Best Credit Cards for Monthly Recurring Bill Payments 2024

An average household spends about 15% of their budget on monthly recurring bills like telecom, insurance and utilities. After careful analysis of 100+ credit cards in Singapore, our experts identified and compared the best credit cards for monthly bill payments below, allowing you to spend more on other areas of your life.

| Best Credit Cards for Monthly Recurring Bills | ||

|---|---|---|

| Best for Cashback | UOB One | 5% flat rebate for S$2k/mo spend |

| OCBC 365 | Rebates on essentials with easy fee-waiver | |

| Online Bill Pay | HSBC Revolution | 2 miles per S$1 online spend (inc. transit, ins. premiums) |

| Low Spenders | MB Platinum Visa | Earn S$30/quarter w/ S$300 monthly spend |

| Unlimited Cashback | UOB Absolute Cashback | Unlimited 1.7% rebate with no minimum spend |

| High Spenders | HSBC Advance | Up to 3.5% cashback capped at S$125/month |

| Amex True CB | Unlimited 1.5% rebate + Amex benefits | |

| Best for Miles | KrisFlyer UOB | Up to 3 mi/S$1 on dining, shopping & more |

| Cashback + Miles | HSBC Visa Plat | Rebates on local dining & entertainment, miles for general |

Best Cashback Credit Cards for Paying Monthly Recurring Bills

If you want to maximise cash back from paying your monthly bills, the following cards offer great rates with added benefits like rebate programmes and fee-waivers.

Best Rebate Card for Stable Spenders: UOB One Card

- Pros

- Good fit for budgets of at least S$2,000 per month

- Easy cashback on daily spend

- Gives rebates for paying bills

- Cons

- Doesn't fit inconsistent budgets

- Annual fee

UOB One Card is the absolute best rebate credit card for people who consistently spend about S$2,000/month. At this spend level, cardholders earn 5% general cashback, up to S$300/quarter (S$100/month)–with rates boosted to 10% on Grab & select UOB Travel and 6% for utilities bills. This offers cardholders one of the highest earning potentials on the market, at up to S$1,200/year.

UOB One Card is especially great for bill pay because of its tiered rebate structure. Cardholders’ cashback rate and cap are determined by their lowest spend during a quarter (3 months total). Consistency is key, because spending even slightly lower than S$2,000 during one month drops cashback from 5% to 3.33%, and max earning from S$100/month to S$33/month. Paying monthly recurring bills through UOB One Card can provide that stability and consistency, and help to ensure you meet minimum spend levels every month.

Another reason to use UOB One Card for bill pay is that its UOB SMART$ Programme can provide ‘double’ value when you pay insurance premiums with UOI. Not only do payments count towards your minimum spend tier, they also earn SMART$ with select merchants–like UOI–which can thereafter be used to offset future purchases. Many merchants are part of the SMART$ Programme, so you can also earn ‘double’ value on dining, groceries, wellness and more.

Ultimately, UOB One Card is a great option for earning top cashback on all of your spend, including on bill payments, as long as you have a fairly consistent budget.

- Annual fee: S$192.60 (first year- waived)

- 5% rebate on general spend, up to S$200/quarter (S$2,000 min spend) with min 5 transactions/mo

- Up to 10% on Grab, Shopee, Dairy Farm Singapore & select UOB travel, 1% on utilities bills

- 3.33% rebate, up to S$100/quarter (S$1,000 min spend)

- 3.33% rebate, up to S$50/quarter (S$500 min spend)

- 0.03% rebate on all spend if no rebate earned for calendar year

- Up to 21.15% savings at Shell and 22.66% at SPC

- Annual fee: S$192.60 (first year- waived)

- 5% rebate on general spend, up to S$200/quarter (S$2,000 min spend) with min 5 transactions/mo

- Up to 10% on Grab, Shopee, Dairy Farm Singapore & select UOB travel, 1% on utilities bills

- 3.33% rebate, up to S$100/quarter (S$1,000 min spend)

- 3.33% rebate, up to S$50/quarter (S$500 min spend)

- 0.03% rebate on all spend if no rebate earned for calendar year

- Up to 21.15% savings at Shell and 22.66% at SPC

Best No-Fee Rebate Card for Daily Essentials: OCBC 365 Card

- Pros

- 6% rebate on dining, 3% on groceries, transport, utilities, online travel

- Fee waiver with S$10,000 annual spend

- Up to 22.1% fuel savings at Caltex, 20.2% at Esso

- Cons

- 0.3% rebate on general spend

- High S$800 minimum spend requirement

If you want to earn high cashback rates for your monthly bill spend and daily essentials, OCBC 365 Card is an excellent option that even comes with a fee-waiver. Cardholders earn 6% rebate on dining & online food delivery and 3% on groceries, land transport and travel bookings.

