Best Citibank Credit Cards 2024

Our research team has reviewed and compared Citibank's best credit cards that have distinct and disparate strengths to appeal to different individuals. No card is perfect, but we think these cards could be highly valuable to most Singaporeans who want to earn rewards and save on daily expenditures.

- Citi Cash Back: Up to 8% rebate on groceries & petrol, 6% on dining

- Citi Cash Back Plus: Unlimited 1.6% cashback on all spend

- Citi SMRT: 5% everyday rebates w/S$500 min spend

- Citi PremierMiles: 45,000 Welcome Citi Miles with S$9,000 spend in 3 mo

- Citi Prestige: Unlimited lounge access, bonus hotel nights & more

- Citi Rewards: Up to 4 miles per S$1 for fashion & online spend

- Citi Lazada: Up to 4 miles per S$1 spend on Lazada

- Citi Ultima: 150k annual bonus miles, Companion airfare program, buy-one-get-one hotel nights and up to three Priority Pass memberships

- Citi Clear: 0.4 miles per S$1 for students, foodie privileges

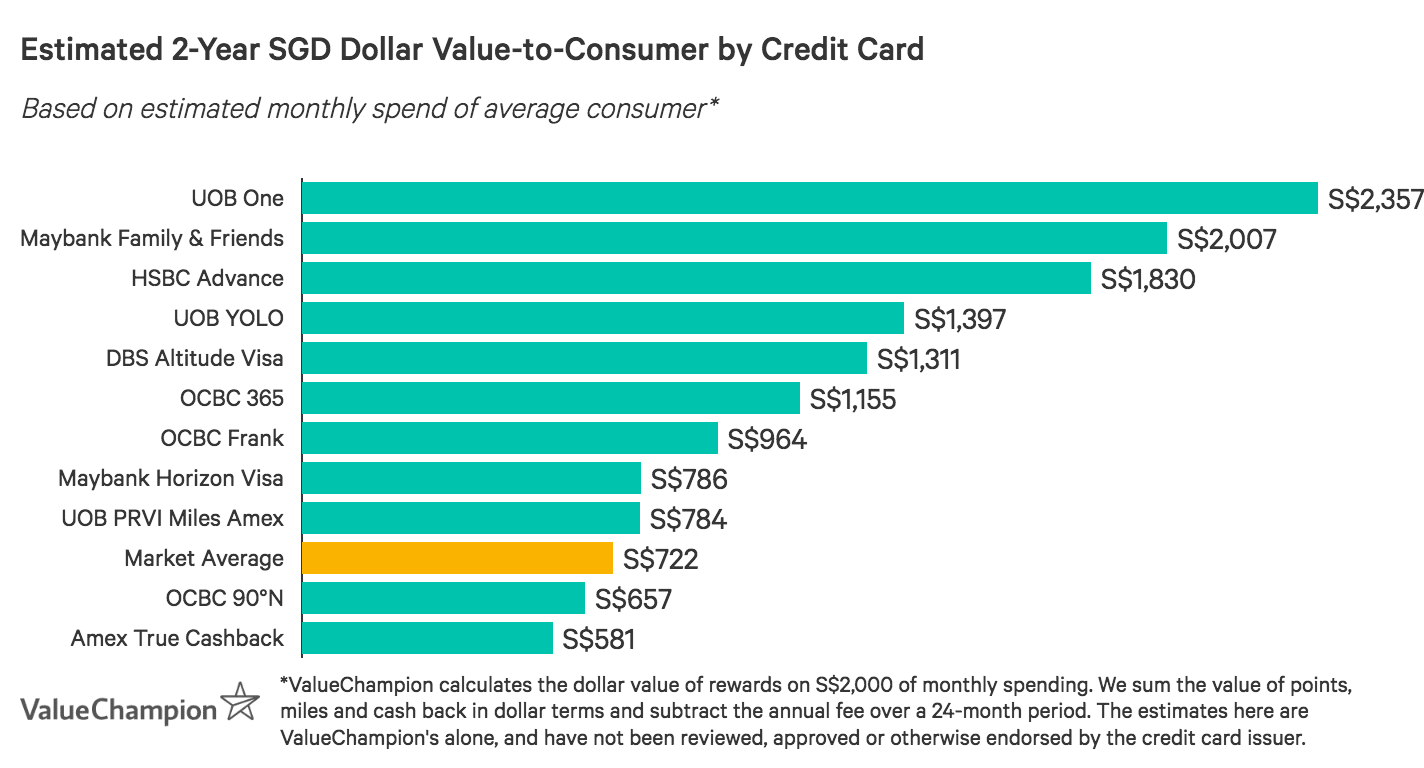

Compare Best Citibank Credit Cards by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best Citibank credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

