How to Optimise Your Personal Finance Strategy During the COVID-19 Crisis

Dealing with the financial repercussions of COVID-19 can be incredibly challenging and quite stressful. It's tempting to retreat into what feels safe at times of high pressure and risk. However, with a sound financial strategy it's possible to transform your savings and expenses into opportunities to grow. You may even be able to optimise your insurance policy, mortgage or personal loan to save money in the long run. Our expert team at ValueChampion has provided a detailed roadmap below, to help you approach your finances with confidence even in these turbulent times.

Table of Contents:

- Investing: Should My Strategy Change Due to the Economic Impacts of COVID-19?

- Bank Accounts: Ensure Even Your Safe Funds are Actively Growing

- Credit Cards: Never Pay "Full Price"–Let Rewards Offset Your Purchases

- Insurance: Understanding and Improving Your Coverage

- Loans: What Borrowers Need to Know to Be Confident in Uncertain Times

Investing: Should My Strategy Change Due to the Economic Impacts of COVID-19?

Markets around the world have experienced significant volatility due to the economic uncertainty caused by the novel coronavirus. Depending on your perspective, this can cause a range of emotions. Individuals investing for their retirement are likely to feel uneasy as they see markets tanking. On the other hand, individual investors may see the downturn as a great opportunity to "buy low".

Both reactions are rational, though there are some important considerations to keep in mind. First, unless you are planning to retire very soon, you can take a deep breath. This is not the first time the stock market has experienced significant volatility, nor will it be the last. In fact , markets have historically performed well over the long-term. Therefore, it is prudent for most individuals to stay the course when it comes to their retirement strategy. If you don't have a strategy, it is important to conduct research and develop a plan. For those seeking professional assistance, robo advisors are an intriguing, low-cost, way to approach investing. These services cost a fraction of the fees associated with traditional wealth management and do not typically have high wealth requirements.

If you are the type to invest on your own, we strongly recommend that you develop a solid understanding of various investing strategies and valuation techniques. There's nothing wrong with trying to time the market—provided that you know what you're doing. As you do so, it's important to avoid fees that will cut into your returns. For example, the commissions of the top online brokerages typically cost about a third of the average fees.

Bank Accounts: Ensure Even Your "Safe" Funds are Actively Growing

It's also a good time to stash away funds for a rainy day, and even optimise them for boosted savings. You can do so effectively by investing in either a fixed deposit or savings account–which are amongst the safest ways to earn on your existing money. How can you decide which is a better match for you?

Fixed Deposits: Safe & Secure, But Less Flexible

Fixed deposit accounts are a form of investment where consumers place funds with the bank for a set amount of time, earning at a predetermined interest rate based on deposit size and tenor. In layman's terms, the amount you'll earn depends on how much you're depositing and how long you've agreed to keep it there, without making a withdrawal. Bank requirements vary, but you can typically place anywhere from S$500–S$500k+ for time periods ranging from 3 months to 3+ years. If you make an early withdrawal, you risk losing all interest however–so fixed deposits aren't a great option for emergency funds you may need to access.

| Average Board Interest Rates by Deposit Size and Tenure 2020 | |||

|---|---|---|---|

|

|

| |

| Short Tenure (3, 6 Mo) | 0.41% | 0.64% | 0.77% |

| Medium Tenure (9, 12 Mo) | 0.71% | 1.02% | 1.09% |

| Long Tenure (24, 36 Mo) | 1.14% | 1.14% | 1.20% |

If you are considering a fixed deposit investment, be aware that the market is essentially ruled by promotional rates. These rates change every month, have specific placement minimums and tenors (usually S$20k+ for between 6-12 months), and are significantly higher than board rates. Every bank offers a different promotional rate, so be sure to compare before making a final decision.

Savings Accounts: Competitive Rates & Fluid Access

Savings accounts are more flexible than fixed deposit investments, as you can withdraw funds as needed. However, if you fall below a minimum average daily balance (typically S$500–S$1k), you'll typically be charged a S$2 monthly fall-below fee. This can significantly cut into your interest earnings, especially when your balance size is fairly small.

There are 3 main "types" of savings accounts in Singapore:

- Basic Accounts have the lowest rates, but require little-to-no maintenance; you simply deposit money whenever you can and your balance grows from interest

- Multi-Product Accounts are more complex, rewarding account holders with interest rate boosts when they engage in other bank products (like insurance, investments or credit cards) and meet certain minimum transaction requirements. These accounts have very high effective interest rate potential–but only for those who are financially savvy enough to closely track their personal finances

- Incentivised Growth Accounts offer a middle ground–slightly elevated interest rates and moderate maintenance. These accounts usually reward consumers who can make consistent month-on-month deposits and refrain from making withdrawals

It is important to mention that several banks are reacting to the current climate by reducing interest rates for their most competitive savings accounts. The changes will be taken live in May. As a result, it's important to apply with the projected (rather than just the currently advertised) rates in mind.

