HSBC Visa Platinum Credit Card: No Fee Cashback Card for Food & Petrol

HSBC Visa Platinum Credit Card: No Fee Cashback Card for Food & Petrol

ValueChampion Rating ![]()

Pros

- Great local dining & groceries rewards

- Suitable for moderate budgets (S$1,600+/month)

- Cashback & miles rewards

Cons

- Limited miles & travel perks

- Not suitable for frequent online shoppers

Consumers with high consistent spend on food and petrol can maximise rewards–both in cashback and miles–with HSBC Visa Platinum Credit Card. Consumers earn 5% cashback on local dining and groceries (including food deliveries and online groceries), up to 17% instant discount plus 5% cash rebate on fuel spending at Caltex and Shell stations, and 0.4 miles per S$1 general spend (equivalent in value to 0.4% cashback).

However, the card's rebate system requires a consistent S$600+ monthly spend to access this rate, and earnings are capped at S$250/quarter. Still, consumers with a S$2,000 budget could reasonably earn S$85–S$90 monthly in total value, making HSBC Visa Platinum Credit Card one of the best cards on the market for average spenders.

HSBC Visa Platinum Credit Card Features and Benefits

|

|---|

Key Features:

|

What Makes HSBC Visa Platinum Credit Card Stand Out

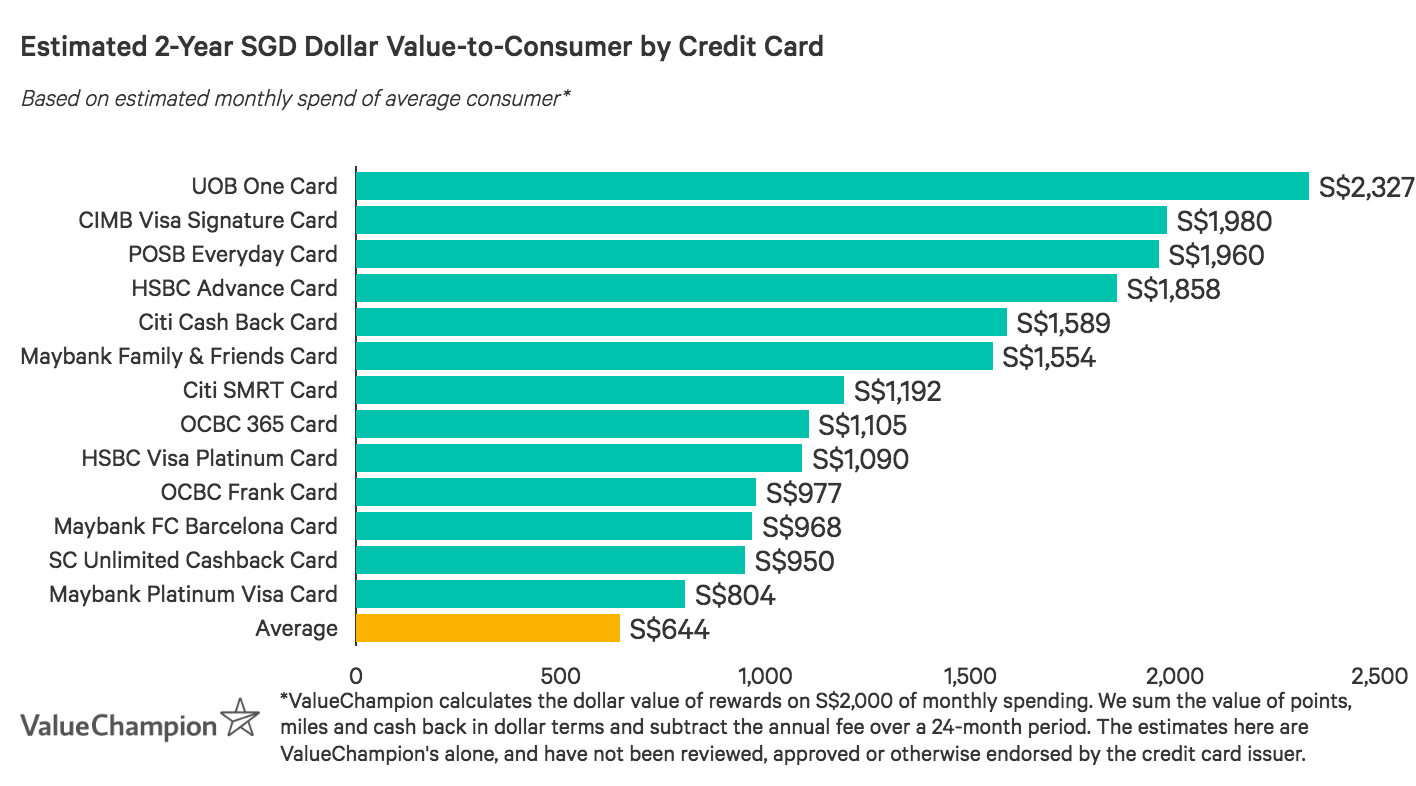

HSBC Visa Platinum Credit Card may be the best rewards card on the market for average consumers who consistently spend on local food and petrol, and is unique in offering both cashback and miles. Cardholders can earn 5% cashback on local dining and groceries (includes food deliveries and online groceries) and up to 22% fuel savings at Caltex and Shell (up to 17% instant discount + 5% card savings). In addition, consumers earn an unlimited 0.4 miles per S$1 general spend, which has a value equivalent to about 0.4% cashback–a return higher than the base rate offered by many cashback cards (Citi Cash Back Credit Card has a base rate of 0.25% and the CIMB Platinum MasterCard offers 0.2%, for example).

