DBS Live Fresh vs. POSB Everyday Credit Card Comparison 2022

If you're looking for a new cashback card, you may be already be considering DBS Live Fresh Card or POSB Everyday Card. After all, both are quite well-known within Singapore and offer cardholders the opportunity to earn rewards for nearly all of their spend. These cards are actually quite different, however, each with its own strengths and weaknesses. We've closely analysed the rewards rates, perks and fees for both of these options to help you determine which might be better for you.

- Details of rebate system & structure

- General & boosted cashback rates

- Minimum spend requirements & monthly rewards caps

- Maximum potential annual earnings

- Travel insurance offerings

- Current petrol promotions & savings

- SimplyGo & mobile pay compatibility

- Extra rebate programmes & card-specific privileges

- Minimum age & minimum income requirements

- Annual fees, spend-based waivers & sign-on bonuses

- Foreign transaction fees

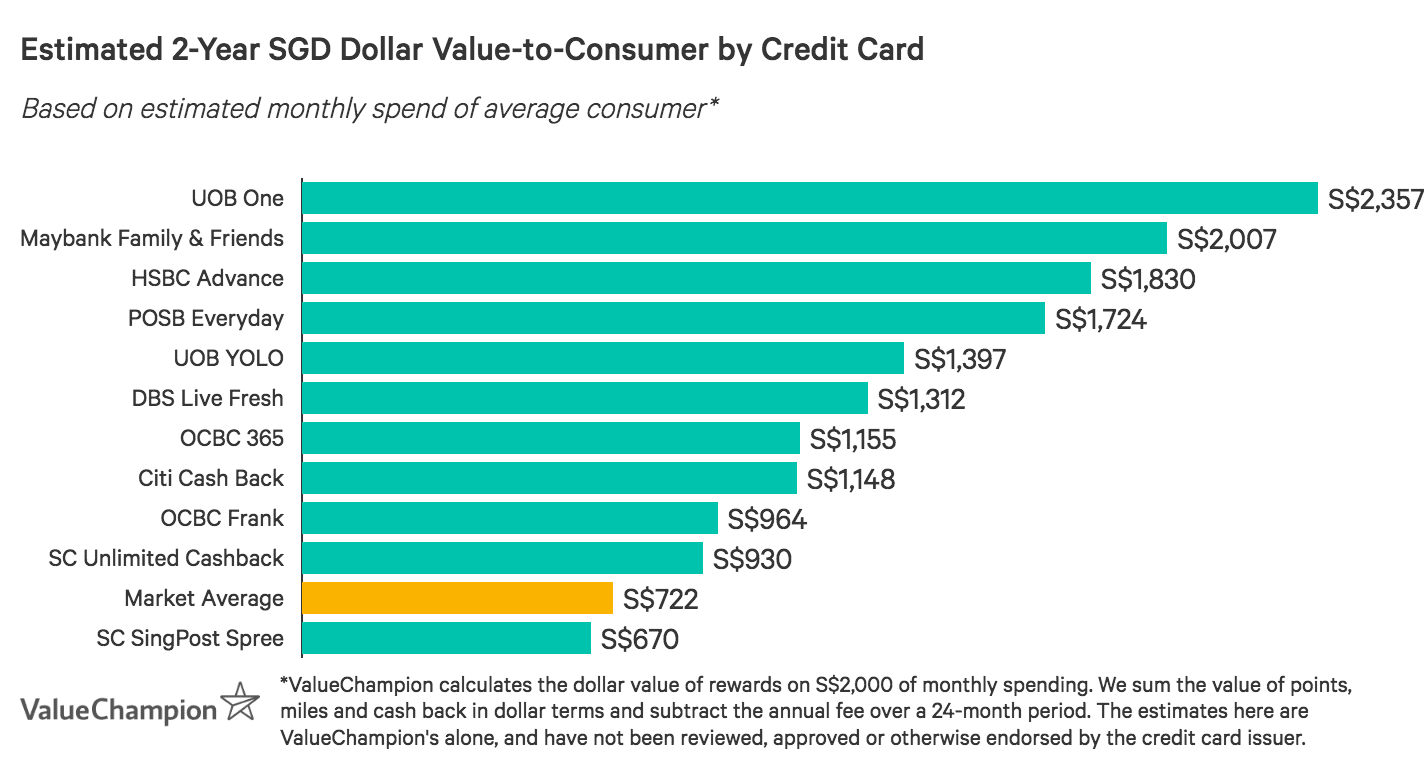

Comparison of Competitive Rebate Cards in Singapore by Dollar Value

Based on an average monthly spend of S$2,000, we analysed some of the most competitive rebate cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Comparison of Competitive Rebate Cards in Singapore by Dollar Value

