Credit Card Minimum Payment: What You Need To Know

Get the Best Credit Cards in Singapore

The minimum payment on a credit card is the smallest amount of money you’re required to pay on your bill. Failure to pay at least this amount of your bill can result in various penalties like late payment fees, interest charges and lower credit scores. Each bank has a different method for calculating a credit card’s monthly minimum payment, though most banks require a minimum of S$50.

Table of Contents

- Minimum Credit Card Payment by Issuer

- What Happens If You Pay Just The Minimum Amount Due On Your Credit Card

- Minimum Payment and Your Credit Score

- Consequences of Paying Less Than The Minimum On Your Credit Card Bill

- FAQs

Minimum Credit Card Payment by Issuer

Though banks calculate their minimum credit card payment in a variety of ways, most require at least S$50 or 3% of your total principal outstanding balance, whichever is higher, plus any overdue amount. In general, this minimum requirement is meant to be large enough so that the cardholder pays at least some portion of their principal balance.

In theory, such a rule prevents banks from setting minimum payments that would result in negative amortization, which could mislead a card user to pay less than his interest and end up with an unbearable amount of credit card debt. Failure to make the minimum monthly payment will result in a late payment charge of S$100.

| Issuer | Minimum Payment Formula | Your Minimum Payment Will Be At Least |

|---|---|---|

| ANZ | S$50 or 3% of the total principal outstanding balance, whichever is higher, and any overdue amount | S$50 |

| American Express | 3% of the outstanding balance plus the total sum of any overdue minimum payment and late payment charges, and any amount exceeding your credit limit, or S$50, whichever is greater | S$50 |

| CIMB | 3% of the outstanding balance or S$50, whichever is higher plus any amount that is overdue and/or exceeds your credit limit | S$50 |

| Citibank | 1% of the current balance plus 1% of any outstanding unbilled instalment amounts plus interest charges and fees or S$50, whichever is greater, plus any overdue amounts | S$50 |

| DBS & POSB | 3% of the statement balance or S$50, whichever is greater plus any amount that is overdue and/or exceeds your credit limit | S$50 |

| HSBC | 3% of the outstanding balance or S$50, whichever is greater | S$50 |

| Maybank | 3% of outstanding balance or S$20, whichever is higher, plus any outstanding amount "Past Due" from previous statements (part of COVID-19 Relief, till Dec 31, 2020 min payment is reduced to 1% or S$20) | S$20 |

| OCBC | S$50 or 3% of the total balance, whichever is higher, and any overdue amount | S$50 |

| Standard Chartered | S$50 or 8.33% of your principal plus interest, fees and charges, whichever is higher, plus any amount in the account balance exceeding your credit limit and any past due amount | S$50 |

| UOB | 3% of current balance or S$50, whichever is higher, plus any overdue amount | S$50 |

Note that while the fees listed above are current as of the time of writing, they are subject to change. You can always find your current minimum payment formula in your cardmember agreement. If you don't have a copy of it, you can call your bank and ask that a copy be sent to you.

What Happens if You Only Pay the Minimum Amount Due on Your Credit Card?

Although the credit card minimum payment requirement is meant to protect consumers, making just the minimum payments every month is a dangerous practice. For one, it can cause you to carry a balance for an extremely long time as well as have a negative impact on your credit score.

