Best Credit Cards for Hospital Bills 2024

Whether you're dealing with big doctors' bills right now or regularly spend on your health, you may be interested in a credit card that offers rewards for medical spend. Most credit cards actively exclude hospital spend from earning rewards. So, to make things easier, our experts scoured the terms & conditions of 100+ cards in Singapore to find which actually do provide cash rebates or miles.

- UOB Absolute Cashback: Unlimited 1.7% cashback on all spend

- SC Unlimited Cashback: 1.5% unlimited rebate + transport perks

- Amex True Cashback: Unlimited 1.5% rebate + Amex benefits

- HSBC Advance: Up to 3.5% cashback capped at S$300/month

- OCBC Cashflo: Rewards for split payments, no processing fee

- SC SingPost Spree: 3% rebate online overseas & vPost transactions

- HSBC Revolution: 4 miles per S$1 spent online and on contactless payments

- CIMB Platinum MasterCard: 10% rebate on wine and dine, transport, petrol, health and travel, capped at S$100/month

- POSB Everyday: Rebates up to 10% in Singapore

- Citi SMRT: 5% everyday rebates w/S$500 min spend

- BOC Family: Up to 10% on dining, 3% on transit, medical & more

- SC Visa Infinite X: Bonus S$6,000 w/ S$200k fund placement

- SC Visa Infinite: 3 miles per S$1 overseas, rewards for tax-pay

Compare the Best Credit Cards for Making Medical Payments by Dollar Value

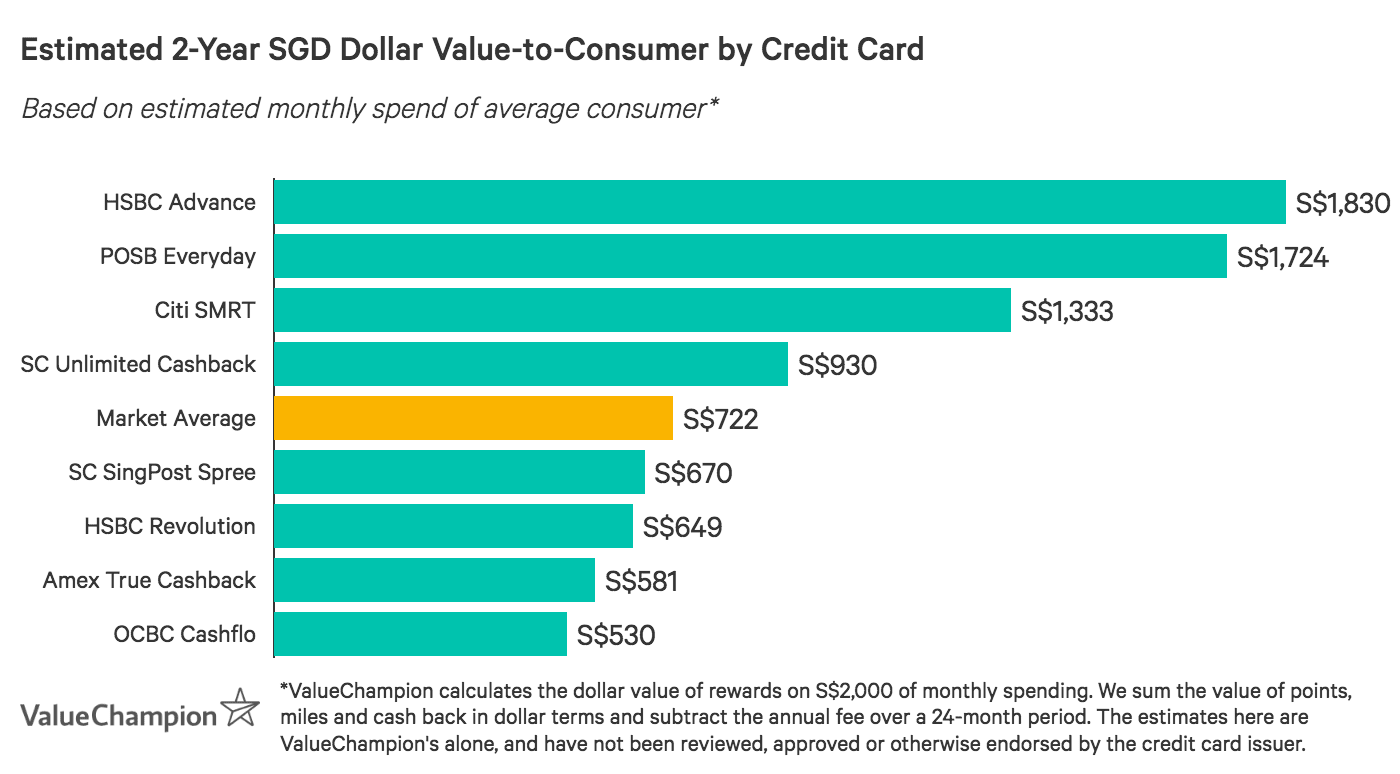

Based on an average monthly spend of S$2,000, we analysed the best credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Compare the Best Credit Cards for Making Medical Payments by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