Based on an average monthly spend of S$2,000, we analysed some of the most competitive rebate cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Overview: DBS Live Fresh vs. POSB Everyday Card

While both DBS Live Fresh Card and POSB Everyday Card can ostensibly be used as "catch all" cards for daily essentials, their differing rebate and rewards structures make them best-suited to different types of spenders. As an essentially flat rebate card, DBS Live Fresh caters to modern consumers who want an easy-to-use card. POSB Everyday Card offers competitive rates on essentials, but has a few complications that make it less straightforward to use. We've expanded on the similarities and differences between these cards in the sections below.

Summary Comparison Table: DBS Live Fresh vs. POSB Everyday Card

| Category | Feature | DBS Live Fresh | POSB Everyday |

|---|---|---|---|

| Rates | Min. Spend Req. | S$600/mo | S$800/mo |

| Rebate Boosts |

|

| |

| Earnings Cap |

|

| |

| Perks | Petrol Savings | Up to 14% fuel savings at Esso | Up to 20.1% + 2% fuel savings at SPC |

| Compatibility | SimplyGo & Mobile Pay Compatible | SimplyGo & Mobile Pay Compatible | |

| Card Privileges | #FreshDropFriday Sweepstakes | POSB Exclusive Merchant Deals | |

| Fees | Annual Fee | S$194.40 | S$192.60 |

| Waiver Option | Waived for 1 year | Waived for 1 year |

Rewards Rates: DBS Live Fresh vs. POSB Everyday Card

Technically, DBS Live Fresh and POSB Everyday Card offer rewards on a month-to-month basis based on category boosts. However, the details of their rebate structures set them apart. To begin with, DBS Live Fresh Card rewards consumers with 5% cashback on online purchases and contactless transactions, all after S$600 minimum spend. These categories, however, lend themselves to almost any type of purchase–especially given how many vendors now accept tap and pay in Singapore. As a result, DBS Live Fresh functions almost like a flat rate card; modern consumers comfortable with using a digital wallet can easily earn cashback on nearly all of their spend.

POSB Everyday Card is a bit more complicated. Cardholders earn cashback boosts ranging from 3% to up to 10% in different categories (dining, groceries, personal care, recurring bills & more), but some of these rewards categories are merchant restricted or apply to local spend only. This means users must carefully track their purchases.

Finally, the current minimum spend requirement for POSB Everyday Card is S$800 with monthly cashback capped at S$30. As a result, given that DBS Live Fresh Card has a higher monthly cashback cap and is definitely easier to use, it may be a better option even though POSB Everyday Card may offer higher rates.

Comparison Table: Cashback Rewards

| Feature | DBS Live Fresh | POSB Everyday |

|---|---|---|

| Rebate Structure | Monthly System | Monthly System |

| Rate Structure | Category Boosts | Category Boosts |

| Base Rate | 0.30% | 0.30% |

| Min. Spend Req. | S$600 | S$800 |

| Boosts |

|

|

| Mo. Rewards Cap |

|

|

| Max Annual Earnings | S$720 | S$360 |

DBS Live Fresh Card isn't as straightforward as it might seem at first glance, either. While cardholders can technically earn up to S$60 per month, this cap is divided among the 3 categories. While cardholders can quickly max out the online and contactless categories with just S$400 spend in each, it would take S$6,667 general spend to max out the final category with the low 0.30% rate. Realistically, cardholders should expect to earn S$40 to S$45 per month at most with DBS Live Fresh Card. Those spending more than S$800 a month might want to look for a more flexible option.

Perks & Privileges: DBS Live Fresh vs. POSB Everyday Card

DBS Live Fresh and POSB Everyday Card each have perks that cater to a specific audience. The first focuses on young millennials. Cardholders have access to special promotions and sweepstakes as part of #FreshDropFriday. In previous contests, winners have received everything from gaming systems to customised sneakers. Cardholders also have access to special dining and lifestyle discounts, making it easy to save on fast food, live entertainment and more.