- Citi Cash Back: Up to 8% rebate on groceries & petrol, 6% on dining

- Citi Cash Back+: Unlimited 1.6% cashback on all spend

- Citi SMRT: 5% everyday rebates w/S$500 min spend

- Citi PremierMiles: 45,000 Welcome Citi Miles with S$9,000 spend in 3 mo

- Citi Prestige: Unlimited lounge access, bonus hotel nights & more

- Citi Rewards: Up to 4 miles per S$1 for fashion & online spend

- Citi Lazada: Up to 4 miles per S$1 spend on Lazada

- Citi Ultima: 150k annual bonus miles, Companion airfare program, buy-one-get-one hotel nights and up to three Priority Pass memberships

- Citi Clear: 0.4 miles per S$1 for students, foodie privileges

Compare Best Citibank Credit Cards by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best Citibank credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Citi Cash Back Credit Card: Best Cashback on Food & Petrol

| |

Citi Cash Back Card is an exceptional option if you spend a great deal of your budget on food and transport. In fact, cardholders can earn up to 8% cashback on groceries and petrol, and 6% on dining worldwide–one of the higher rates on the market. Even better, you can earn up to S$80/month, or S$960/year, just for spending in these key categories.

| |

|

|

Citi Cash Back Card is an exceptional option if you spend a great deal of your budget on food and transport. In fact, cardholders can earn up to 8% cashback on groceries and petrol, and 6% on dining worldwide–one of the higher rates on the market. Even better, you can earn up to S$80/month, or S$960/year, just for spending in these key categories.

|

Citi Cash Back+ (Plus) Credit Card: Highest Unlimited Flat Rebate Rate

| |

For high spenders with a budget of about S$7,000/month, Citi Cash Back+ Card is one of the cards that can maximise the rebates they can earn. Cardholders receive an unlimited rebate of 1.6% on all expenditures, with no minimum spend requirement or cap on rebate. Due to this no cap feature, Citi Cash Back Plus Card is ideal for consumers who are constrained by cards that may offer higher rate of rewards but with low limits. Also, while this card doesn't provide many extra perks or privileges, its rewards rate is also higher than the 1.5% offered by most comparable "unlimited cashback" cards, and the cashback earned does not expire.

| |

|

|

For high spenders with a budget of about S$7,000/month, Citi Cash Back+ Card is one of the cards that can maximise rebates they can earn. Cardholders receive an unlimited rebate of 1.6% on all expenditures, with no minimum spend requirement or cap on rebate. Due to this no cap feature, Citi Cash Back Plus Card is ideal for consumers who are constrained by cards that may offer higher rate of rewards but with low limits. Also, while this card doesn't provide many extra perks or privileges, its rewards rate is also higher than the 1.5% offered by most comparable "unlimited cashback" cards, and the cashback earned does not expire.

|

Citi SMRT Credit Card: Rebates + EZ-Link for Low Spenders

|

|

If you have a low or variable budget, but want consistent access to top rebate rates, consider Citi SMRT Card. This card has one of the lowest minimum spend requirements – S$500, and it offers respectable rates across a variety of categories– 5% on online purchases, groceries, taxis and public transport rides (EZ-Link Auto Top-Up and SimplyGo transactions).

| |

|

|

|---|

|

|

If you have a low or variable budget, but want consistent access to top rebate rates, consider Citi SMRT Card. This card has one of the lowest minimum spend requirements – S$500, and it offers respectable rates across a variety of categories– 5% on online purchases, groceries, taxis and public transport rides (EZ-Link Auto Top-Up and SimplyGo transactions).

