Best UOB Credit Cards 2024

With hundreds of cards with different kinds of rewards, it could seem impossible to narrow down the list to a few that best fits your situation. After reviewing 100+ credit card options, our experts came up to with the best credit cards from UOB to help make your decisions easier.

- UOB One: Highest flat rebate on the market, earn up to $300/qtr

- KrisFlyer UOB: 3mi/S$1 on dining, transport, shopping & travel

- UOB PRVI Miles Amex: Fee-Waiver + 20k bonus miles, 2.4 miles per $1 overseas

- UOB EVOL: Rebates on online and contactless spend with easy fee-waiver

- UOB Visa Signature: Up to 4mi/S$1 on local petrol, contactless & overseas

- UOB Preferred Platinum: Miles for online & mobile contactless spend

- UOB Absolute Cashback: Unlimited 1.7% cashback on all spend

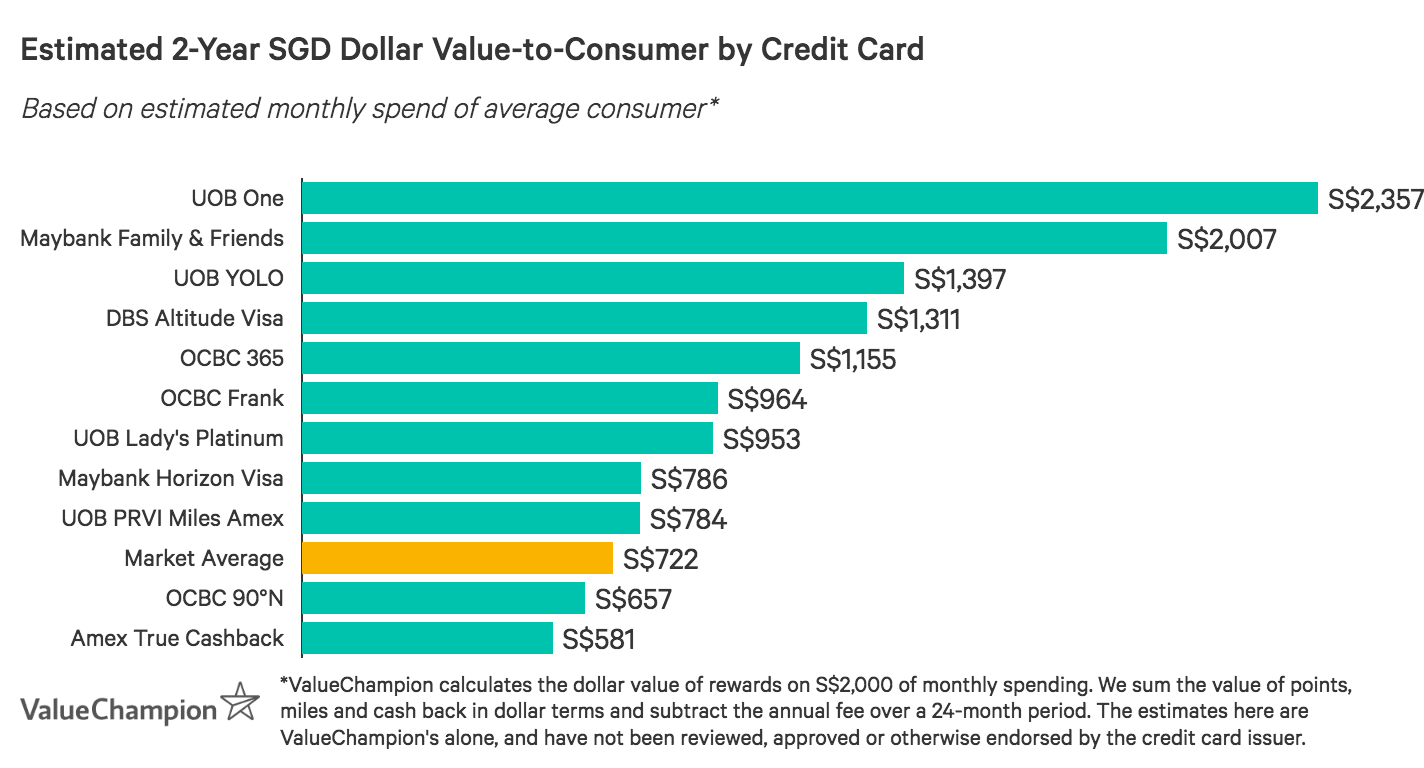

Compare Best UOB Credit Cards by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best UOB credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