Comparison Table: Card Perks & Privileges

| Feature | DBS Live Fresh | POSB Everyday |

|---|---|---|

| Travel Insurance | N/A | N/A |

| Petrol Savings | Up to 14% fuel savings at Esso | Up to 20.1% + 2% fuel savings at SPC |

| Transit Perks | SimplyGo Compatible | SimplyGo Compatible |

| Mobile Pay | Google Pay, Apple Pay, Samsung Pay & more | Google Pay, Apple Pay, Samsung Pay & more |

| Card Privileges | #FreshDropFriday Sweepstakes, DBS Dining & Lifestyle Deals | POSB Exclusive Merchant Deals |

POSB Everyday Card's perks appeal more towards household spenders. Cardholders have access to POSB Exclusive Merchant Deals which typically center on utilities (sign-on bonuses with select companies), health (discounted check-ups, deals on supplements) and shopping (extra rebates with select fashion brands). While promotions change frequently, there are almost always a broad range of practical deals available to consumers.

Fees, Promos & Requirements: DBS Live Fresh vs. POSB Everyday

Finally, DBS Live Fresh and POSB Everyday Card are actually quite similar in terms of fees and requirements. Both cards have a S$192.60 annual fee, which is waived for the 1st year. While this waiver length is shorter than that offered by some competitors, cardholders whose accounts are in good standing may be able to call in and request an extension–though there are no guarantees.

Comparison Table: Requirements, Promos & Fees

| Feature | DBS Live Fresh | POSB Everyday |

|---|---|---|

| Minimum Age | 21 yo | 21 yo |

| Minimum Income |

|

|

| Annual Fee | S$194.40 | S$192.60 |

| Waiver Option | Waived for 1 year | Waived for 1 year |

| Sign-on Bonus | ||

| FX Fee | 3.25% | 3.25% |

Comparison to Similar Rebate Credit Cards

There are many competitive cashback cards on the market other than DBS Live Fresh and POSB Everyday. We've reviewed a few of the best comparable options below.

UOB One Card: Best Cashback for Stable Budgets

| |

Cardholders who reliably spend S$2k/month should definitely consider UOB One Card. Consumers earn based on a quarterly system; whose who maintain this spend level for a full 3 months earn 5% cashback on all of their purchases, up to S$100/month (S$300/quarter). This rebate rate and "flat" nature are similar to DBS Live Fresh Card. However, UOB One Card's earnings cap is much higher and is not divided, meaning moderate and higher spenders can earn far more than they could with DBS Live Fresh.

| |

|

|

Cardholders who reliably spend S$2k/month should definitely consider UOB One Card. Consumers earn based on a quarterly system; whose who maintain this spend level for a full 3 months earn 5% cashback on all of their purchases, up to S$100/month (S$300/quarter). This rebate rate and "flat" nature are similar to DBS Live Fresh Card. However, UOB One Card's earnings cap is much higher and is not divided, meaning moderate and higher spenders can earn far more than they could with DBS Live Fresh.

|

OCBC 365 Card: No-Fee Cashback on Essentials

| |

OCBC 365 Card is one of the best-known everyday cards currently on the market, and is also quite competitive. Cardholders who spend S$800/month earn up to 6% rebate on dining & online food delivery and 3% on groceries, land transport, recurring bills and online travel. Earnings are capped at S$80/month, which is notably higher than that offered by DBS Live Fresh Card. Also, OCBC 365 Card has no merchant restrictions, making it a bit easier to use than POSB Everyday Card. Finally, OCBC 365 Card's fee is even waived with just S$10k annual spend–neither DBS Live Fresh nor POSB Everyday Card have this feature. Ultimately, OCBC 365 Card is both competitive and easy-to-use, making it well worth considering as an everyday card.

| |

|

|

OCBC 365 Card is one of the best-known everyday cards currently on the market, and is also quite competitive. Cardholders who spend S$800/month earn up to 6% rebate on dining & online food delivery and 3% on groceries, land transport, recurring bills and online travel. Earnings are capped at S$80/month, which is notably higher than that offered by DBS Live Fresh Card. Also, OCBC 365 Card has no merchant restrictions, making it a bit easier to use than POSB Everyday Card. Finally, OCBC 365 Card's fee is even waived with just S$10k annual spend–neither DBS Live Fresh nor POSB Everyday Card have this feature. Ultimately, OCBC 365 Card is both competitive and easy-to-use, making it well worth considering as an everyday card.