|

Citi PremierMiles Credit Card: Affordable Miles & Perks

| |

Citi PremierMiles Card is the best travel card if you’re looking for affordable miles and travel perks. Cardholders earn 4 miles per S$1 on food delivery and home entertainment, 1.2 miles per S$1 locally and 2 miles overseas, which aligns with market standards. However, Citi PM Card stands out because new cardmembers receive 45,000 Citi Miles as a welcome gift for spending S$9,000 within 3 months of card approval. These bonuses easily offset the already reasonable S$192.60 fee. Most travel cards have fees of S$250+, and the closest competitor doesn’t offer bonus miles.

| |

|

|

Citi PremierMiles Card is the best travel card if you’re looking for affordable miles and travel perks. Cardholders earn 4 miles per S$1 on food delivery and home entertainment, 1.2 miles per S$1 locally and 2 miles overseas, which aligns with market standards. However, Citi PM Card stands out because new cardmembers receive 45,000 Citi Miles as a welcome gift for spending S$9,000 within 3 months of card approval. These bonuses easily offset the already reasonable S$192.60 fee. Most travel cards have fees of S$250+, and the closest competitor doesn’t offer bonus miles.

|

Citi Prestige MasterCard Credit Card: Best for Luxury Travel Perks

|

|

Citi Prestige MasterCard is one of the absolute best travel cards on the market if you prioritise luxury perks & privileges. In terms of rewards, cardholders earn an impressive 4 miles per S$1 spend on food delivery and entertainment, 1.3 miles per S$1 locally and 2 miles overseas. In addition, new cardmembers receive 25,000 Miles as a welcome gift for paying the S$535 annual fee.

| |

|

|

|---|

|

|

Citi Prestige MasterCard is one of the absolute best travel cards on the market if you prioritise luxury perks & privileges. In terms of rewards, cardholders earn an impressive 4 miles per S$1 spend on food delivery and entertainment, 1.3 miles per S$1 locally and 2 miles overseas. In addition, new cardmembers receive 25,000 Miles as a welcome gift for paying the S$535 annual fee.

|

Citi Rewards Credit Card: Best Miles for Online & Fashion Spend

| |

Citi Rewards Card is one of the most flexible shopping cards on the market if you primarily spend online & on fashion retail. Cardholders earn 10 points (4 miles) per S$1 spend on online purchases, shopping, rides (Grab, Gojek and more), online food delivery and groceries. As a result, it's rather easy for modern shoppers to earn rewards across a broad variety of spending categories. While the base rate of 0.4 miles per S$1 spend is uncapped, the bonus rate of 4 miles per S$1 is capped at 4,000 miles/month (or 10,000 Points). This amount can be reached with S$1,000 spend, making Citi Rewards Card a great option for those with a similarly-sized monthly shopping budget.

| |

|

|

Citi Rewards Card is one of the most flexible shopping cards on the market if you primarily spend online & on fashion retail. Cardholders earn 10 points (4 miles) per S$1 spend on online purchases, shopping, rides (Grab, Gojek and more), online food delivery and groceries. As a result, it's rather easy for modern shoppers to earn rewards across a broad variety of spending categories. While the base rate of 0.4 miles per S$1 spend is uncapped, the bonus rate of 4 miles per S$1 is capped at 3,600 miles/month (or 9,000 Points). This amount can be reached with S$1,000 spend, making Citi Rewards Card a great option for those with a similarly-sized monthly shopping budget.

|

Citi Lazada Credit Card: Miles for Lazada & Social Spend

|

|

Citi Lazada Card is the best option on the market for frequent Lazada shoppers who also have a small-to-medium budget for social spend. Cardholders earn 4 miles (10pts) per S$1 spend with Lazada, 2 miles (5pts) on dining, travel, entertainment and commute as well as shipping rebates on Lazada on purchases of S$50+ (up to 4x/month). While this may not seem like a lot, it adds up to a potential 4% rebate on associated purchase. Consumers also have access to exclusive Lazada offers and discounts.

| |

|

|

|---|

|

|

Citi Lazada Card is the best option on the market for frequent Lazada shoppers who also have a small-to-medium budget for social spend. Cardholders earn 4 miles (10pts) per S$1 spend with Lazada, 2 miles (5pts) on dining, travel, entertainment and commute as well as shipping rebates on Lazada on purchases of S$50+ (up to 4x/month). While this may not seem like a lot, it adds up to a potential 4% rebate on associated purchase. Consumers also have access to exclusive Lazada offers and discounts.

