DBS Altitude Visa Credit Card: No Annual Fee Miles Card

ValueChampion Rating ![]()

Pros

- Great for online travel bookings

Cons

- Those willing to pay an annual fee for more bonus miles

- Affluent travellers who are willing to pay a high fee for luxury travel perks

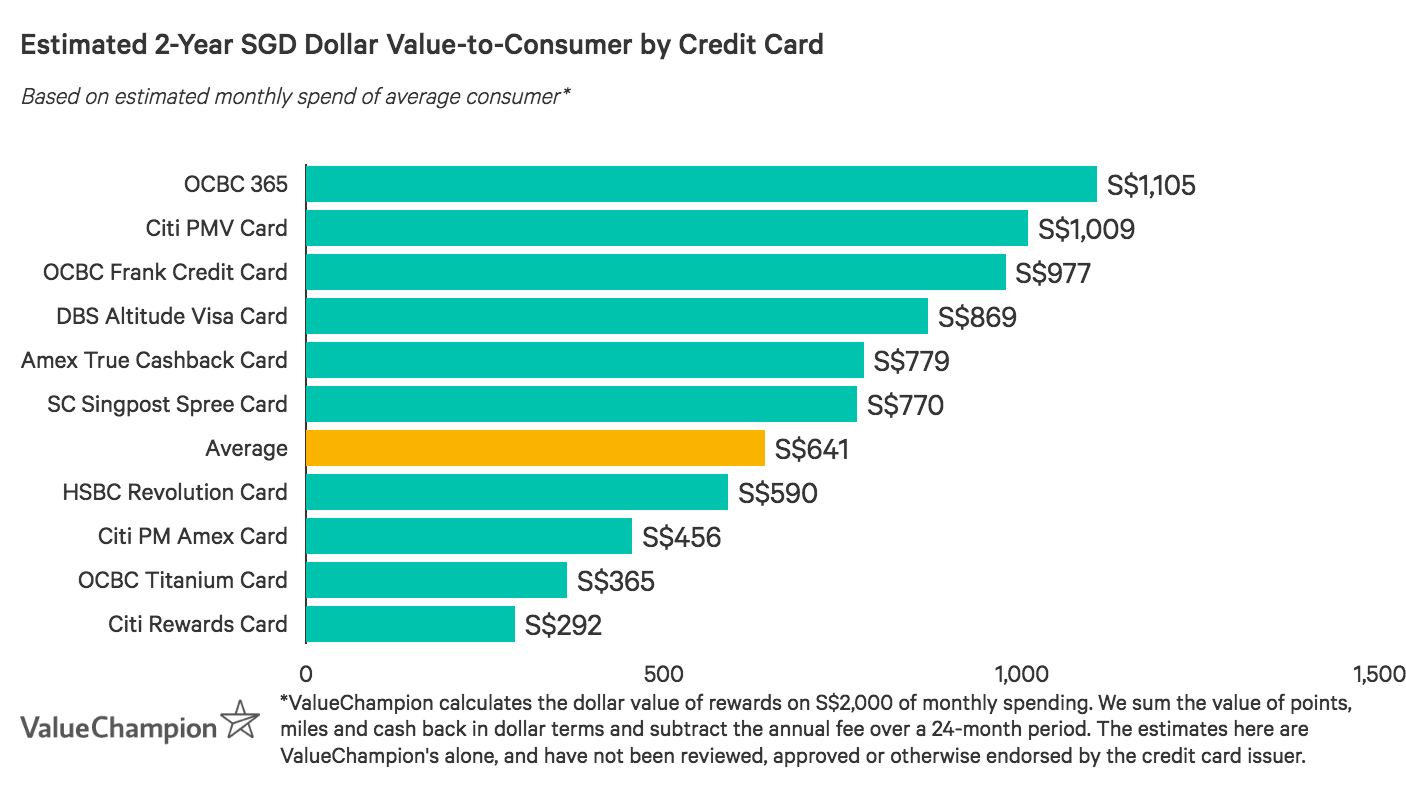

If you're an average spender looking to avoid annual fees while still earning miles and enjoying a variety of travel perks, DBS Altitude Visa Card is a great option for you. Cardholders earn 1.2 miles per S$1 local spend, 2 miles for overseas spend, and 3 miles for online flights and hotel transactions–plus promotional rates like up to 10 miles for transactions with Expedia and Kaligo. Travellers can quickly accumulate miles (that never expire) and can enjoy perks like free airport lounge visits. Even with these perks, which are on par with those of some pricier cards, DBS Altitude Visa Card remains affordable. The annual fee of S$194.4 is waived every year after with a annual spend of S$25,000, which is a reasonable spend for the average consumer.

DBS Altitude Visa Card Features and Benefits

|

|---|

Key Features:

|

What Makes DBS Altitude Visa Card Stand Out

DBS Altitude Visa Card is great for average spenders seeking a miles card with respectable rewards rates and a variety of travel perks, but without an annual fee. To being with, consumers earn 1.2 miles per S$1 local spend, 2 miles for overseas spend, and 3 miles for online flight and hotel transactions. While these rates are fairly standard, consumers boost earnings significantly through promotions. For example, consumers can often earn 6 miles per S$1 spend with Expedia and 10 miles per S$1 spend with Kaligo. Even better, miles never expire. Perks like a complimentary Digital Priority Pass membership that gives you 2 free airport lounge visits per year also adds value.