- Highest flat rebate on the market, earn up to $300/qtr

- 3mi/S$1 on dining, transport, shopping & travel

- Fee-Waiver + 20k bonus miles, 2.4 miles per $1 overseas

- Rebates on online and contactless spend with easy fee-waiver

- Up to 4mi/S$1 on local petrol, contactless & overseas

- Miles for online & mobile contactless spend

- Unlimited 1.7% cashback on all spend

Compare Best UOB Credit Cards by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

UOB One Credit Card: Best Rebate for Stable Budgets

- Pros

- Good fit for budgets of at least S$2,000 per month

- Easy cashback on daily spend

- Gives rebates for paying bills

- Cons

- Doesn't fit inconsistent budgets

- Annual fee

UOB One Card is an extraordinary credit card for those with stable budgets. In fact, if you consistently spend S$2,000/month, you’ll earn the highest flat rebate on the market–5% on general spend, up to S$300/quarter, boosted to 10% on Grab & select UOB Travel and 6% on utilities bills. Lower or inconsistent spenders earn a still relatively high 3.33% rebate, capped at S$50 or S$100/quarter based on minimum spend level.

Cardholders even enjoy some of the highest petrol discounts on the market, with up to 24% fuel savings with SPC and 21.15% with Shell. Overall, UOB One Card is the perfect option if you’re a stable spender and want one, easy-to-use credit card that will maximise rebates. | |

- Pros

- Good fit for budgets of at least S$2,000 per month

- Easy cashback on daily spend

- Gives rebates for paying bills

- Cons

- Doesn't fit inconsistent budgets

- Annual fee

|

UOB One Card is an extraordinary credit card for those with stable budgets. In fact, if you consistently spend S$2,000/month, you’ll earn the highest flat rebate on the market–5% on general spend, up to S$300/quarter, boosted to 10% on Grab & select UOB Travel and 6% on utilities bills. Lower or inconsistent spenders earn a still relatively high 3.33% rebate, capped at S$50 or S$100/quarter based on minimum spend level.

Cardholders even enjoy some of the highest petrol discounts on the market, with up to 24% fuel savings with SPC and 21.15% with Shell. Overall, UOB One Card is the perfect option if you’re a stable spender and want one, easy-to-use credit card that will maximise rebates. |

KrisFlyer UOB Credit Card: Top Miles for Young SIA Loyalists

- Pros

- 3 mi per S$1 on SIA, SilkAir, Scoot & KrisShop

- Up to 3 mi on dining, transport, online shopping & travel

- Expedited KF Elite Silver status, Scoot privileges

- 10,000 annual bonus renewal miles

- Cons

- Just 1.2 mi on non-category overseas spend

- No lounge access perks

- No spend-based fee-waiver

KrisFlyer UOB Card is a great option for SIA loyalists–especially young adults who tend to fly on a budget. Cardholders earn 3 KF miles per S$1 on all spend with SIA brands (SIA, SilkAir, Scoot & KrisShop) and 1.2 miles per S$1 on general local & overseas purchases. This general rate is boosted to an incredible 3 miles on dining, transport, online fashion shopping & travel bookings with just S$800 annual spend with SIA brands. These categories are a great fit to the lifestyle of millennial travellers who are willing to commit to SIA airlines.

| |

- Pros

- 3 mi per S$1 on SIA, SilkAir, Scoot & KrisShop

- Up to 3 mi on dining, transport, online shopping & travel

- Expedited KF Elite Silver status, Scoot privileges

- 10,000 annual bonus renewal miles

- Cons

- Just 1.2 mi on non-category overseas spend

- No lounge access perks

- No spend-based fee-waiver

|

KrisFlyer UOB Card is a great option for SIA loyalists–especially young adults who tend to fly on a budget. Cardholders earn 3 KF miles per S$1 on all spend with SIA brands (SIA, SilkAir, Scoot & KrisShop) and 1.2 miles per S$1 on general local & overseas purchases. This general rate is boosted to an incredible 3 miles on dining, transport, online fashion shopping & travel bookings with just S$500 annual spend with SIA brands. These categories are a great fit to the lifestyle of millennial travellers who are willing to commit to SIA airlines.