Even better, spend on telco (SingTel, StarHub, M1, MyRepbulic, Circles.Life) and electric (Senoko Energy, Sembcorp Power, Keppel Electric & more) also earns 3% cashback. Cardholders only need to spend S$800/month to access these rates, and can earn up to a lofty S$80/month. In comparison, other cards require stable spending at much higher levels to earn meaningful cashback, or have very low category caps (in fact, some cap recurring bill earnings at just S$1/month).

OCBC 365 Card also comes with a relatively easy fee-waiver. Cardholders only need to spend S$10,000/year (about S$833/month) to earn exemption from the S$192.6 fee, which is already waived 2 years. At this rate, cardholders would easily meet the minimum spend requirements as well. If you’re looking for a no-fee card that rewards all of your spend–including bills–OCBC 365 Card could very well be the right option for you.

- Annual fee: S$194.40 (automatic 2 years fee waiver with min annual spend of S$10,000)

- 6% rebate on local, overseas dining & online food delivery

- 3% rebate on local, overseas and online groceries

- 3% rebate on land transport, utilities (telco and electricity bills) & online travel

- 5% rebate on petrol (up to 22.1% fuel savings at Caltex and 20.2% with Esso)

- 0.3% cashback on all other spend

- Annual fee: S$194.40 (automatic 2 years fee waiver with min annual spend of S$10,000)

- 6% rebate on local, overseas dining & online food delivery

- 3% rebate on local, overseas and online groceries

- 3% rebate on land transport, utilities (telco and electricity bills) & online travel

- 5% rebate on petrol (up to 22.1% fuel savings at Caltex and 20.2% with Esso)

- 0.3% cashback on all other spend

Rebate Credit Card for Essentials & Bill Pay: POSB Everyday Card

- Pros

- Benefits highly diversified spend with large food budgets

- Great fit for commuters seeking a convenient, an all-in-one card

- Cons

- Not suitable for consistent spend of S$2k+/mo

- Lacks travel rewards

- Has an annual fee

POSB Everyday Card is a great all-in-one rebate credit card that rewards daily essentials and even has ABT/SimplyGo capabilities. Cardholders can typically earn up to 10% cash back in categories such as online food delivery, dining, groceries, petrol, and personal care. Some but not all of these categories are merchant restricted.

POSB Everyday Cardholders also can typically earn 1% on telco and electricity bills with select vendors (Best Electricity, Geneco, Ohm, SP Group, Tuas Power, Union Power & more). This is great because many cards exclude bill pay from earning rewards. It is worth mentioning that earnings are capped at just S$1/month. Still, POSB Everyday Card is generally a great rebate card with top rates in key categories plus the added convenience of ABT/SimplyGo functionality.

- Annual fee: S$194.40 (first year - waived)

- 10% cash rebates on online food delivery (foodpanda, Deliveroo and WhyQ ) and 3% on other dining spend

- 5% cash rebates on online shopping (Amazon, Lazada, Qoo10, Shopee, RedMart, iHerb & Taobao)

- 3% cash rebates on dining spend

- 0.3% cash rebate on all other spend

- DBS Payment Plan: pay 0% interest, up to 24 months

- Annual fee: S$194.40 (first year - waived)

- 10% cash rebates on online food delivery (foodpanda, Deliveroo and WhyQ ) and 3% on other dining spend

- 5% cash rebates on online shopping (Amazon, Lazada, Qoo10, Shopee, RedMart, iHerb & Taobao)