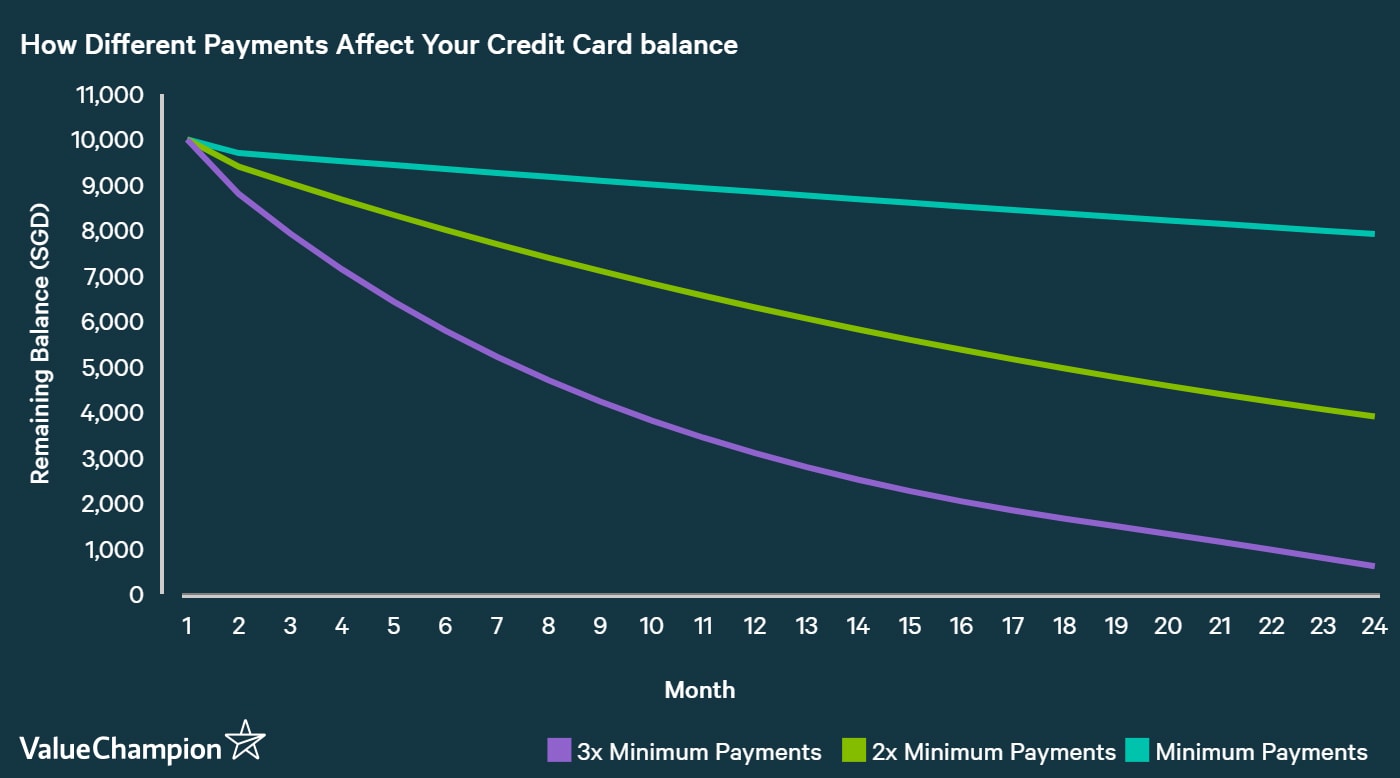

Only making the minimum payments can actually result in you having to pay down your balance for several years or more. For example, we modeled out and graphed the change in a sample outstanding credit card balance as a result of several different repayment options, including sticking to just the minimum. The graph below shows how quickly balances go down based over a 24-month period, for a principal balance of S$10,000 at an APR of 25%.

In the above example, the individual making just the minimum payments on the S$10,000 of balance would pay S$4,043 in interest charges over two years. Paying just twice the minimum payment reduces the interest charges by S$1,119. Those who could manage to pay 4 times the minimum payment would save $2,388 in interest. Extending this calculation also showed that it would take about 21 years for someone to pay off S$10,000 in credit card bill by only making the minimum payment.

Minimum Payment and Your Credit Score

Paying only the minimum monthly requirement on your credit card bill has no direct impact on your credit score. However, there are indirect effects that consumers should be aware of. The more your credit card balance grows each month, the higher your credit utilisation is – a factor that can negatively influence your credit score. Credit utilisation refers to the percentage of your total available credit limit you are using. For example, if your outstanding balance is S$400, and your available line of credit is S$1,000, your utilization would be at 40%.

In general, it is best to keep your credit utilisation below 30%. When you make just the minimum credit card payments, however, your balance and your credit utilisation declines by the lowest possible amount. If you are close to having maxed out your credit card, paying just the minimum will cause your issuer to report a high utilisation ratio to the credit bureaus.

Consequences of Paying Less Than The Minimum Credit Card Payment

There are many consequences of paying less than the minimum amount due on a credit card.

- Late payment fees

- Being reported to the credit bureaus

- Breaking a contractual obligation to pay the min amount due

- Other penalty fees

Here is a little more information about the three major consequences of paying less than the minimum amount due on your credit card:

- Late Fees: Your issuer will charge you a late fee that you will be required to pay in full on your next billing statement. The fee will make your next month’s minimum payment larger than what it would have otherwise been. This fee generally ranges from S$50 to S$80.

- Penalty APR: Paying less than the minimum amount due can cause your issuer to impose a penalty APR on your future balances. This special type of APR is much higher than average, often being as high as 29% to 30%.

- Credit Score: Since paying less than the minimum amount due counts as a late payment, it also has a negative impact on your credit score.

FAQs

A minimum payment on a credit card is the lowest payment you have to make each month to avoid incurring extra fees and to keep your account in good standing. This amount is typically set at 3% of your outstanding balance, or S$50, whichever is higher.

If you repeatedly pay only the minimum amount due each month, you will prolong the time it takes to repay the amount borrowed from the bank. As the balance grows, so will the fees charged and the as a result, your credit utilisation.Higher credit utilisation will have a negative impact on your credit score.

If you fail to make the minimum payment for at least two months, you will likely not be approved for another credit card, your overdue credit lines may get suspended, and the late payments will end up increasing your overall balance.

Read More:

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.