Despite its value, DBS Altitude Visa Card lacks some features found in other travel cards. The rewards rate of 2 miles per S$1 overseas spend is lower than some alternatives. Nonetheless, DBS Altitude Visa does offer a unique Miles Accelerator service which allows cardholders to earn an extra mile per any S$1 spend, as long as they're willing to pay an admin fee equal to 2% of the spend amount.. After taking into consideration the impact of this fee, this service essentially allows consumers to "buy" discounted miles at the cost of about 2 cents per 1 mile. Cardholders can then enjoy a redemption value of up to 8 cents per mile if they book business or first class for their flight. As a result, people who are more likely to fly with elevated ticket status can especially benefit from DBS Altitude Visa Card's accelerator service.

Ultimately, however, what may appeal most to consumers seeking affordable travel cards to DBS Altitude Visa Card is its easily waivable annual fee. The S$194.4 fee is waived as long as you meet the annual minimum spend of S$25,000. This breaks down to about S$2,100 in spend per month, which is reasonable for an average spender. In addition, cardholders who do pay the annual fee are rewarded with 10,000 bonus miles (worth $100), which effectively reduces the net cost to S$94.40. DBS Altitude Visa Card is a great option for average spenders who prefer not to pay a fee, but would still like to earn miles quickly and enjoy perks when they travel.

How Does DBS Altitude Visa Card's Rewards Program Work?

Use our quick and easy-to-read guide below to learn how you you can redeem DBS Altitude Visa Card rewards.

- Spend officially rewarded in DBS Points (redeemable as rewards vouchers, instant-redemption at select merchants, miles, and as payment for annual fee)

- Cardholder can redeem points for KrisFlyer Miles or Asia Miles in blocks of 5,000 DBS Points for 10,000 air miles through DBS Rewards Frequent Flyer Programme. Administrative fee of S$27.00 applies for each miles redemption.

- Cardholder can automatically convert points to KrisFlyer Miles on the 10th day of each quarter (January, April, July and October) through DBS KrisFlyer Miles Auto Conversion Programme. Points are converted in blocks of 500 DBS Points for 1,000 KrisFlyer Miles. Administrative fee for miles redemption does not apply, but participants must pay an annual fee of S$43.20.

- DBS Points earned through DBS Altitude Visa Card to not expire

DBS Altitude Visa Card Rewards Exclusions

Some credit card expenditures are ineligible for cash back or rebate. We identify these exclusions in the table below.

| Exclusion Category | Description |

|---|---|

| Bank Fees | Instalment payment plan purchases, preferred payment plans, balance transfer, fund transfer, cash advances, annual fees, interest, late payment charges, all fees charged by Bank, miscellaneous charges imposed by Bank (unless otherwise stated in writing by Bank) |

| Transfers & Bill Payments | Any top-ups or payment of funds to payment service providers, prepaid cards and any prepaid accounts (including EZ-Link, NETS FlashPay, Singtel Dash and Transit Link); payments done via AXS, SAM, eNETS |

| Institutional Payments | Payments to educational institutions, government institutions and services (court cases, fines, bail and bonds, tax payment, postal services, parking lots and garages, intra-government purchases and any other government services not classified here), insurance companies (sales, underwriting, and premiums), financial institutions (including banks and brokerages), and non-profit organisations |

| Betting or Gambling | Betting (including lottery tickets, casino gaming chips, off-track betting, and wagers at race tracks) through any channel |

How does DBS Visa Altitude Card Compare Against Other Cards?

Read our comparisons of DBS Altitude Visa Card with other cards and learn what makes each card unique in their own way. We compare and contrast each card to highlight its uniqueness to help you identify the card that you need.

DBS Altitude Visa Card v. Citi PremierMiles Visa Card

- Pros

- Frequent traveler perks

- Low fees

- Flexible miles redemption

- Cons

- Lacks luxury perks

- Not suitable for occasional travel

For consumers looking for a travel card that rewards overseas spend, has great perks, and has a reasonable annual fee, Citi PremierMiles Visa Card is an option worth considering. The card is very similar to DBS Visa Altitude Card. Both offer 1.2 miles per S$1 local spend and promotions with up to 10 miles for spend on select travel sites, as well as perks like travel insurance and 2 free visits to airport lounges. Both cards also offer an overseas rewards rate of 2 miles per S$1 spend. However, Citi PMV Card stands out for its welcome bonus of 21,000 miles (worth S$210) after S$7,500 in spend. DBS Altitude Visa Card, on the other hand, has an easily waivable annual fee while Citi PMV Card's annual fee is waived only the first year. Even though Citi PMV Card's fee is further offset by 10,000 renewal miles per year (worth S$100), the resulting fee is still higher than avoiding a fee altogether. If a consumer doesn't mind paying a moderate annual fee, they could gain more from the welcome bonus miles of Citi PMV Card. Consumers who would like to avoid an annual fee might want to instead consider DBS Altitude Card.