- 3% cash rebates on dining spend

- 0.3% cash rebate on all other spend

- DBS Payment Plan: pay 0% interest, up to 24 months

Best Credit Card for Online Bill Pay: HSBC Revolution Card

- Pros

- Great rewards on local dining and entertainment

- Online shopping perks

- No-fee card

- Cons

- Lacks rewards for frequent travellers who spend large amounts overseas

- Not suitable for low budgets

HSBC Revolution Card is the best miles-earning credit card option on the market if you’re a local social spender and pay most of your bills online. Cardholders earn 2 miles per S$1 on local dining & entertainment as well as for online spend–including insurance premiums and bill pay. This is equal to about 2% rebate in value, and there’s no minimum spend requirement, meaning you can easily earn on payments no matter the size of your overall monthly budget. Other cards require S$800+ to earn at similar rates.

In addition, HSBC Revolution Card also comes with a fee-waiver. After just S$12,500 annual spend (about S$1,042/month), cardholders are exempt from the S$160.5 fee. Ultimately, if you spend socially and locally and prefer online bill pay, HSBC Revolution Card is one of the best cards on the market.

- No annual fee

- Earn up to 4 miles, equivalent to up to 10X reward points or up to 2.5% cashback for every S$1 spent

- Points can be redeemed for miles through Mileage Programme in blocks of 10,000 Points for 4,000 miles

- Receive complimentary access to the ENTERTAINER with HSBC app, with over 1,000 1-for-1 deals on dining, lifestyle and travel worldwide

- T&Cs apply. SGD deposits are insured by up to S$75K by SDIC.

- No annual fee

- Earn up to 4 miles, equivalent to up to 10X reward points or up to 2.5% cashback for every S$1 spent

- Points can be redeemed for miles through Mileage Programme in blocks of 10,000 Points for 4,000 miles

- Receive complimentary access to the ENTERTAINER with HSBC app, with over 1,000 1-for-1 deals on dining, lifestyle and travel worldwide

- T&Cs apply. SGD deposits are insured by up to S$75K by SDIC.

Best Bill Pay Rebates for Low Spenders: Maybank Platinum Visa Card

- Pros

- Great starter card for young adults

- Good fit for budgets between S$300 and S$500/month

- S$80 annual fee

- Cons

- Few extra perks

- Doesn't award specialised spend (ie dining, shopping)

If you have a relatively low budget and minimum requirements are keeping you from earning cashback, consider Maybank Platinum Visa Card. With just S$300 monthly spend, you can earn at 3.33% up to S$30/quarter–or S$120/year. Alternative cards offer base rates of about 0.3% at this spend level, which only adds up to S$3.6/year.

Maybank Platinum Visa Card also rewards recurring bill payments, so even if you’re looking for a credit card just to pay bills with, this is likely your best option. Additionally, the S$20.0 quarterly fee is waived 3 years, and then simply with card use. Ultimately, if you have a limited budget, you can make the most of your bill pay and earn no-fee cashback with Maybank Platinum Visa Card.

- Annual fee: S$80 (3 years fee waiver)

- Subsequently quarterly service fee is waived w/ card use at least 1x/quarter

- Up to 3.33% on all local and foreign currency spend

- $30 quarterly rebate with at least S$300 monthly spend

- S$100 quarterly rebate with at least S$1,000 monthly spend

- Free travel insurance

- Annual fee: S$80 (3 years fee waiver)

- Subsequently quarterly service fee is waived w/ card use at least 1x/quarter

- Up to 3.33% on all local and foreign currency spend

- $30 quarterly rebate with at least S$300 monthly spend

- S$100 quarterly rebate with at least S$1,000 monthly spend

- Free travel insurance

Best for Easy, Unlimited Bill Pay Rebates: UOB Absolute Cashback

- Pros

- Unlimited cashback

- No min, caps or exclusions

- American Express Card privileges

- Cons

- Low cashback rate for smaller budgets

- Annual fee

UOB Absolute Cashback Card offers 1.7% cashback on just about any purchase or payment you put on it, with no minimum spend and no reward limits. While the rate is lower than other cards we feature, UOB Absolute Cashback stands out as a very easy-to-use option where you won't need to keep track of your monthly spending to get the most value from the credit card.

