form along with required documentation and receipts as soon as possible.

| Contact Information | |

|---|---|

| Customer Service | +65 6827 7602 |

| Claims Hotline | +65 6827 7660 |

| Claims Information | Home Insurance Claims Procedure |

| [email protected] | |

| Submit Your Claim | Online Form |

MSIG Enhanced Home Insurance Summary

For some homeowners, MSIG can be a great fit, especially if they are looking for a plan that can protect their valuables. However, consumers on a budget may not find the comprehensive benefits valuable enough to justify the higher price. Below, we summarise the main benefits MSIG offers. Find out our top picks for the best home insurance policies in Singapore if you'd like to compare MSIG to other insurers on the market.

| Benefit | Standard Limit | Superior Limit | Ultimate Limit |

|---|---|---|---|

| Contents | S$50,000 | S$80,000 | S$120,000 |

| Renovations | S$75,000 | S$115,000 | S$150,000 |

| Personal Liability | S$500,000 | S$500,000 | S$500,000 |

| Property Owner's Liability | S$1,000,000 | S$1,000,000 | S$1,000,000 |

| Worldwide Accident Protection | S$20,000 | S$30,000 | S$30,000 |

| Hospital Cash Benefit | S$50/day | S$75/day | S$75/day |

| Alternative Accommodation | |||

| Loss of Rent | |||

| Debris Removal | |||

| Conservancy Charges | S$500 | S$750 | S$750 |

| Cost of Temporary Item Protection | S$1,500 | S$2,000 | S$2,000 |

| Temporarily Removed Contents | S$7,500 | S$12,000 | S$15,000 |

| Lock/Key Replacement | S$500 | S$750 | S$750 |

| Death of Pet | S$500 | S$750 | S$750 |

| Burglary of Money | S$500 | S$750 | S$750 |

| Emergency Cash Allowance | S$500 | S$750 | S$750 |

| Security Systems Damage | S$500 | S$750 | S$750 |

All insurance product-related transactions via AMTD PolicyPal Group (including Value Champion) are arranged and administered by Baoxianbaobao Pte. Ltd., our insurance broker and exempt financial adviser licensed and regulated by the Monetary Authority of Singapore. This insurance purchase is powered by Baoxianbaobao Pte. Ltd.

Protected up to specified limits by SDIC. This is only product information provided. You may wish to seek advice from a qualified adviser before buying the product. If you choose not to seek advice from a qualified adviser, you should consider whether the product is suitable for you. Buying an insurance product that is not suitable for you may impact your ability to finance your future financial needs. If you decide that the policy is not suitable after purchasing the policy, you may terminate the policy in accordance with the free-look provision, if any, and the insurer may recover from you any expense incurred by the insurer in underwriting the policy.