|

UOB PRVI Miles Card: No-Fee Miles for Affluent Travellers

- Pros

- Great for rapid miles accrual

- Awards high spend on airlines & hotels

- Annual fee waiver with Amex card

- Cons

- Doesn't fit infrequent travellers with mostly local budgets

- Lacks luxury perks & privileges

UOB PRVI Miles American Express Card is the absolute best travel credit card for above-average spenders because of its top rewards rates and fee-waiver. Cardholders earn at some of the highest rates on the market–1.4 miles per S$1 local spend, 2.4 miles overseas, and 6 miles with major hotels and airlines. This matches or exceeds the rates offered by even the most expensive travel credit cards.

| |

- Pros

- Great for rapid miles accrual

- Awards high spend on airlines & hotels

- Annual fee waiver with Amex card

- Cons

- Doesn't fit infrequent travellers with mostly local budgets

- Lacks luxury perks & privileges

|

UOB PRVI Miles American Express Card is the absolute best travel credit card for above-average spenders because of its top rewards rates and fee-waiver. Cardholders earn at some of the highest rates on the market–1.4 miles per S$1 local spend, 2.4 miles overseas, and 6 miles with major hotels and airlines. This matches or exceeds the rates offered by even the most expensive travel credit cards.

|

UOB EVOL Card: Cashback for Young Adults

- Pros

- Easy to use cashback card

- Great for budgets of at least S$600/month

- Rewards all online and mobile spend

- Cons

- Cashback capped at S$60/mo

Formerly known as the YOLO Card, UOB EVOL Card has only gotten better for younger spenders. Where the YOLO Card's max cashback used to be active only on weekends, the new EVOL card awards the full 8% cashback any day of the week, so long as you use mobile contactless spend via Apply Pay, Google Pay, Samsung Pay or Fitbit Pay. In addition, the cashback for all online spend has been upgraded to 8% from 3%, and is no longer limited to just dining and travel.

| |

- Pros

- Easy to use cashback card

- Great for budgets of at least S$600/month

- Rewards all online and mobile spend

- Cons

- Cashback capped at S$60/mo

|

Formerly known as the YOLO Card, UOB EVOL Card has only gotten better for younger spenders. Where the YOLO Card's max cashback used to be active only on weekends, the new EVOL card awards the full 8% cashback any day of the week, so long as you use mobile contactless spend via Apply Pay, Google Pay, Samsung Pay or Fitbit Pay. In addition, the cashback for all online spend has been upgraded to 8% from 3%, and is no longer limited to just dining and travel.

|

UOB Visa Signature Card: Easy Miles for Occasional Travellers

- Pros

- 4 mi (2 UNI$) / S$1 local contactless & petrol

- 4 mi (2 UNI$) / S$1 overseas (inc. online)

- Free travel insurance

- Cons

- General spend earns 0.4 mi (0.2 UNI$) / S$1

- S$1k local + S$1k overseas min. spend

- Petrol rate excludes SPC & Shell

- Few travel perks

UOB Visa Signature Card is a great option for miles-seeking consumers with moderate budgets and variable travel schedules. Cardholders who spend at least S$1k overseas/month earn 4 miles/S$1 on foreign currency transactions. Those who spend S$1k/month locally earn 4 miles/S$1 on petrol & contactless transactions (both via Visa payWave and mobile digital wallets). These categories capture almost all types of spend, and those who hit both minimums (or spend S$2k in one category alone) can max out the 8k miles/month earnings cap. This cap has a value-to-consumer of about S$80, which is quite competitive.

| |

- Pros

- 4 mi (2 UNI$) / S$1 local contactless & petrol

- 4 mi (2 UNI$) / S$1 overseas (inc. online)

- Free travel insurance

- Cons

- General spend earns 0.4 mi (0.2 UNI$) / S$1

- S$1k local + S$1k overseas min. spend

- Petrol rate excludes SPC & Shell

- Few travel perks

|

UOB Visa Signature Card is a great option for miles-seeking consumers with moderate budgets and variable travel schedules. Cardholders who spend at least S$1k overseas/month earn 4 miles/S$1 on foreign currency transactions. Those who spend S$1k/month locally earn 4 miles/S$1 on petrol & contactless transactions (both via Visa payWave and mobile digital wallets). These categories capture almost all types of spend, and those who hit both minimums (or spend S$2k in one category alone) can max out the 8k miles/month earnings cap. This cap has a value-to-consumer of about S$80, which is quite competitive.