Besides being so flexible, UOB Absolute Cashback gives you certain American Express Card benefits such as discounts of up to 50% at certain restaurants, shops and hotels. It also offers petrol discounts of 20.8% at Shell stations and up to 24% at SPC. These features can help you save money in areas beyond just bill pay, which further offsets UOB Absolute Cashback's lower cashback rate.

- Annual fee: S$194.40 (first year - waived)

- 1.7% unlimited cashback

- No min spend and no spend exclusions

- Earn cashback on insurance payments, school fees, wallet top-ups

- Cashback also available on healthcare, utilities and telco bills and rental payments

- Annual fee: S$194.40 (first year - waived)

- 1.7% unlimited cashback

- No min spend and no spend exclusions

- Earn cashback on insurance payments, school fees, wallet top-ups

- Cashback also available on healthcare, utilities and telco bills and rental payments

Best Credit Cards for High Spenders & Recurring Monthly Bill Pay

If you’re a high spender and want to avoid limits on your earning potential, the following cards are some of the best options on the market, and even reward bill pay.

Best Rebate Card for Affluent HSBC Advance Customers: HSBC Advance Card

- Pros

- Great fit for budgets between S$2,000 and S$8,000/month

- Easy, low-maintenance cashback

- Cons

- Lacks travel perks

- Doesn't fit highly specialised spend behaviors

If you spend S$3,500/month, you can earn up to S$1,500/year with HSBC Advance Card–one of the best flat rebate credit cards on the market. Cardholders with Advance banking accounts earn 3.5% cashback on all spend after a S$2,000 minimum (2.5% if below), up to S$125/month. This includes for monthly recurring bill payments. Even more, HSBC Advance customers are exempt from the annual fee.

While great for Advance customers, HSBC Advance Card is a bit less competitive for non-customers. These cardholders earn 2.5% cashback after S$2,000 spend (1.5% if below), up to S$70/month. They also must pay a S$180.0 fee, though it’s waived with S$12,500 annual spend. Even non-customers can earn on bills, however, making HSBC Advance Card an excellent option if your a higher spender–though we’d definitely recommend checking to see if you qualify for an HSBC Advance account.

- Annual fee: S$194.40 (first year- waived)

- 2.5% base cashback when you spend above SGD2,000

- 1.5% base cashback with no minimum spend

- 1% bonus cashback on your eligible credit card spending if you are HSBC Everyday Global Account holder and qualified for the HSBC Everyday+. T&Cs apply. SGD deposits are insured by up to S$75K by SDIC

- Receive complimentary access to the ENTERTAINER with HSBC app, with over 1,000 1-for-1 deals on dining, lifestyle and travel worldwide

- Annual fee: S$194.40 (first year- waived)

- 2.5% base cashback when you spend above SGD2,000

- 1.5% base cashback with no minimum spend

- 1% bonus cashback on your eligible credit card spending if you are HSBC Everyday Global Account holder and qualified for the HSBC Everyday+. T&Cs apply. SGD deposits are insured by up to S$75K by SDIC

- Receive complimentary access to the ENTERTAINER with HSBC app, with over 1,000 1-for-1 deals on dining, lifestyle and travel worldwide

Best Unlimited Cashback Card with Amex Benefits: American Express True Cashback Card

- Pros

- Great Amex perks

- Straightforward, easy-to-use card

- Cons

- Not suitable for lower budgets

- Rewards general spend only

- None currently available

High spenders often feel limited by typical, capped cashback credit cards. American Express True Cashback Card offers unlimited earning potential, including for recurring bill payments. Cardholders earn 1.5% flat cashback on all of their spend, boosted to 3% (up to S$150) during the first 6 months. No other unlimited card offers such a lucrative welcome deal. Even better, cardholders enjoy signature Amex benefits, like Global Assist and American Express Selects dining & lifestyle deals. True Cashback card-specific promotions often feature wedding and travel-related discounts. Overall, if you’re a high spender and Amex loyalist, American Express True Cashback Card is an excellent option for rewards on bill pay.

