4 Ways to Avoid Losing Money As a Landlord

Renovations, accidental structural damage and noncompliant tenants are among the top fears of landlords. With the number of HDB rental applicants increasing 55% between 2011 and 2017, we can surmise that more and more homeowners are making the decision to rent out their properties in hopes of getting extra cash. However, it is important to address the potential financial risks that can come with becoming a landlord. The decision to become a landlord comes responsibilities beyond simply collecting the rent check every month. You also need to make your sure your flat is comfortable for your tenants, carry out repairs and make sure your tenants don't end up scamming you. Thus, while it can be a lucrative investment when everything goes according to plan, a nightmare tenant or property neglect can also result in significant financial loss. Below, we discuss 4 things you should do to avoid losing money while renting out your property.

Choose Your Tenants Carefully

One of the most important things you can do to prevent losing money on your rental property is to vet your tenants carefully. A responsible and respectful tenant will minimise the risk of damage and ensure that you receive on-time rent payments consistently. Since there has been an increase in the number of people searching for apartments in Singapore, you may feel overwhelmed with the number of potential tenants you'll need to vet in order to find out out the best one. However, you can avoid making the wrong decision by conducting background checks, checking work permits for foreign applicants and getting references from previous landlords.

You should take it as a warning sign that your tenant is trying to scam you if you notice your rent is appearing late or not at all without a proper excuse and false promises of payments. In this instance, it may be a better option to terminate your rental agreement early and suffer a couple months of lost income as you search for a new tenant (which can be recoverable with a good home insurance policy) as opposed to hoping that your current tenant will eventually pay you. Furthermore, you should remember you are legally allowed to evict a tenant after 14 days of nonpayment, meaning you don't have to put up with non-paying tenants for months on end.

Renovations: Know When to Invest and When to Cut Costs

Because the primary goal of landlords is to earn a profit from their property, new landlords may investing tens of thousands of dollars into fancy renovations in hopes of being able to charge higher rents for a faster ROI. However, not only is that not necessary, but going all out on renovations for a flat you'll be renting out can be expensive and financially risky. For example, interior design trends come and go, making it much more cost efficient to settle on a classic design. Second, renovations can be very costly, meaning you may have to take out a renovation loan. With these added costs, you may end up not breaking even, especially if you are paying a mortgage on both your home and your investment property.