|

Citi Ultima Credit Card: Metal Card Luxury, By Invite Only

|

|

As one of the most luxurious invite-only metal cards on the market, Citi Ultima credit card is ideal for high-spending travellers who enjoy golfing on their getaways. Cardholders–who must earn S$500k/year just to qualify–earn a fairly standard 1.6 miles per S$1 locally and 2 miles overseas, but receive an incredible 150,000 bonus miles (worth S$1.5k) every year with card renewal. This at least partially offsets the hefty S$4,160 annual fee.

| |

|

|

|---|

|

|

As one of the most luxurious invite-only metal cards on the market, Citi Ultima credit card is ideal for high-spending travellers who enjoy golfing on their getaways. Cardholders–who must earn S$500k/year just to qualify–earn a fairly standard 1.6 miles per S$1 locally and 2 miles overseas, but receive an incredible 150,000 bonus miles (worth S$1.5k) every year with card renewal. This at least partially offsets the hefty S$4,160 annual fee.

|

Citi Clear Credit Card: Best Miles Card for Students

|

|

Citi Clear Card is one of the only options on the market that allows students to earn points/miles instead of cashback. Cardholders earn 1 point (0.4 miles) per S$1 spend, which is roughly equal to a 0.4% rebate. This is a higher rate than offered by several competitor cards. In addition, cardholders have access to dining programmes like Citi Gourmet Pleasures, which offers discounts on everything from online food delivery to sit-down meals at high-end restaurants. There are no minimum spend requirements and the S$29.96 fee is waived 1 year. For students who prefer miles to cashback, Citi Clear Card is worth considering.

| |

|

|

|---|

|

|

Citi Clear Card is one of the only options on the market that allows students to earn points/miles instead of cashback. Cardholders earn 1 point (0.4 miles) per S$1 spend, which is roughly equal to a 0.4% rebate. This is a higher rate than offered by several competitor cards. In addition, cardholders have access to dining programmes like Citi Gourmet Pleasures, which offers discounts on everything from online food delivery to sit-down meals at high-end restaurants. There are no minimum spend requirements and the S$29.96 fee is waived 1 year. For students who prefer miles to cashback, Citi Clear Card is worth considering.

|

Other Citibank Credit Cards

Citi M1 Credit Card: Best for M1 Loyalists

|

|

Citi M1 Credit Card is a great option for M1 customers looking to earn cashback and discounts on their M1 bills and purchases. Customers earn up to 10% rebate on their recurring M1 bills, 1% cashback on purchases at M1 shops and 0.3% cashback on all other retail transactions. The boosted rates only apply to monthly spend above S$600. In addition, customers get complimentary replacement of lost and damaged SIM cards, waiver of activation fees for data passport registration and buy now, pay later plan with no processing fees.

| |

|

|

|---|

|

|

Citi M1 Credit Card is a great option for M1 customers looking to earn cashback and discounts on their M1 bills and purchases. Customers earn up to 10% rebate on their recurring M1 bills, 1% cashback on purchases at M1 shops and 0.3% cashback on all other retail transactions. The boosted rates only apply to monthly spend above S$600. In addition, customers get complimentary replacement of lost and damaged SIM cards, waiver of activation fees for data passport registration and buy now, pay later plan with no processing fees.

|

Learn More About Maximising Your Rewards with Citibank Credit Cards

Choosing the right credit card for you can be challenging and often confusing. Rewards rates, while often the clearest, are rarely the best indicator of whether or not a card matches your lifestyle. Consider these factors when you weigh your options to make sure you are taking a more holistic, representative view:

Annual Fee: Many credit cards charge an annual fee, typically ranging from S$180.0 up to S$600+, depending on the nature of the card. Fortunately, there are several cards that offer spend-based fee waivers (for example, if you spend S$10k/year, you won't need to pay the fee) and a few that don't charge an annual fee at all. When selecting a credit card, take a look at its associated annual fee and any potential waivers. For a card to truly prove beneficial, you'll need to earn more in rewards value than you're cost by the annual fee (it's important to mention that some perks, like lounge access and free limo transfers, provide value that's harder to quantify). If you're interested in a card that has a fee waiver, make sure you can confidently meet the minimum spend required to unlock that waiver. Finally, cards without an annual fee may not necessarily be the best fit, so it's better to consider all options before defaulting to what's "free."