- Annual fee: S$171.20 (first year - waived)

- Get 1.5% cashback on all eligible spend, with no min. spend required and no cap

- Get double the cashback at 3% on first S$5,000 spent within first 6 months

- Free travel insurance up to S$350,000 when you purchase travel tickets with this card

- Annual fee: S$171.20 (first year - waived)

- Get 1.5% cashback on all eligible spend, with no min. spend required and no cap

- Get double the cashback at 3% on first S$5,000 spent within first 6 months

- Free travel insurance up to S$350,000 when you purchase travel tickets with this card

Best Miles Credit Cards for Paying Monthly Recurring Bills

Several travel cards offer miles for paying monthly recurring bills. We’ve identified the best and reviewed them below.

Best Miles for Young SIA Loyalists: KrisFlyer UOB Credit Card

- Pros

- 3 mi per S$1 on SIA, SilkAir, Scoot & KrisShop

- Up to 3 mi on dining, transport, online shopping & travel

- Expedited KF Elite Silver status, Scoot privileges

- 10,000 annual bonus renewal miles

- Cons

- Just 1.2 mi on non-category overseas spend

- No lounge access perks

- No spend-based fee-waiver

If you're a young budget-conscious traveller who also wants to earn miles on utilities bills, you may want to consider KrisFlyer UOB Card. Cardholders earn 1.2 miles per S$1 spend on general local and overseas transactions, including utilities. This rate is elevated to 3 miles per S$1 for SIA brand transactions (SIA, Scoot, SilkAir, KrisShop) and then–after S$500 annual SIA spend–for dining & online food delivery, transport (including BUS and MRT) and online fashion shopping & travel bookings. Given these spend categories, KF UOB Card is a great match for young adults who tend to have a higher concentration of spend in these areas.

KF UOB Card's perks are also ideal for a budget traveller. Cardholders enjoy privileges with Scoot, SIA's low-cost carrier, such as baggage allowance upgrades, priority check-in & boarding, free standard seat selection and booking flexibility waivers. Other perks include S$15 worth of Grab rides to and from Changi Airport, another S$15 towards ChangiWiFi, and a S$20 rebate at KrisShop after a S$100 nett transaction. Given the card's 10,000 annual miles bonus (worth about S$100)–which offsets the S$192.6 annual fee–KF UOB Card is also very affordable. If you're willing to commit to flying with SIA and want access to practical perks, you should definitely consider KrisFlyer UOB Card.

- Annual fee: S$192.60 (first year - waived

- 3.0 KF miles/S$1 on spend with SIA brands (SIA, SilkAir, Scoot, KrisShop)

- 3.0 KF miles/S$1 on dining & food delivery, online shopping & travel and transport–with min. S$800 annual spend on SIA brands

- 1.2 KrisFlyer miles/S$1 on general spend, locally & overseas

- 10,000 annual bonus renewal miles

- Annual fee: S$192.60 (first year - waived

- 3.0 KF miles/S$1 on spend with SIA brands (SIA, SilkAir, Scoot, KrisShop)

- 3.0 KF miles/S$1 on dining & food delivery, online shopping & travel and transport–with min. S$800 annual spend on SIA brands

- 1.2 KrisFlyer miles/S$1 on general spend, locally & overseas

- 10,000 annual bonus renewal miles

Beginner Travel Card: American Express Singapore Airlines KrisFlyer Card

- Pros

- Easy-to-use miles card

- No conversions & transfer fees

- Great rewards with Singapore Airlines

- Cons

- Not easy to maximise miles

- Lacks airline/travel rewards aside from SIA

American Express Singapore Airlines KrisFlyer Card offers travellers KrisFlyer miles on nearly all of their spend, including on most monthly bill payments. Cardholders earn 1.1 miles per S$1 spend (including on bill pay), 2 miles overseas in June & December, 2 miles for spend with SingaporeAir, SilkAir and KrisShop, and 3.1 miles on Grab transactions. These rates definitely reward SIA loyalists. Rewards are also earned directly as KrisFlyer Miles, so there’s no need for conversions or transfer fees. Ultimately, if you’re looking for an easy-to-use miles credit card that rewards for bill-pay, Amex SIA KF Card is worth considering.