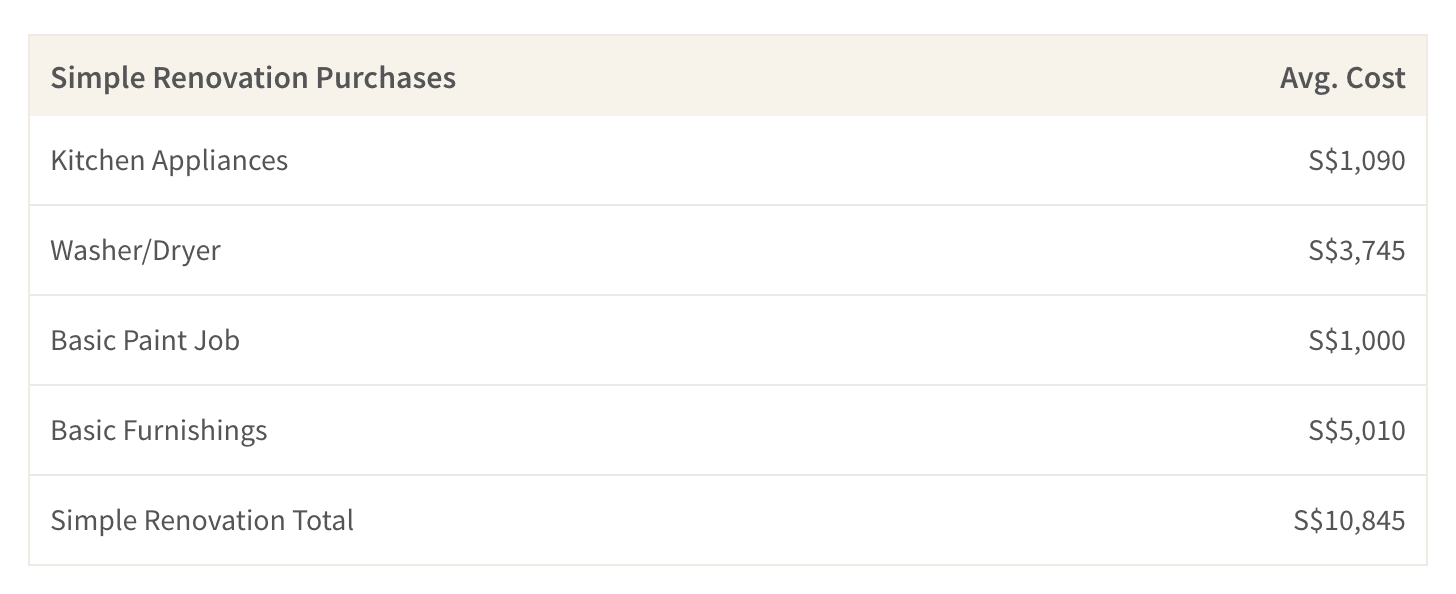

Thus, a more cost efficient method could be to keep a clean, classic property with basic but high quality amenities in the kitchen or bathroom. Since the quality of kitchens and bathrooms are very important for renters, focusing on those areas of the flat and maintaining a clean space can save you thousands of dollars compared to the average full-scale renovation cost of S$55,000. This means choosing to invest in high quality appliances rather than full-scale renovations can save you 80% on renovation costs and give you a reason to add an extra S$50-S$100 to your rent.

Get the Right Home Insurance

The right home insurance can be a landlord's best friend. Upgrading to a comprehensive home insurance plan with landlord-specific benefits can be a great way to protect yourself against rental income loss, damages and repairs. For instance, your home insurance can cover the damages provided they weren't due to neglect or purposeful damage made by the tenant if you are the responsible party for carrying out repairs and maintenance. You can also claim for emergency home repairs relating to plumbing, electricity, locksmithing and pest control. Furthermore, some insurance companies even offer a loss of rent benefit in your home insurance, saving you a couple of months of rental income in the event of default. However, you should always read the policy wording to make sure the reason for your loss of rent is covered.

Proactive Rather than Reactive When it Comes to Repairs

It is best to investigate immediately if your tenant raises concerns about broken appliances, fixtures or issues such as mould. For instance, if your tenant is complaining about a leaking refrigerator. Ignoring the problem and chalking it up to a fussy tenant will force you to shop or find a repairman under duress since it's an appliance that has to be fixed as soon as possible. Instead, you should investigate the issue as soon as possible to see whether the damage is significant enough to require replacement down the line. In this case you will have plenty of time to shop around and compare prices to get the best deal.

If the issue is something like mould—which requires a more comprehensive approach than a trip to a store—treating it early is even more important. Not only does mould pose health problems, but it can lead to thousands of dollars of damage if not treated properly. For instance, a great way to lose money is to paint over the mould. If you do this, the proteins in paint will feed the mould and exacerbate the problem. All of a sudden you lost half a month's rent and the problem is still not solved. Instead of ignoring the problem, pay for mould inspection to find the root of the problem and install the necessary measures to prevent it from spreading. You can also purchase mould removers for around S$10-S$15 for minor mould problems.

What Not to Do

Just as there are things you should to do as a landlord to minimise the risk of financial loss, there are also actions that you should avoid. For instance, don't refuse to give back your tenant's security deposit because of slight natural wear and tear in the apartment. Most tenants want their security deposit back to pay for their next rental and will thus put in effort to patch up damage before leaving. Furthermore, a savvy tenant will fight back and sue you for refusing to give back their deposit if your complaints are invalid (grease on a stove is in no way a valid reason to withhold a security deposit). Considering legal fees are not cheap in Singapore, this can lead to an otherwise avoidable loss of hundreds of dollars.

Instead, you should avoid being a towering figure of authority over your tenant and focus on being amicable and trustworthy. A tenant who knows they can come to you when they have problems can lead to an honest tenant-landlord relationship. They'll also be less likely to lie about things that need repairs (or worse, attempt to hide them until you discover the damage after the leave) and let you know if they are worried about potential financial problems. Furthermore, they may even recommend you to their friends, reducing the time you'll need to spend looking for tenants after they leave. In short, you should just treat your tenants the way you'd want to be treated.

Are you a landlord or tenant? If you had an interesting experience you want to share about Singapore's rental market, we'd love to hear from you: [email protected]

Anastassia is a Senior Research Analyst at ValueChampion Singapore, evaluating insurance products for consumers based on quantitative and qualitative financial analysis. She holds degrees in Economics and International Business Management and her prior working experience includes work in the capital markets sector. Her analyses surrounding insurance, healthcare, international affairs and personal finance has been featured on AsiaOne, Business Insider, DW, Vice, Her World, Asia Insurance Review, the Australian Institute of International Affairs and more.