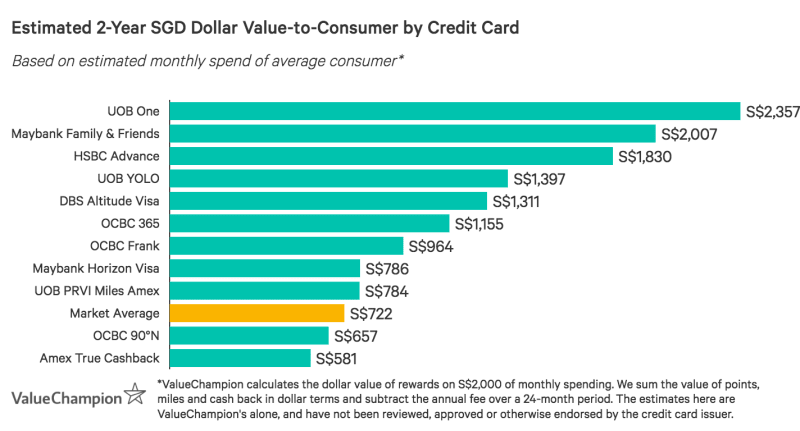

Credit Cards: Never Pay "Full Price"– Let Rewards Offset Your Purchases

In times of risk and uncertainty, budgeting can feel especially frustrating and stressful–especially if you're now out of a job. However, it's now more important than ever to make the most of your money, including your spending. It's fairly likely you already have a credit card. Are you putting it to its fullest use? If you're looking for a new card–perhaps to take advantage of a sign-on bonus–how do you pick the best option? And finally, what are the best options to keep in mind given the current climate? Let's break it down and explore these questions below.

I Have a Credit Card. How Do I Make Sure I'm Maxing Out All the Rewards?

There are a few important things to take into consideration. First, make sure you know what types of transactions actually qualify for boosts advertised by the credit card company. For example, what kinds of purchases qualify as "online" spend? Some cards only reward online fashion, like spend on clothing or shoes; others include everything from food delivery to bill-pay. Check the terms & conditions to ensure that you're using your card in a way that actually optimises rewards.

Also, take the time to check up on your card's homepage & loyalty programme page once in a while. You'll typically get a notification when larger promotions are launched, but smaller and frequently changing initiatives may go unnoticed. Many programmes offer discounts on food delivery and with online shopping merchants, which might be especially helpful in our current environment.

Finally, rethink annual fees. Most banks will consider waiving a card's annual fee for loyal customers with a good track record. This usually doesn't apply to ultra-expensive options, but it's always worth asking. If your card offers a spend-based waiver, keep track to ensure you meet the minimum requirement. Without fees, you won't have to worry about card costs cutting into your rewards.

I'm Looking for a New Card. What's the Best Way to Decide on One?

You may be on the market for a new credit card–after all, sign-on promotions are quite attractive, with many banks offering S$200+ to successful applicants. However, remember to consider whether a card will fit your needs in the long run. Can you meet the minimum spend requirement, if there is one? Do you frequently spend in the highest-earning categories? If rewards are capped, will you cut off your earning potential prematurely? And finally, do the perks and privileges align with your lifestyle and interests? We cover these topics and others in a dedicated guide found here.

What Types of Cards Best Fit Our Current Environment?

Beyond selecting a credit card that fits your general spending habits, you might also want to consider options with features that align with the current climate. For example, while the vast majority of credit cards do not reward spend on hospital bills, there are a few–like Amex True Cashback Card–that do in fact reward medical spend. There are also a few options on the market that offer miles or cashback for paying recurring bills, and a handful–though rapidly decreasing in size–that reward insurance premium payments.

No matter what, it's important to remember that a credit card should complement your spending rather than enable unsustainable budget "stretching." Missing payments leads to late fees and interest charges on your balance, ultimately leading to debt and damaging your credit score. When paired with responsible budgeting and cognizant spending, using a credit card can ultimately help you save on a daily basis.

Insurance: Understanding and Improving Your Coverage

Your insurance coverage is especially crucial during pandemics as it will provide much needed financial protection if you get sick. During the COVID-19 crisis, not only have insurers expanded coverage to include COVID-19-related claims in a myriad of policies, including life, health and personal accident insurance, but they have also stepped up to increase benefits and help their customers stay covered during economic hardship. Below, we answer some frequently asked questions surrounding your coverage.

What Happens If I Can't Afford My Insurance Premiums?

One of the greatest worries for people who have been recently laid off or left without pay is how to manage their monthly bills. Based on how many insurance plans you have, your insurance obligations can make up a considerable portion of your monthly budget. If you're considering cancelling your plans so you can reduce your monthly payments during this time, check with your insurer beforehand. They may be offering payment deferment for certain policies. If they're not offering deferment or other forms of financial relief, see if you can reduce your coverage for cheaper premiums.

Aviva, Income, Prudential, Great Eastern and FWD are some of the insurers who are offering 6-month premium deferments for life and health insurance customers who got laid off, sustained a drop in income or were put on a no-pay leave. Therefore, you can still maintain necessary health and life coverage while receiving some financial relief. However, you will still be responsible for paying back all of the deferred premiums when the deferment period ends.

Am I Currently Covered for COVID-19 Medical Expenses?