|

UOB Preferred Platinum: Boosted Miles for Online & Mobile-Pay

- Pros

- Great fit for smaller budgets seeking miles rewards

- Rewards online shopping

- Cons

- Lacks luxury perks for frequent travellers

- Doesn't fit traditional spenders uncomfortable w/ digital wallets

- Annual fee

UOB Preferred Platinum Card is the best miles-earning everyday credit card for modern spenders–especially those on a budget. Cardholders earn a competitive 4 miles (2 UNI$) for every S$1 spend online or with a mobile digital wallet (like Apple Pay, Google Pay, Fitbit Pay & more). These categories are incredibly flexible as there are no merchant restrictions and most merchants now accept contactless payments. As a result, tech-savvy individuals can easily earn miles for nearly all of their spend.

| |

- Pros

- Great fit for smaller budgets seeking miles rewards

- Rewards online shopping

- Cons

- Lacks luxury perks for frequent travellers

- Doesn't fit traditional spenders uncomfortable w/ digital wallets

- Annual fee

|

UOB Preferred Platinum Card is the best miles-earning everyday credit card for modern spenders–especially those on a budget. Cardholders earn a competitive 4 miles (2 UNI$) for every S$1 spend online or with a mobile digital wallet (like Apple Pay, Google Pay, Fitbit Pay & more). These categories are incredibly flexible as there are no merchant restrictions and most merchants now accept contactless payments. As a result, tech-savvy individuals can easily earn miles for nearly all of their spend.

|

UOB Absolute Cashback Card: Unlimited Cashback on All Spend

- Pros

- Unlimited cashback

- No min, caps or exclusions

- American Express Card privileges

- Cons

- Low cashback rate for smaller budgets

- Annual fee

UOB Absolute Cashback Card offers 1.7% limitless cashback, with no minimum spend and no exclusions, making this the highest unlimited cashback credit card. While a rate of 1.7% isn't as high as some other credit cards on the market, higher rates often come with monthly caps and restrictions. For more affluent spenders this credit card will earn higher cashback at the end of the month.

| |

- Pros

- Unlimited cashback

- No min, caps or exclusions

- American Express Card privileges

- Cons

- Low cashback rate for smaller budgets

- Annual fee

|

UOB Absolute Cashback Card offers 1.7% limitless cashback, with no minimum spend and no exclusions, making this the highest unlimited cashback credit card. While a rate of 1.7% isn't as high as some other credit cards on the market, higher rates often come with monthly caps and restrictions. For more affluent spenders this credit card will earn higher cashback at the end of the month.

|

Learn More About Maximising Your Rewards with UOB

UOB One Card vs HSBC Advance Card

| |

| HSBC Advance Card is the best flat rate card for high spenders. Customers earn an extraordinary 2.5% flat cashback after reaching a S$2,000 minimum monthly spend, and 1.5% cashback if spend is below S$2,000 with a monthly cap of S$70. An additional 1% bonus cashback can be earned simply by depositing at least S$2,000 in fresh funds to your account and charging five transactions. This additional step will allow you to raise the cashback cap from S$70 to S$300/month, which is S$3,600/year in savings– the highest earning potential for a capped credit card on the market! | |

UOB One Card vs American Express True Cashback Card

|

|

| American Express True Cashback Card is a great option for the highest spenders because it offers unlimited earning potential. Cardholders earn 1.5% unlimited cashback on all spend, boosted to 3% for the first 6 months (up to S$150). While these rates are lower than those offered by UOB One Card, high spenders may feel constrained by UOB One Card’s earning caps. If you spend S$7,000+/month, you’re more likely to maximise cashback with Amex True Cashback Card; if you spend closer to S$2,000/month, you may prefer UOB One Card. | |

UOB PRVI Miles Amex Card vs SC Visa Infinite X Card

| |

| Standard Chartered Visa Infinite X Card is one of the best options available for very wealthy travellers looking to rapidly accrue miles. The card's real stand-out feature is its sign-on bonus. Consumers who can place S$300k fresh funds with a SC Priority Banking account receive 10,000 bonus KrisFlyer miles (worth about S$10k when redeemed for first class air tickets). Placing S$800k earns 15,000 bonus miles, and Priority Private Banking clients who place S$1.5m in funds receive an astounding 300,000 bonus miles. Beyond the bonus, cardholders earn a standard 1.2 miles per S$1 local spend and 2 miles overseas and enjoy perks like free lounge access and hotel privileges.

| |

UOB EVOL Card vs OCBC Frank Card

|

|

| OCBC Frank Card is the best no-fee rebate credit card for young adults, offering 6% rebate for online spend and 5% on weekend entertainment & at select cafes (3% on weekdays). While these rates are lower than UOB EVOL Card's 8%, OCBC Frank Card has a minimum spend of just S$400 offline (compared to S$600 with UOB EVOL Card).