- Annual fee: S$176.55 (first year- waived)

- 1.1 miles per S$1 local & overseas spend, 2 mi overseas in June & December only

- 2 miles per S$1 spend on SingaporeAir online & app, SilkAir, KrisShop in-flight & online

- 3.1 miles per S$1 spend on Grab transactions (up to 620 mi/mo)

- Free travel insurance

- Hertz Gold Plus Rewards & Amex Selects Privileges

- Annual fee: S$176.55 (first year- waived)

- 1.1 miles per S$1 local & overseas spend, 2 mi overseas in June & December only

- 2 miles per S$1 spend on SingaporeAir online & app, SilkAir, KrisShop in-flight & online

- 3.1 miles per S$1 spend on Grab transactions (up to 620 mi/mo)

- Free travel insurance

- Hertz Gold Plus Rewards & Amex Selects Privileges

Best Miles Card for Travel Membership Upgrades: American Express Singapore Airlines KrisFlyer Ascend Card

- Pros

- Luxury travel perks

- Great rewards with Singapore Airlines

- Elite travel memberships

- Cons

- Not suitable for high overseas spend

- High annual fee

American Express Singapore Airlines KrisFlyer Ascend Card is a great credit card option for people seeking unique travel perks without having to pay an exorbitant annual fee. Cardholders earn 1.2 miles/S$1 general spend, 2 miles with SIA brands and overseas in June & December, and 3.2 miles on Grab transactions. What differentiates Amex SIA KF Ascend Card is that it provides cardholders with access to exclusive membership upgrades, including Hilton Honors Silver, KrisFlyer Elite Gold, and Hertz Gold Plus. These perks are complemented by 4 free lounge visits/year, 1 free hotel night and free travel insurance.

Even with these exclusive travel benefits, Amex SIA KF Ascend Card costs just S$337.05 in annual fees. This is far lower than the S$500+ charged by travel cards with comparable perks. It's also helpful that even spend on insurance payments is eligible for rewards. Overall, if you're looking for exclusive perks and upgrades to improve your travel experience, you may want to consider Amex SIA KF Ascend–especially if you're hoping to save on an annual fee.

- Annual fee: S$337.05

- 1.2 miles per S$1 local & overseas spend, 2 miles overseas in June & December only

- 2 miles per S$1 spend on SingaporeAir online & app, SilkAir, KrisShop in-flight & online

- 3.2 miles per S$1 spend on Grab transactions (up to 640 mi/mo)

- 4 free lounge visits/year, free annual hotel night, travel insurance

- Access to Hilton Honors Silver & Krisflyer Elite Gold status

- Annual fee: S$337.05

- 1.2 miles per S$1 local & overseas spend, 2 miles overseas in June & December only

- 2 miles per S$1 spend on SingaporeAir online & app, SilkAir, KrisShop in-flight & online

- 3.2 miles per S$1 spend on Grab transactions (up to 640 mi/mo)

- 4 free lounge visits/year, free annual hotel night, travel insurance

- Access to Hilton Honors Silver & Krisflyer Elite Gold status

Best for Rapid Mile Accumulation: UOB PRVI Miles American Express Card

- Pros

- Great for rapid miles accrual

- Awards high spend on airlines & hotels

- Annual fee waiver with Amex card

- Cons

- Doesn't fit infrequent travellers with mostly local budgets

- Lacks luxury perks & privileges

If you’re an above average spender, UOB PRVI Miles American Express Card is the best way to rapidly accumulate miles for spend, including on bill pay, and even comes with a fee-waiver. Cardholders earn 1.4 miles per S$1 locally, 2.4 miles overseas, and 6 miles with major airlines & hotels–some of the highest rates on the market. In fact, travel credit cards with similar rates have annual fees of S$400+.

UOB PRVI Miles Card, on the other hand, has a S$256.8 fee which is waived with S$50,000 annual spend. At this spend level, cardholders are not only exempt from the fee–they also receive 20,000 bonus miles (worth S$200). Cardholders also receive free travel insurance and airport transfers. Ultimately, if you spend about S$4,200/month and want to rapidly accrue no-fee miles, UOB PRVI Miles Card is definitely the card for you.