Minimum Spend Requirement: Some credit cards, especially cashback cards, may require you to spend a set amount per month before you're eligible to earn above a base rewards rate (typically 0.4% cashback or 0.4 miles per S$1 spend). As a result, you should only select a card whose minimum requirement is quite reasonable in terms of your budget. If you can't reliably meet this minimum every month, it won't matter how high the card's advertised rewards rates are. Additionally, you'll lose out even if you miss the cut-off by S$1 or if your final qualifying purchases miss the deadline for a given month. If you're uncertain, it's better to opt for a credit card with a more achievable minimum spend requirement.

Monthly Earnings Caps: Credit card companies often advertise high rewards rates, like "10% cashback on dining," "4 miles per S$1 online" and more. While these rates are certainly attractive and may lead the market, they may not apply to every purchase you make, even in the eligible categories. In fact, higher rates usually come with earnings caps. For example, you may earn 10% cashback on dining–up to S$20 in rewards, and thereafter earn a base rate of 0.4% on dining spend. Other credit cards might offer lower rebate rates, but allow for higher caps. This means that if you're a higher spender, you may ultimately be able to earn more from the second type of card. Always check to see if a credit card caps earnings, especially if it has high rewards rates in select categories.

Rewards-Eligible Categories: Finally, you may come across credit cards with sky-high rewards rates–at first, this may seem incredibly appealing. However, check to see which rewards categories these rates apply to. Earning an 8% rebate on pet supplies isn't so great if you don't own a pet, and a card with high rates for overseas spend may not be a match if you only spend locally. If you want a credit card that's especially easy to use and doesn't require you to track categories or even specific merchants, consider applying for a flat credit card that offers the same rewards rate for all spend.

Citi SMRT Credit Card v. OCBC 365 Card

| |

| OCBC 365 Card is an excellent option for average spenders looking for rebates on daily essentials. Cardholders earn up to 6% cashback on dining and 3% on groceries, transport, recurring bills and online travel. Even EZ-Link & Transitlink transactions are rewards eligible, though only at a 0.3% rate. There is a S$800 minimum spend requirement and cardholders can earn up to S$80/month. Finally, the S$192.60 fee is waived with S$10,000 annual spend.

| |

Citi PremierMiles Credit Card v. DBS Altitude Card

| |

| DBS Altitude Visa Card is fairly similar to Citi PM Card. Both offer 1.2 miles per S$1 spend locally and 2 miles overseas, and both also have a S$192.6 annual fee. Both cards also offer 2 free lounge visits/year. These cards are differentiated in a few ways, however. DBS Altitude Cardholders can earn a fee-waiver with S$25,000 annual spend, and enjoy a few extra travel perks, like golfing privileges. Citi PM Card, on the other hand, offers 10,000 bonus renewal miles and has a stronger free travel insurance plan. Overall, you may prefer Citi PM Card if you want to earn extra bonus miles, or DBS Altitude Card if you want a fee-waiver. | |

Citi Rewards Credit Card v. OCBC Titanium Rewards Card

| |

| Like Citi Rewards Card, OCBC Titanium Rewards Card offers 4 miles per S$1 spend on fashion retail online, offline, locally and overseas. OCBC Titanium Card, however, also rewards online and offline spend with merchants like Amazon, Shopee, IKEA & more, allowing you to earn for a broad range of purchases. In addition, cardholders can earn a fee-waiver with S$10,000 annual spend. If you have broader retail shopping habits and want a no-fee card, you might prefer OCBC Titanium Card. | |

Citi Lazada Credit Card v. HSBC Revolution Card

| |

| HSBC Revolution Card offers a great way for consumers to earn miles both on local social spend as well as on online purchases. Cardholders earn 2 miles per S$1 on local dining & entertainment as well as on all online spend. This even includes online travel bookings and even bill-pay, which are often excluded by other cards. Even better, rewards are uncapped and consumers can earn a fee waiver with just S$12.5k annual spend. Many shopping cards, including Citi Lazada, either cap rewards or lack a fee-waiver (or in some cases, both). As a result, consumers who want a no-fee miles card with flexible rewards for online spend may prefer HSBC Revolution Card. | |