| |

UOB EVOL Card vs HSBC Revolution Card

| |

| Like UOB EVOL Card, HSBC Revolution Card rewards local dining and entertainment. However, HSBC Revolution Card stands apart by offering miles rather than cashback, offering a fee-waiver, and having no minimum spend requirement. Cardholders earn 2 miles per S$1 spend on local dining, entertainment and online spend (including bill-pay). In addition, they can avoid paying an annual fee by spending S$12,500/year. While this rewards rate equates to about 2% rebate, HSBC Revolution Card is far more flexible, and a better match for miles-seekers. However, if you can easily meet a higher minimum spend requirement and prefer cashback, UOB EVOL Card is a better fit. | |

| UOB One v. HSBC Advance |

|---|

| HSBC Advance Card is the best flat rate card for high spenders, if they are willing to consider opening an HSBC Advance account. Advance customers earn 3.5% flat rebate after S$2,000 spend (2.5% if below), up to S$125/month. They also never pay a fee. While this rate is lower than UOB One Card’s, the monthly cap is S$25 higher. If you spend about S$3,500/month, you can max out rewards with HSBC Advance Card and earn S$1,500/year. At the same spend level, you’d earn just S$1,200/year with UOB One Card, and you’d also need to pay an annual fee.

|

| UOB One vs Amex True Cashback |

|---|

|

|

| American Express True Cashback Card is a great option for the highest spenders because it offers unlimited earning potential. Cardholders earn 1.5% unlimited cashback on all spend, boosted to 3% for the first 6 months (up to S$150). While these rates are lower than those offered by UOB One Card, high spenders may feel constrained by UOB One Card’s earning caps. If you spend S$7,000+/month, you’re more likely to maximise cashback with Amex True Cashback Card; if you spend closer to S$2,000/month, you may prefer UOB One Card. |

| UOB PRVI Miles Amex vs SC Visa Infinite X |

|---|

| Standard Chartered Visa Infinite X Card is one of the best options available for very wealthy travellers looking to rapidly accrue miles. The credit card's real stand-out feature is its sign-on bonus. Consumers who can place S$300k fresh funds with a SC Priority Banking account receive 10,000 bonus KrisFlyer miles (worth about S$10k when redeemed for first class air tickets). Placing S$800k earns 15,000 bonus miles, and Priority Private Banking clients who place S$1.5m in funds receive an astounding 300,000 bonus miles. Beyond the bonus, cardholders earn a standard 1.2 miles per S$1 local spend and 2 miles overseas and enjoy perks like free lounge access and hotel privileges.

|

| UOB EVOL vs OCBC Frank |

|---|

|

|

| OCBC Frank Card is the best no-fee rebate card for young adults, offering 6% rebate for online spend and 5% on weekend entertainment & at select cafes (3% on weekdays). While these rates are lower than UOB EVOL Card's 8%, OCBC Frank Card has a minimum spend of just S$400 offline (compared to S$600 with UOB EVOL Card).

|

| UOB EVOLvs HSBC Revolution |

|---|

| Like UOB EVOL Card, HSBC Revolution Card rewards local dining and entertainment. However, HSBC Revolution Card stands apart by offering miles rather than cashback, offering a fee-waiver, and having no minimum spend requirement. Cardholders earn 2 miles per S$1 spend on local dining, entertainment and online spend (including bill-pay). In addition, they can avoid paying an annual fee by spending S$12,500/year. While this rewards rate equates to about 2% rebate, HSBC Revolution Card is far more flexible, and a better match for miles-seekers. However, if you can easily meet a higher minimum spend requirement and prefer cashback, UOB EVOL Card is a better fit. |

In some cases, owning a credit card can also boost the interest rate you can earn with a savings account with the same bank. This is true with UOB, which boosts rates with its UOB One Savings Account for account holders who spend at least S$500/month with a UOB One, UOB EVOL, or UOB Lady's credit card. Such spending earns an impressive +1.45% p.a. bonus to the 0.05% p.a. base. Account holders can further boost their interest rate by up to +2.38% p.a. by crediting their salary or making 3 GIRO debit transactions per month (boost varies by tiers across the total balance size). Altogether, someone who uses their UOB credit card every month and credits their salary can earn a maximum EIR of 2.44% p.a. at a S$75k balance. This is one of the higher savings account interest rates available on the market.

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.