- Annual fee: S$259.20 (first year- waived)

- Annual fee waived and 20,000 bonus annual renewal miles (worth S$200) with min annual spend of S$50,000

- 1.4 miles/ S$1 local spend, 2.4 miles/S$1 overseas

- 6 miles/S$1 spend on Expedia, Agoda and UOB Travel

- Complimentary airport transfers & free travel insurance

- Can choose to redeem for miles or cashback

- Annual fee: S$259.20 (first year- waived)

- Annual fee waived and 20,000 bonus annual renewal miles (worth S$200) with min annual spend of S$50,000

- 1.4 miles/ S$1 local spend, 2.4 miles/S$1 overseas

- 6 miles/S$1 spend on Expedia, Agoda and UOB Travel

- Complimentary airport transfers & free travel insurance

- Can choose to redeem for miles or cashback

Best Card for Cashback + Miles: HSBC Visa Platinum Card

- Pros

- Great local dining & groceries rewards

- Suitable for moderate budgets (S$1,600+/month)

- Cashback & miles rewards

- Cons

- Limited miles & travel perks

- Not suitable for frequent online shoppers

HSBC Visa Platinum Card is one of the few options on the market that allows cardholders to earn both cashback and miles. After a S$600 minimum, cardholders earn 5% rebate on local dining, groceries & petrol. They also earn 0.4 miles per S$1 general spend, with no minimum requirement. While this rate may be low, it does include recurring bill payments. In addition, cardholders can earn up to S$250/quarter, and can avoid the S$180.0 fee with S$12,500 annual spend. Ultimately, HSBC Visa Platinum Card stands out for its flexibility, while also offering miles for bill pay.

- Annual fee: S$194.40 (waived for two years)

- 5% cash rebate on local dining and groceries (food deliveries and online groceries included)

- 0.4 miles per S$1 general spend, unlimited

- Earn up to 17% instant discount plus 5% cash rebate on fuel spending at Caltex and Shell stations

- Receive complimentary access to the ENTERTAINER with HSBC app, with over 1,000 1-for-1 deals on dining, lifestyle and travel worldwide

- T&Cs apply. SGD deposits are insured by up to S$75K by SDIC.

- Annual fee: S$194.40 (waived for two years)

- 5% cash rebate on local dining and groceries (food deliveries and online groceries included)

- 0.4 miles per S$1 general spend, unlimited

- Earn up to 17% instant discount plus 5% cash rebate on fuel spending at Caltex and Shell stations

- Receive complimentary access to the ENTERTAINER with HSBC app, with over 1,000 1-for-1 deals on dining, lifestyle and travel worldwide

- T&Cs apply. SGD deposits are insured by up to S$75K by SDIC.

Summary of Best Cards for Paying Recurring Monthly Bills 2024

Below, we've summarized our picks for the best credit cards for paying recurring monthly bills in 2024.