Citi Cash Back Credit Card v. CIMB Platinum MasterCard

|

|

| CIMB Platinum MasterCard offers the highest rebate rate for food on the market–10% cashback on both dining worldwide. This rate also applies to transport, petrol, medical spend & more, making it an especially versatile card. There is a S$800 minimum spend requirement, which is slightly lower than Citi Cash Back Card's, and the earnings cap is a lofty S$100/month. Cardholders also never need to pay an annual fee.

| |

Citi Prestige Credit Card v. Standard Chartered Visa Infinite Card

| |

| Standard Chartered Visa Infinite X Credit Card has the highest welcome bonus on the market, with an astounding up to 300k KrisFlyer miles for those who place S$1.5mn fresh funds in a Priority Banking account and maintain this amount for 3 months, which is worth S$30k if redeemed for business or first class tickets (100k miles for $300k). This card is clearly designed for high income earners due to this benefit, which is the biggest highlight of the product.

| |

| Citi SMRT Credit Card v. OCBC 365 Card | |

|---|---|

| |

| OCBC 365 Card is an excellent option for average spenders looking for rebates on daily essentials. Cardholders earn up to 6% cashback on dining and 3% on groceries, transport, recurring bills and online travel. Even EZ-Link & Transitlink transactions are rewards eligible, though only at a 0.3% rate. There is a S$800 minimum spend requirement and cardholders can earn up to S$80/month. Finally, the S$192.6 fee is waived with S$10,000 annual spend.

| |

| Citi PremierMiles Credit Card v. DBS Altitude Card | |

|---|---|

| |

| DBS Altitude Visa Card is fairly similar to Citi PM Card. Both offer 1.2 miles per S$1 spend locally and 2 miles overseas, and both also have a S$192.6 annual fee. Both cards also offer 2 free lounge visits/year. These cards are differentiated in a few ways, however. DBS Altitude Cardholders can earn a fee-waiver with S$25,000 annual spend, and enjoy a few extra travel perks, like golfing privileges. Citi PM Card, on the other hand, offers 10,000 bonus renewal miles and has a stronger free travel insurance plan. Overall, you may prefer Citi PM Card if you want to earn extra bonus miles, or DBS Altitude Card if you want a fee-waiver. | |

| Citi Rewards Credit Card v. OCBC Titanium Rewards Card |

|---|

|

| Like Citi Rewards Card, OCBC Titanium Rewards Card offers 4 miles per S$1 spend on fashion retail online, offline, locally and overseas. OCBC Titanium Card, however, also rewards online and offline spend with merchants like Amazon, Shopee, IKEA & more, allowing you to earn for a broad range of purchases. In addition, cardholders can earn a fee-waiver with S$10,000 annual spend. If you have broader retail shopping habits and want a no-fee card, you might prefer OCBC Titanium Card. |

| Citi Lazada Credit Card v. HSBC Revolution Card |

|---|

|

| HSBC Revolution Card offers a great way for consumers to earn miles both on local social spend as well as on online purchases. Cardholders earn 2 miles per S$1 on local dining & entertainment as well as on all online spend. This even includes online travel bookings and even bill-pay, which are often excluded by other cards. Even better, rewards are uncapped and consumers can earn a fee waiver with just S$12.5k annual spend. Many shopping cards, including Citi Lazada, either cap rewards or lack a fee-waiver (or in some cases, both). As a result, consumers who want a no-fee miles card with flexible rewards for online spend may prefer HSBC Revolution Card. |

| Citi Cash Back Credit Card v. CIMB Platinum MasterCard |

|---|

|

|

|

| CIMB Platinum MasterCard offers the highest rebate rate for food on the market–10% cashback on both dining worldwide. This rate also applies to transport, petrol, medical spend & more, making it an especially versatile card. There is a S$800 minimum spend requirement, which is slightly lower than Citi Cash Back Card's, and the earnings cap is a lofty S$100/month. Cardholders also never need to pay an annual fee.

|

| Citi Prestige Credit Card v. Standard Chartered Visa Infinite Card |

|---|

|

| Standard Chartered Visa Infinite X Credit Card has the highest welcome bonus on the market, with an astounding up to 300k KrisFlyer miles for those who place S$1.5mn fresh funds in a Priority Banking account and maintain this amount for 3 months, which is worth S$30k if redeemed for business or first class tickets (100k miles for $300k). This card is clearly designed for high income earners due to this benefit, which is the biggest highlight of the product.

|

Read More:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.