|

Citi Cash Back Card: High Rates for Food & Petrol

| |

Citi Cash Back Card is great for consumers looking to earn cashback on their core expenses. Cardholders earn an impressive 8% cashback on dining, groceries and petrol after S$888 minimum spend. Rewards are capped at S$25/category (maxed out with S$312.5 spend), allowing consumers to potentially earn up to S$75/month.

| |

|

|

Citi Cash Back Card is great for consumers looking to earn cashback on their core expenses. Cardholders earn an impressive 8% cashback on dining, groceries and petrol after S$888 minimum spend. Rewards are capped at S$25/category (maxed out with S$312.5 spend), allowing consumers to potentially earn up to S$75/month.

|

Cashback Credit Card Comparison Tables

| Credit Card | Min. Spend | Rebates | Cap |

|---|---|---|---|

| Citi Cash Back | S$800 |

| S$80/mo |

| Citi SMRT | N/A |

| S$50/mo |

| DBS Live Fresh | S$600 |

| S$60/mo |

| OCBC 365 | S$800 |

| S$80/mo |

| OCBC Frank | S$600 |

| S$75/mo |

| POSB Everyday | S$800 |

| S$30 |

| UOB One | S$500-S$2k |

| S$100+/mo |

| UOB YOLO | S$600 |

| S$60/mo |

| Credit Card | Travel Ins | Petrol Savings | Card Perks |

|---|---|---|---|

| Citi Cash Back | Coverage up to S$1M | Up to 20.88% fuel savings at Esso & Shell | Citi World Privileges, Citi Gourmet Pleasures |

| Citi SMRT | N/A | Up to 20.88% fuel savings at Esso & Shell | Citi World Privileges, Citi Gourmet Pleasures |

| DBS Live Fresh | N/A | Up to 14% fuel savings at Esso | #FreshDropFriday Sweeps |

| OCBC 365 | Coverage up to S$500k | Up to 22.1% savings at Caltex, 20.2% at Esso, 26.8% at Sinopec and 5% cashback at all other petrol stations | Visa Concierge & Luxury Hotels |

| OCBC Frank | N/A | Up to 23% fuel savings at Sinopec, 16% at Caltex, 14% at Esso | Frank Hot Deals |

| POSB Everyday | N/A | Up to 20.1% + 2% fuel savings at SPC | POSB Merchant Deals |

| UOB One | Coverage up to S$500k | Up to 22.66% fuel savings at SPC, 21.15% at Shell | UOB SMART$, UOB Travel & Dining Advisors |

| UOB YOLO | Coverage up to S$500k | Up to 20% fuel savings at SPC, 14% at Shell | UOB SMART$, YOLO events |

| Credit Card | Annual Fee | Spend Waiver | Promotion |

|---|---|---|---|

| Citi Cash Back | S$194.40 | Waived for 1 year | |

| Citi SMRT Back | S$194.40 | Waived for 2 years | |

| DBS Live Fresh | S$194.40 | Waived for 1 year | |

| OCBC 365 | S$194.40 | Waived for 2 years with min spend of S$10,000/year | |

| OCBC Frank | S$80 | Waived 2 years, & subsequently with S$10,000 annual spend | |

| POSB Everyday | S$192.60 | Waived for 1 year | |

| UOB One | S$194.40 | Waived for 1 year | |

| UOB YOLO | S$192.60 | Waived for 1 year, no annual fees if min. 3 transactions per month for 12 consecutive months |

Learn More About Finding the Best Credit Card for You

- In-Depth Comparison: POSB Everyday Card vs. OCBC 365 Card

- In-Depth Comparison: UOB One Card vs. OCBC 365 Card

- In-Depth Comparison: UOB One Card vs. UOB YOLO Card

- In-Depth Comparison: DBS Live Fresh Card vs. UOB YOLO Card

- In-Depth Comparison: OCBC Frank Card vs. OCBC 365 Card

- In-Depth Comparison: Citi Cash Back Card vs. Citi Rewards Card

- In-Depth Comparison of Unlimited Cashback Credit Cards

- How to Use a Credit Card

- How to Find the Best Rewards Credit Card

- Comparing Fee Credit Cards to No Annual Fee Cards in Singapore

- Understanding Credit Cards' Minimum Spend Requirements

- Understanding Rewards Caps on Monthly Earnings