How to Earn Credit Card Rewards on Hospital Bills

Medical bills can be quite expensive and are sometimes difficult to pay off all at once. Facing such a large bill can certainly be daunting, but also presents an opportunity to earn significant cashback or miles. Additionally, some credit cards offer 0% interest instalment plans which allow cardholders to make payments on big bills over time at no extra cost.

While there are hundreds of credit cards in Singapore, few cards reward medical payments. Medical bills, including those from public hospitals and polyclinics, are often nested under "government services," which are often excluded from rewards calculations. After carefully reviewing credit card terms and conditions from across the market, we've picked out a handful of cards that offer cashback or miles for medical payments while also providing competitive rewards for other spending.

Best Credit Cards for Rebates on Big Hospital Bills

These cards help you translate big bill payments into big cashback rewards, thanks to their unlimited cashback features.

UOB Absolute Cashback Card: Unlimited Rebates, No Minimums and No Exclusions

| |

Here is why UOB Absolute Cashback Card is one of the best credit cards for paying large hospital bills. If you need to pay large medical or hospital bills, chances are you’ll feel limited by typical capped cashback cards. UOB Absolute offers an unlimited 1.7% cashback on all of your spend, no matter how much or how little. It also comes with none of the typical exclusions that competing cards have, so you can be sure that you'll earn the full rebate on every transaction.

| |

|

|

Here is why UOB Absolute Cashback Card is one of the best credit cards for paying large hospital bills. If you need to pay large medical or hospital bills, chances are you’ll feel limited by typical capped cashback cards. UOB Absolute offers an unlimited 1.7% cashback on all of your spend, no matter how much or how little. It also comes with none of the typical exclusions that competing cards have, so you can be sure that you'll earn the full rebate on every transaction.

|

Standard Chartered Unlimited Cashback Card: Unlimited Rebates + SimplyGo

| |

Here is why Standard Chartered Unlimited Cashback Card is one of the best credit cards for paying large hospital bills. If you need to pay large medical or hospital bills, chances are you’ll feel limited by typical capped cashback cards. Standard Chartered Unlimited Cashback Card offers unlimited earning potential, so no matter how much you need to spend, you’ll continue earning a flat 1.5% cashback.

Another reason to consider SC Unlimited Cashback Card instead of other unlimited cards is for its excellent transport benefits. Not only is it SimplyGo compatible, it also offers up to 21% fuel savings with Caltex. While there’s a S$192.6 fee, it’s waived for 2 years, so you won’t need to worry about card costs when you’re paying your bills. Ultimately, SC Unlimited Cashback Card is the best option for paying big medical bills if you’re also interested in transport benefits. | |

|

|

Here is why Standard Chartered Unlimited Cashback Card is one of the best credit cards for paying large hospital bills. If you need to pay large medical or hospital bills, chances are you’ll feel limited by typical capped cashback cards. Standard Chartered Unlimited Cashback Card offers unlimited earning potential, so no matter how much you need to spend, you’ll continue earning a flat 1.5% cashback.

Another reason to consider SC Unlimited Cashback Card instead of other unlimited cards is for its excellent transport benefits. Not only is it SimplyGo compatible, it also offers up to 21% fuel savings with Caltex. While there’s a S$192.6 fee, it’s waived for 2 years, so you won’t need to worry about card costs when you’re paying your bills. Ultimately, SC Unlimited Cashback Card is the best option for paying big medical bills if you’re also interested in transport benefits. |

American Express True Cashback Card: Unlimited Cashback + Amex Benefits

|

|

Here is why American Express True Cashback Card is one of the best cashback credit cards for paying large hospital bills. American Express True Cashback Card is an excellent option for paying large hospital bills because of its unlimited 1.5% rewards rate, boosted to 3% during the first 6 months (up to S$150). This is perfect if you’re paying your medical bills currently, or in the near future. Additionally, cardholders enjoy perks like American Express Global Assist–which provides free English-speaking doctor referrals when overseas–and travel accident insurance, covering up to S$350,000 for injuries.