While HSBC Visa Platinum Credit Card offers great earning potential, its rewards are structured according to a quarterly rebate system, which requires budget consistency. Consumers must spend at least S$600/month for every month within a quarter to access the 5% cashback rates. If spend is lower within any month, earnings default to 0.4% cashback for the entire quarter. Low or inconsistent spenders may not be the best fit for this card.

The rebate system also limits earnings to S$250/quarter, or about S$83/month. Cardholders can max out cashback by spending S$1,667/month on local food and petrol, which is reasonable for the average consumer. Miles rewards for general spend are unlimited, so individuals with a budget closer to S$2,000 may very well earn up to S$85–S$90/month in total rewards value.

| Category | Rewards Rate | Monthly Spend | Monthly Cashback | Quarterly Cashback |

|---|---|---|---|---|

| Local dining, groceries & petrol | 5% | S$1,667 | S$83 | S$250 (cap) |

| General spend | 0.4%* | S$500 | S$2 | S$6 |

| Total | -- | S$2,167 | S$85 | S$255 |

HSBC Visa Platinum Card has a S$192.60 annual fee, but this is waived 2 years and subsequently with every S$12,500 spend, making the card even more affordable. Because consumers can avoid this fee and earn S$1,000+ in rewards value per year, HSBC Visa Platinum Credit Card is an excellent option for average spenders with primarily local budgets.

How Does HSBC Visa Platinum Credit Card's Rewards Program Work?

Use our quick and easy-to-read guide below to learn how you you can redeem HSBC Visa Platinum Card rewards.

| Program Description by Rewards Type |

|---|

Cashback

|

Points/Miles

|

HSBC Visa Platinum Credit Card Rewards Exclusions

Some credit card expenditures are ineligible for cash back or rebate. We identify these exclusions in the table below.

| Exclusion Category | Description |

|---|---|

| Bank Fees | Balance transfers, financial charges, late charges, fees, foreign exchange transactions (including but not limited to Forex, etc), cash advances |

| Transfers & Bill Payments | Transactions relating to the trading of securities or crypto-currencies of any kind (including but not limited to any top up of any cash amount required by a financial institution), transactions relating to payments and money transfers made through the Internet (including but not limited to Paypal, SKR), transactions made with any professional services provider (including but not limited to GOOGLE Ads, Facebook Ads, Amazon Web Services, MEDIA TRAFFIC AGENCY INC), any pre-paid card top-ups (including but not limited to EZ-Link, Transitlink or NETS Flashpay), any AXS transaction and tax payments |

| Institutional Payments | Donations and payments to charitable and social organisations (Merchant Category Code (MCC)= 8398), any payment in connection with any government institutions and/or services (including but not limited to court costs, fines, bail and bond payment), hotel dining merchants* |

| Betting or Gambling | Quasi-cash transactions (for example but not limited to transactions relating to money orders, traveler's checks, gaming related transactions, lottery tickets) |

| Insurance | Payments to insurance companies (including but not limited to sales, underwriting, premiums and insurance services) |

Examples of excluded transaction include:

- Foreign exchange transactions (including but not limited to Forex.com);

- Donations and payments to charitable, social organisations and religious organisations;

- Payments on money payments/transfers (including but not limited to Paypal, SKR skrill.com, CardUp, SmoovPay, iPayMy);

- Payments to any professional services provider (including but not limited to GOOGLE Ads, Facebook Ads, Amazon Web Services, MEDIA TRAFFIC AGENCY INC);

- Top-ups, money transfers or purchase of credits of prepaid cards, stored-value cards or e-wallets (including but not limited to EZ-Link, Transitlink, NETS Flashpay and Youtrip);

- Payments in connection with any government institutions and/or services (including but not limited to court costs, fines, bail and bond payment);

- Any AXS and ATM transactions;

- Tax payments (except HSBC Tax Payment Facility);

- Payments for cleaning, maintenance and janitorial services (including property management fees);

- Payments to educational institutions;

- Payments on utilities;

- The monthly instalment amounts under the HSBC Spend Instalment;

- Balance transfers, fund transfers, cash advances, finance charges, late charges, HSBC’s Cash Instalment Plan, any fees charged by HSBC;

- Any unposted, cancelled, disputed and refunded transactions

How does HSBC Visa Platinum Credit Card Compare Against Other Cards?