Read Our Full Comparative Analysis

DBS Altitude Visa Card v. HSBC Revolution Card

- Pros

- Great rewards on local dining and entertainment

- Online shopping perks

- No-fee card

- Cons

- Lacks rewards for frequent travellers who spend large amounts overseas

- Not suitable for low budgets

HSBC Revolution Card rewards consumers who spend socially on dining and entertainment and shop online. Even though rewards earned are easily converted into miles, this card is oriented more towards local and everyday expenditures than travel cards like DBS Altitude Visa Card. Cardholders earn 2 miles per S$1 spend on local dining and entertainment, as well as on a wide variety of online purchases, including travel and taxi bookings as well as insurance payments. Other spend, however, earns only 0.4 miles per S$1–so this card is not ideal for those with a more diversified expenditure or those who frequently make purchases abroad. The upside is that this card's annual fee of S$160.5 is easily waivable, requiring an even lower minimum spend of S$12,500 annually. The accessibility and affordability of HSBC Revolution Card make it easy for medium and even lower spenders to earn rewards, especially for local and social purchases. Consumers who'd still like to avoid an annual fee but who travel more frequently and desire travel perks might instead consider DBS Altitude Visa Card.

DBS Altitude Visa Card v. OCBC Titanium Rewards Card

- Pros

- 10 pts (4 miles) per S$1 on fashion & select retail (Qoo10, Amazon, & more)

- Fee waiver with S$10,000 annual spend

- Cons

- 1 pt (0.4 miles) per S$1 other spend

- Earnings capped at 48,000 miles per year (worth S$480)

Frequent fashion retail shoppers can make the most of their purchases with OCBC Titanium Rewards Card. All spend on clothes, shoes, bags, electronics, gadgets, and on transactions with select merchants are rewarded with 4 miles per S$1 spend–one of the highest rates on the market. Like DBS Altitude Visa Card, OCBC Titanium Rewards Card has an easily waivable annual fee–the S$192.6 fee is waived the first two years, and then subsequently with each annual spend of S$10,000. However, non-shopping spend earns only 0.4 miles per S$1 and travel perks are in the form of discounts (such as USD 27 per airport lounge visit) rather than as complimentary privileges. Consumers who spend much of their budget on shopping could maximise rewards with OCBC Titanium Rewards Card while avoiding an annual fee. Consumers who would like to avoid a fee but travel often and seek travel rewards should instead take DBS Altitude Visa Card into consideration.

DBS Altitude Visa Card v. UOB PRVI Miles American Express Card

- Pros

- Great for rapid miles accrual

- Awards high spend on airlines & hotels

- Annual fee waiver with Amex card

- Cons

- Doesn't fit infrequent travellers with mostly local budgets

- Lacks luxury perks & privileges

UOB PRVI Miles American Express Card is best fit for affluent travellers who care more about rapidly accruing miles than receiving luxury travel perks like airport lounge access. Cardholders can rapidly earn miles with high rewards rates like 1.4 miles per S$1 local spend, 2.4 miles overseas, and 10 miles on major airlines and hotels. Consumers can also earn an additional 20,000 miles per year with an annual spend of S$50,000. However, this card isn't fit for everyone because this minimum spend requirement averages to almost S$4,200 per month and there's an annual fee of S$256.8 which is only waived the first year. This card lacks travel privileges like unlimited airport lounge access and complimentary green fees, even though consumers can enjoy up to 8 free limo transfers per year. Ultimately, affluent consumers looking to rapidly earn miles for travel expenses can benefit from UOB PRVI Miles Amex Card as long as they are willing to forgo a few luxury perks. Consumers who are interested in fairly high rewards rates but aren't as willing to give up travel perks or pay a high annual fee might instead consider DBS Altitude Visa Card.

DBS Altitude Visa Card v. American Express Singapore Airlines KrisFlyer Card

- Pros

- Easy-to-use miles card

- No conversions & transfer fees

- Great rewards with Singapore Airlines

- Cons

- Not easy to maximise miles

- Lacks airline/travel rewards aside from SIA

American Express Singapore Airlines KrisFlyer Card is great for Singapore Airlines loyalist and travellers who value bonus miles and welcome gifts. Cardholders immediately earn 5,000 KrisFlyer miles with their first purchase, and can earn up to 7,500 miles within the first 3 months with a spend of S$5,000. After a S$12,000 spend, cardholders earn another S$150 cashback for use on Singapore Airlines. Beyond all of these promotions, consumers earn 1.1 miles per S$1 local spend and 2 miles per S$1 spend on SingaporeAir online and on the mobile app, as well as at KrisShop (in-flight and online). Still, Amex KrisFlyer Card does not offer luxe benefits like complimentary lounge access, limo transfers, or golfing privileges. Consumers looking for deals and promotions might want to consider Amex KrisFlyer Card, but those who still want to enjoy travel perks or annual fee waiver might prefer DBS Altitude Visa Card.

Read Also:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.