| |

|

|

|---|

|

|

Here is why American Express True Cashback Card is one of the best cashback credit cards for paying large hospital bills. American Express True Cashback Card is an excellent option for paying large hospital bills because of its unlimited 1.5% rewards rate, boosted to 3% during the first 6 months (up to S$150). This is perfect if you’re paying your medical bills currently, or in the near future. Additionally, cardholders enjoy perks like American Express Global Assist–which provides free English-speaking doctor referrals when overseas–and travel accident insurance, covering up to S$350,000 for injuries.

|

HSBC Advance Card: High Flat Rebate for Advance Customers

| |

Here is why HSBC Advance Card is one of the best credit cards for Advance customers in paying large hospital bills. If you’re open to an HSBC Advance account, you can quickly maximise rebates for medical spend with HSBC Advance Card. Customers spending at least S$2,000/month have the opportunity to earn an incredible 3.5% cashback rate on all spend, including on public and private hospitals spend. To earn 3.5% cashback, 2.5% base rate + 1% bonus rate, cardholders must spend at least S$2,000 and deposit a minimum of S$2,000 per month in fresh funds and charge at least five transactions to their account. With this bonus rate, monthly cashback is capped at S$300, which is S$3,600 per year in savings. The closest competitor only rewards spend at private hospitals and caps earnings at S$100/month.

| |

|

|

Here is why HSBC Advance Card is one of the best credit cards for Advance customers in paying large hospital bills. If you’re open to an HSBC Advance account, you can quickly maximise rebates for medical spend with HSBC Advance Card. Customers spending at least S$2,000/month have the opportunity to earn an incredible 3.5% cashback rate on all spend, including on public and private hospitals spend. To earn 3.5% cashback, 2.5% base rate + 1% bonus rate, cardholders must spend at least S$2,000 and deposit a minimum of S$2,000 per month in fresh funds and charge at least five transactions to their account. With this bonus rate, monthly cashback is capped at S$300, which is S$3,600 per year in savings. The closest competitor only rewards spend at private hospitals and caps earnings at S$100/month.

|

Best Credit Cards for 0% Instalment Medical Payments

If you can't pay off a big hospital bill all at once, consider these cards with 0% interest instalment plans.

OCBC Cashflo Card: Rebates on Instalment Payments

|

|

Here is why OCBC Cashflo Card is one of the best credit cards in Singapore for paying hospital bills with rebates on installments. OCBC Cashflo Card is the only rebate card on the market that allows consumers to net-earn on split payments. At a specific spend threshold determined by the cardholder, payments are automatically split into instalments across 3 or 6 months. Most instalment plans require call-ahead or retroactive applications, making OCBC Cashflo Card especially convenient. Even better, cardholders don’t need to pay a processing fee–other card plans charge up to 5% of the transaction amount.

This is especially great if you’re faced with large medical or hospital bills that you need to pay back over time. To put it in perspective, if you pay off a S$5,000 bill over 6 months, you’ll actually earn S$50 with OCBC Cashflo. If you paid this same bill with competitor cards, you’d either earn nothing at all, or potentially lose as much as S$140. In addition, OCBC Cashflo Card offers a fee-waiver with S$10,000 annual spend. If you’re splitting a big hospital bill into instalments, there’s no better option than OCBC Cashflo Card. | |

|

|

|---|

|

|

Here is why OCBC Cashflo Card is one of the best credit cards in Singapore for paying hospital bills with rebates on installments. OCBC Cashflo Card is the only rebate card on the market that allows consumers to net-earn on split payments. At a specific spend threshold determined by the cardholder, payments are automatically split into instalments across 3 or 6 months. Most instalment plans require call-ahead or retroactive applications, making OCBC Cashflo Card especially convenient. Even better, cardholders don’t need to pay a processing fee–other card plans charge up to 5% of the transaction amount.

This is especially great if you’re faced with large medical or hospital bills that you need to pay back over time. To put it in perspective, if you pay off a S$5,000 bill over 6 months, you’ll actually earn S$50 with OCBC Cashflo. If you paid this same bill with competitor cards, you’d either earn nothing at all, or potentially lose as much as S$140. In addition, OCBC Cashflo Card offers a fee-waiver with S$10,000 annual spend. If you’re splitting a big hospital bill into instalments, there’s no better option than OCBC Cashflo Card. |

Standard Chartered SingPost Spree: Online Overseas Shopping Rebates

|

|

Here is why Standard Chartered SingPost Spree Card is one of the best credit cards in Singapore for paying hospital bills online. Standard Chartered SingPost Spree Card is great for online hospital bill payments in instalments. Cardholders can access EasyPay, which is a 0% interest instalment plan that splits transactions of at least S$500 across up to 12 months. Unlike many other plans, EasyPay rewards payments on the plan upfront. In other words, if you split a large hospital bill into instalments, you can pay them back over a year, but earn cashback on the entire bill right away. There is a 5% processing fee, however.