Read our comparisons of HSBC Visa Platinum Credit Card with other cards and learn what makes each card unique in their own way. We compare and contrast each card to highlight its uniqueness to help you identify the card that you need.

HSBC Visa Platinum Credit Card v. Maybank Family & Friends MasterCard

- Pros

- Good for budgets of S$800/month

- Awards 8% cashback on 5 categories of your choice

- 3 year annual fee waiver

- Great to use in Singapore, Malaysia, Indonesia and the Philippines

- Cons

- Merchant restrictions

- Lacks miles & travel perks

People with lower budgets who primarily spend in Singapore and Malaysia can definitely make more of their purchases with Maybank Family & Friends MasterCard. With just S$500 minimum spend–lower than HSBC Visa Platinum's–cardholders can earn 5% rebate on fast food & food delivery, groceries, transport, petrol, data communications/online TV streaming & more (S$800 spend boosts the rewards rate to 8%). Rewards categories aren't merchant restricted, and the S$180 fee is waived 3 years, and then with S$12,000 annual spend. Like the HSBC Visa Platinum Credit Card, Maybank F&F Card limits cashback to local and regional spend. However, Maybank's slightly lower minimum spend requirement may be more attractive to people with a smaller budget.

HSBC Visa Platinum Credit Card v. Citi Cash Back Credit Card

- Pros

- Great dining and groceries rewards

- High petrol discounts

- Cons

- Lacks shopping and entertainment rewards

- Not suitable for lower budgets

Consumers who mostly spend on food and transport can benefit from Citi Cash Back Credit Card's 8% cashback on dining, groceries, and petrol worldwide, capped at S$75/month. While its rate and cap are higher than HSBC Visa Platinum Credit Card's, the minimum monthly spend is a lofty S$888, and the S$192.6 fee is waived only 1 year. As a result, HSBC Visa Platinum Credit Card may be a better match for consumers with lower monthly spends looking to avoid an annual fee.

HSBC Visa Platinum Credit Card v. CIMB Platinum MasterCard

- Pros

- Awards cashback for global transport

- Cashback for medical expenses and travel spend in foreign currency

- No annual fee credit card

- Cons

- Doesn't award cashback on everyday essentials

- No cashback on online spend

For those who spend a great deal on dining and transport, but also want a credit card with a slightly more well-rounded rewards structure, CIMB Platinum MasterCard is certainly worth considering. Cardholders earn 10% cash back in both of these categories, as well as on health and medical expenses, travel spend in foreign currency, and purchases with select electronics and furnishings vendors. While rewards are capped at S$20/category, consumers can ultimately earn a cumulative S$100/month–one of the highest potential earnings on the market. Even better, there's no annual fee. For consumers who can meet the S$800 minimum spend, and who want a well-balanced dining and petrol card, CIMB Platinum MasterCard is a great fit.

HSBC Visa Platinum Credit Card v. UOB One Card

- Pros

- Good fit for budgets of at least S$2,000 per month

- Easy cashback on daily spend

- Gives rebates for paying bills

- Cons

- Doesn't fit inconsistent budgets

- Annual fee

Like the HSBC Visa Platinum Credit Card, the UOB One Card follows a quarterly rebate system and maximises rewards for consistent spenders. While UOB One Card's 5% flat cashback rate conveniently applies to all purchases, consumers must sustain a S$2,000/month budget or the rate drops to 3.33%–HSBC Visa Platinum Credit Cardholders must only maintain S$600/month spend. Consumers can earn S$50 more per quarter with UOB One Card (S$300 v. S$250 quarterly cap), but those who cannot consistently spend S$2,000/month might consider HSBC Visa Platinum Credit Card instead.

HSBC Visa Platinum Credit Card v. OCBC 365 Card

- Pros

- 6% rebate on dining, 3% on groceries, transport, utilities, online travel

- Fee waiver with S$10,000 annual spend

- Up to 22.1% fuel savings at Caltex, 20.2% at Esso

- Cons

- 0.3% rebate on general spend

- High S$800 minimum spend requirement

OCBC 365 Card rewards average consumers for daily spend on essentials like dining (6%) and petrol (5%). While these rates compare to HSBC Visa Platinum Card's, OCBC 365 Card only offers 3% cashback on groceries (v. 5%). Nonetheless, OCBC 365 Card is more well-rounded and rewards transport, online travel, and utilities with 3% cashback. These categories earn the equivalent of just 0.4% cashback with HSBC Visa Platinum Credit Card. Otherwise, the cards are quite similar–OCBC 365 Card's earnings are capped at S$80/month and its S$192.6 fee is waived with S$10,000 annual spend. Ultimately, the OCBC 365 Card may be a better fit for average spenders with highly diversified spend looking for a true 'everyday' card.

To view the best cashback credit cards available in Singapore, check over here for more!

Read Also:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.