| Card | Best for... | Annual Fee | |

|---|---|---|---|

| UOB One | Best Flat Rebate | S$192.6 | |

| OCBC 365 | Everyday Spend, Easy Waiver | S$192.6 (waiver) | |

| HSBC Revolution | Social & Online Spend | S$160.5 (waiver) | |

| Maybank Platinum Visa | Low Spenders | S$80.0 (waiver) | |

| HSBC Advance | Affluent Advance Customers | S$180.0 (waiver) | |

| UOB PRVI Miles | Rapid Miles | S$256.8 (waiver) | |

| HSBC Visa Platinum | Cashback + Miles | S$192.6 |

| Card | Best for... | Annual Fee | |

|---|---|---|---|

| UOB One | Best Flat Rebate | S$192.6 | |

| OCBC 365 | Everyday Spend, Easy Waiver | S$192.6 (waiver) | |

| HSBC Revolution | Social & Online Spend | S$160.5 (waiver) | |

| Maybank Platinum Visa | Low Spenders | S$80.0 (waiver) | |

| HSBC Advance | Affluent Advance Customers | S$180.0 (waiver) | |

| UOB PRVI Miles | Rapid Miles | S$256.8 (waiver) | |

| HSBC Visa Platinum | Cashback + Miles | S$192.6 |

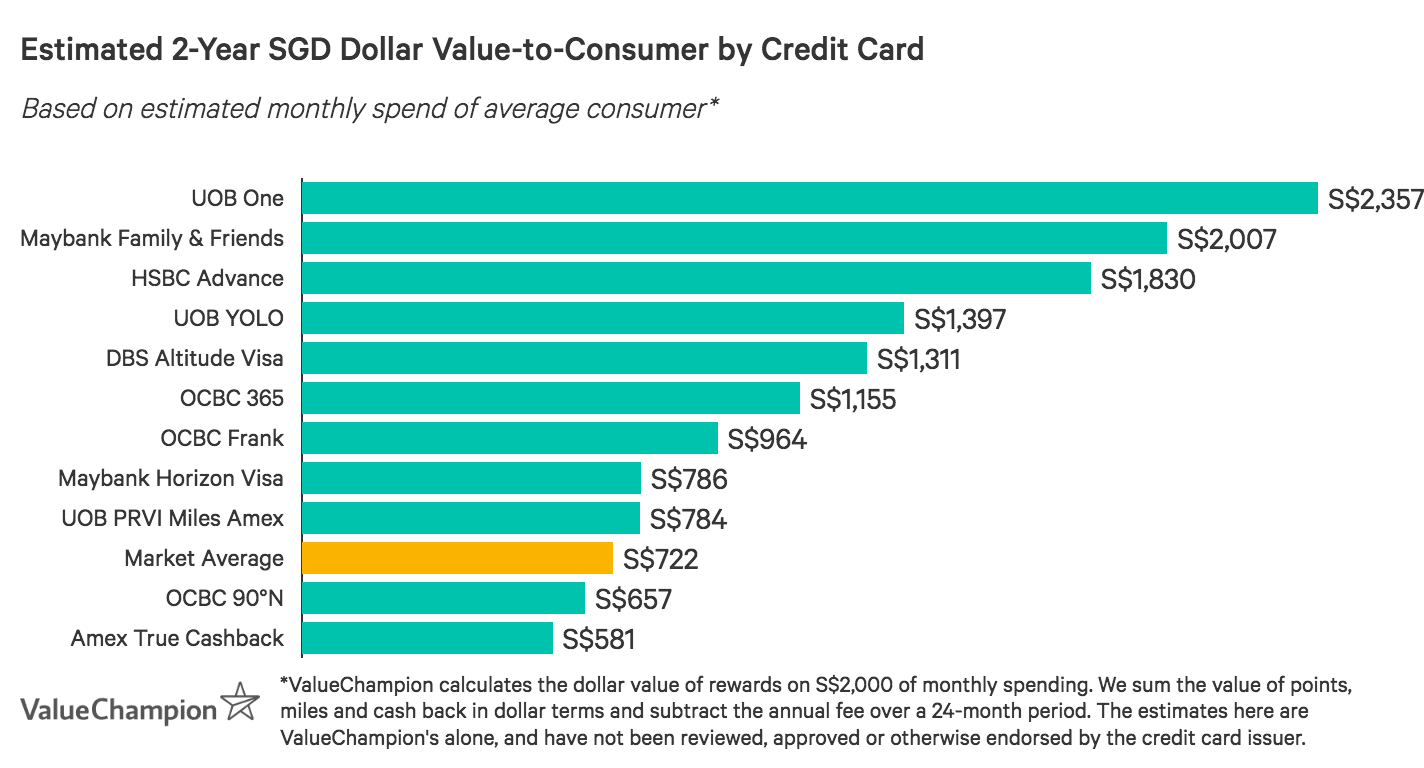

Compare the Best Credit Cards for Monthly Bills by Dollar Value

To help you find the best credit card for monthly recurring bill payments, we have prepared a chart below organizing credit cards by 2-year dollar value*. We have estimated an average Singaporean's monthly expenditure patterns through research to model out likely savings from credit cards. You should note that the dollar value can heavily depending on your spending habits, so make sure to read through each card's review and see if it fits your monthly budget. There are also other "intangible" benefits like complimentary travel insurance and free access to airport lounges whose values are difficult to quantify but nevertheless incredibly valuable to some consumers.

Footnotes

*ValueChampion calculates the dollar value of rewards based on S$2,000 of monthly spending. We sum the value of points, miles and cashback in dollar terms and subtract the annual fee over a 24-month period. The estimates here are ValueChampion's alone, and have not been reviewed, approved or otherwise endorsed by the credit card issuer.

Read More:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.