| |

|

|

|---|

|

|

Here is why Standard Chartered SingPost Spree Card is one of the best credit cards in Singapore for paying hospital bills online. Standard Chartered SingPost Spree Card is great for online hospital bill payments in instalments. Cardholders can access EasyPay, which is a 0% interest instalment plan that splits transactions of at least S$500 across up to 12 months. Unlike many other plans, EasyPay rewards payments on the plan upfront. In other words, if you split a large hospital bill into instalments, you can pay them back over a year, but earn cashback on the entire bill right away. There is a 5% processing fee, however.

|

Best No-Fee Credit Cards for Paying Hospital Bills

No-fee credit cards are especially low-maintenance, allowing you to focus on your health rather than additional costs.

HSBC Revolution: Miles for Social Spend & Online Bills

| |

Here is why HSBC Revolution is one of the best no-fee credit cards in Singapore for paying hospital bills online. HSBC Revolution Card is the best miles-earning card for online payment of hospital bills, and even comes with an easy fee-waiver. Cardholders earn 2 miles per S$1 online spend, including online travel bookings, transit, and bill pay–private and public. There are no minimum spend requirements and no earning caps, which is great if you’re looking to use this card for more than just bills, and want to continue earning. On that note, cardholders also earn at this rate for spend on local dining & entertainment.

| |

|

|

Here is why HSBC Revolution is one of the best no-fee credit cards in Singapore for paying hospital bills online. HSBC Revolution Card is the best miles-earning card for online payment of hospital bills, and even comes with an easy fee-waiver. Cardholders earn 2 miles per S$1 online spend, including online travel bookings, transit, and bill pay–private and public. There are no minimum spend requirements and no earning caps, which is great if you’re looking to use this card for more than just bills, and want to continue earning. On that note, cardholders also earn at this rate for spend on local dining & entertainment.

|

CIMB Platinum MasterCard: Cashback on Medical, Transport & More

|

|

Here is why CIMB Platinum MasterCard is one of the best cashback credit cards in Singapore for paying medical expenses. CIMB Platinum MasterCard offers the highest cashback rate for medical expenses on the market. Cardholders earn 10% rebate on everything from doctors, dentists, optometrists, opticians and chiropractors to hospitals, nursing & personal care facilities, pharmacies and more. This spend category is individually capped at just S$20/month, however, and bills from polyclinics and government hospitals are excluded from earning rewards.

| |

|

|

|---|

|

|

Here is why CIMB Platinum MasterCard is one of the best cashback credit cards in Singapore for paying medical expenses. CIMB Platinum MasterCard offers the highest cashback rate for medical expenses on the market. Cardholders earn 10% rebate on everything from doctors, dentists, optometrists, opticians and chiropractors to hospitals, nursing & personal care facilities, pharmacies and more. This spend category is individually capped at just S$20/month, however, and bills from polyclinics and government hospitals are excluded from earning rewards.

|

Best Credit Cards for Health & Wellness Perks

These cards may not directly reward medical spend, they do offer perks that support overall wellness.

POSB Everyday Card: Rebates on Essentials & Personal Care

| |

Here is why POSB Everyday Card is one of the best credit cards in Singapore for paying essentials and personal healthcare. POSB Everyday Card is an excellent everyday card for families and comes with a few great wellness perks. First of all, cardholders receive 3% cashback on personal care from Watsons, as well as 3% on online shopping at Amazon.sg, Lazada, Qoo10, Shopee, RedMart and iHerb.

| |

|

|

Here is why POSB Everyday Card is one of the best credit cards in Singapore for paying essentials and personal healthcare. POSB Everyday Card is an excellent everyday card for families and comes with a few great wellness perks. First of all, cardholders receive 3% cashback on personal care from Watsons. Additionally, they have access to up to 15% off select local medical packages for health screening, dentistry, cardiology and more.

|

Citi SMRT Card: No Minimum Spend Requirement + Rebates on Essentials

|

|

Here is why Citi SMRT Card is one of the best non-minimum spend credit cards in Singapore for paying hospital bills. If you’re a young professional on a budget, consider Citi SMRT Card, which is one of the few cards on the market with no minimum spend requirement. Cardholders receive 5% rebate on groceries, 5% for online spend and 5% on Auto Top-Ups. In fact, Citi SMRT Card itself is EZ-Link compatible, making it a great choice for commuters.

| |

|

|

|---|

|

|

Here is why Citi SMRT Card is one of the best non-minimum spend credit cards in Singapore for paying hospital bills. If you’re a young professional on a budget, consider Citi SMRT Card, which is one of the few cards on the market with no minimum spend requirement. Cardholders receive 5% rebate on groceries, 5% for online spend and 5% on Auto Top-Ups. In fact, Citi SMRT Card itself is EZ-Link compatible, making it a great choice for commuters.

|

Best Rebate Credit Card for Paying Hospital Bills

It's possible to earn cashback directly from your hospital bills–check out the card below.