People who already have Integrated Shield Plans will be fully covered for hospitalisations related to COVID-19. The range of coverage depends on your insurer, but you will at least be covered fully for hospitalisations related to COVID-19. However, your coverage will lapse if you travel during this time period.

Insurers and their Integrated Shield Plan Coverage for COVID-19

| Insurer | COVID-19 Coverage |

|---|---|

| AIA | Hospitalisation |

| Aviva | Hospitalisation, Surgery, Selected Outpatient Treatment |

| Great Eastern | Hospitalisation (Domestic & Overseas) |

| Income | Hospitalisation |

| Prudential | Hospitalisation, Pre- & Post-Hospitalisation Treatment |

I Want to Increase My Coverage. What Are the Best Supplementary Plans for COVID-19?

However, if you are looking for more coverage, you can consider adding a personal accident plan. These plans provide death and disability coverage for accidents and infectious diseases and offer miscellaneous benefits like a weekly payment benefit and a daily hospital cash benefits. Unlike health insurance, which covers only medical expenses, personal accident plans will give you a payout if you were to get sick or get into an accident. Thus, they can be a good option if you are worried about losing money if you get sick (for instance, if you are a freelancer worker). If you can spare the extra cash, you can get a comprehensive personal accident plan for under S$20 per month.

I Have to Travel In the Upcoming Weeks. Which Insurance Plan Will Cover Me?

Unfortunately, since COVID-19 is a known event and the Singapore government is advising against travel, your coverage will be limited. While you can still get a travel insurance plan, you won't be covered for any COVID-19 related claims. Furthermore, your Integrated Shield Plan most likely won't cover you for COVID-19 hospitalisations if you get sick on your trip. As always in uncertain times, you should reach out to your insurer directly to double check your coverage to avoid unpleasant surprises when it comes time to file your claim.

I Don't Have Insurance Coverage, Should I Consider Buying a Plan?

You should only consider committing to an insurance policy if you know you will be able to afford the premiums. You should also remember this is a temporary situation and things will revert back to normal after the pandemic is over. Therefore, it is not advisable to panic-buy large amounts of protection only to realise you can't afford the premiums. This is especially true with insurance policies like life insurance that require long-term financial commitments and have costly early termination fees. If you do get sick and need to be hospitalised for COVID-19, your treatment at public hospitals will be free. You'll only need to pay for treatment at private hospitals, polyclinics or general practitioner clinics.

On the other hand, if this pandemic made you realise that you will need coverage for the long term and you are interested in exploring policies, then purchasing a plan now can be as good a time as any. You can look for a plan that best suits your needs and budget by carefully shopping around and comparing prices. To make comparisons easier, check out aggregator sites that compare prices on one page. For example, our health insurance guide not only explains the amount of coverage found in the average plan but also breaks down the average pricing you can expect for different types of policies.

Loans: What Borrowers Need to Know to Be Confident in Uncertain Times

In these turbulent times, you may still need funds for purchasing a new home or covering unexpected expenses. If you are a current and or prospective borrower, how can you be confident that you are finding the most affordable loan possible?

What If I Need Cash?

Singapore's government has provided a range of financial assistance due to the financial struggles many individuals face as a result of the current economic climate. For example, the Temporary Relief Fund and the Enhanced Care & Support package both provide cash payouts. However, if you're facing severe financial hardship, you may need additional funds to tide you over. Of course, there is no instant fix for your situation, but it is important to be cognisant of your options. From freelancing to learning new skills for your next job, finding a new source of income is imperative.

In the meantime, if you face significant expenses and your savings are not sufficient, you may want to consider applying for a personal loan. Keep in mind that not all loans are created equal. First, you should only apply for loans from licensed lenders and avoid loan sharks. Also, it is essential to compare interest rates before applying for a loan, especially when you are tight on cash. This is because the best loans can cost half as much as the average loan. Finally, you should never apply for a loan that you will not be able to repay, as this will cause further financial hardship as your owed interest accrues. Instead, you should only apply for a loan you can reasonably expect to repay in the near future.

Notes for Homeowners

If you currently own a home and have an outstanding home loan balance, it might be a good time to refinance. For instance, market interest rates are currently lower than they have been in recent years, which is saying something given how low interest rates have been. Furthermore, lenders often offer attractive refinancing rates in order to win customers from their competitors. You can easily compare rates using ValueChampion's free home loan refinancing tool. Before you decide to refinance, we recommend that you review the terms and conditions of your current loan, as there are often fees associated with refinancing or ending your current mortgage prematurely.

If you are out of work, or otherwise struggling financially, it may be worth enquiring with your mortgage lender about mortgage loan deferment. The Monetary Authority of Singapore announced that borrowers impacted by the economic slowdown will have the option to delay their home loan payments by up to 9 months. Keep in mind that this option will likely cost more in total interest expenses, and is only worth considering if you are currently facing financial hardship.

Stay Informed & Safe

The current economic uncertainty can be unsettling. Hopefully, this article helps you conceptualise key issues related to your own circumstances and helps you maintain financial stability. Furthermore, many of these concepts will serve you even once this era concludes. Above all, our team sends its best wishes and hopes that you and your family are able to stay safe through this time.