BOC Family Card: Everyday Cashback, Inc. for Transit & Medical

|

|

Here is why BOC Family Card is one of the best rebate credit cards in Singapore for paying hospital bills. BOC Family Card is an excellent everyday option for household spenders with largely practical budgets. Cardholders earn 10% rebate on dining & movies, 5% with Family Club merchants like Best Denki, Watsons & more, 3% on MRT trains and SBS/SMRT Buses, and 3% on local supermarkets, online retail and hospital bills. Each of these 4 category groupings are capped at S$25/month in rewards, encouraging diversified spending (skewed towards transit, groceries, online & medical spend). With the right spend distribution, cardholders can earn up to S$100/month.

| |

|

|

|---|

|

|

Here is why BOC Family Card is one of the best rebate credit cards in Singapore for paying hospital bills. BOC Family Card is an excellent everyday option for household spenders with largely practical budgets. Cardholders earn 10% rebate on dining & movies, 5% with Family Club merchants like Best Denki, Watsons & more, 3% on MRT trains and SBS/SMRT Buses, and 3% on local supermarkets, online retail and hospital bills. Each of these 4 category groupings are capped at S$25/month in rewards, encouraging diversified spending (skewed towards transit, groceries, online & medical spend). With the right spend distribution, cardholders can earn up to S$100/month.

|

Best Miles Credit Cards for Paying Hospital Bills

If you prefer miles to cashback rewards, consider these cards when paying your hospital bills.

Standard Chartered Visa Infinite X: Bonus Miles & Rewards for Medical Bills

| |

Here is why Standard Chartered Visa Infinite X Card is one of the best miles and rewards credit cards in Singapore for paying hospital bills. Standard Chartered Visa Infinite X Card is a great card for affluent travellers looking to immediately accrue a large amount of miles without expending a great deal of effort. In fact, cardholders who place S$300k fresh funds in a SC Priority Banking account receive an incredible 100,000 KrisFlyer bonus miles (worth S$10k when redeemed for business class tickets). Those who place S$800k receive 150,000 miles (worth S$15k) and Priority Private Banking customers who place S$1.5m receive 300,000 miles (worth S$30k). While only accessible to those who have extra funds on hand, this sign-up offer provides greater value-to-consumer than any other currently on the market.

| |

|

|

Here is why Standard Chartered Visa Infinite X Card is one of the best miles and rewards credit cards in Singapore for paying hospital bills. Standard Chartered Visa Infinite X Card is a great card for affluent travellers looking to immediately accrue a large amount of miles without expending a great deal of effort. In fact, cardholders who place S$300k fresh funds in a SC Priority Banking account receive an incredible 100,000 KrisFlyer bonus miles (worth S$10k when redeemed for business class tickets). Those who place S$800k receive 150,000 miles (worth S$15k) and Priority Private Banking customers who place S$1.5m receive 300,000 miles (worth S$30k). While only accessible to those who have extra funds on hand, this sign-up offer provides greater value-to-consumer than any other currently on the market.

|

Standard Chartered Visa Infinite: Top Miles Overseas & on Tax-Pay

| |

Here is why Standard Chartered Visa Infinite Card is one of the best miles credit cards in Singapore for paying hospital bills. Not only does Standard Chartered Visa Infinite Card reward medical and hospital bill payments, it does so at the highest miles rates on the market. Cardholders earn 1.4 miles per S$1 local spend and 3 miles overseas, and receive 35,000 welcome miles (worth S$350) just for signing up. Income tax payments, fixed investments, mortgage loans and savings accounts with SC also earn rewards–all of which are often excluded from earning by competitors.

| |

|

|

Here is why Standard Chartered Visa Infinite Card is one of the best miles credit cards in Singapore for paying hospital bills. Not only does Standard Chartered Visa Infinite Card reward medical and hospital bill payments, it does so at the highest miles rates on the market. Cardholders earn 1.4 miles per S$1 local spend and 3 miles overseas, and receive 35,000 welcome miles (worth S$350) just for signing up. Income tax payments, fixed investments, mortgage loans and savings accounts with SC also earn rewards–all of which are often excluded from earning by competitors.

|

Learn More About Selecting the Best Credit Card for You

Read More:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.