Fee Credit Cards Better Than No-Annual Fee Cards For Most Singaporeans: ValueChampion Analysis

Singaporeans are a financially savvy people. They are always looking for deals and opportunities to save more money. In terms of credit cards, however, "saving" on annual fees may not translate into more economic value. While many consumers are interested in getting rewards credit cards with no annual fee, it's actually more economical for an average person in Singapore to get a credit card with a fee.

ValueChampion calculated the rewards values of 10 most popular credit cards assuming an average consumer spending. Here’s what our analysis found:

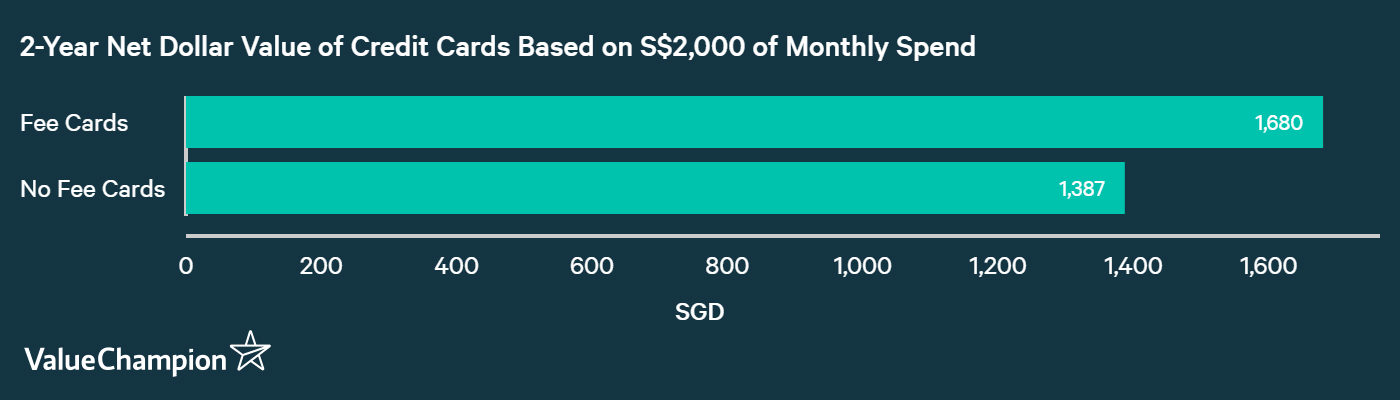

- For an average Singaporean spending around S$2,000 on their credit card per month, the best fee credit cards in Singapore yield 20% more in rewards than the best no fee credit cards.

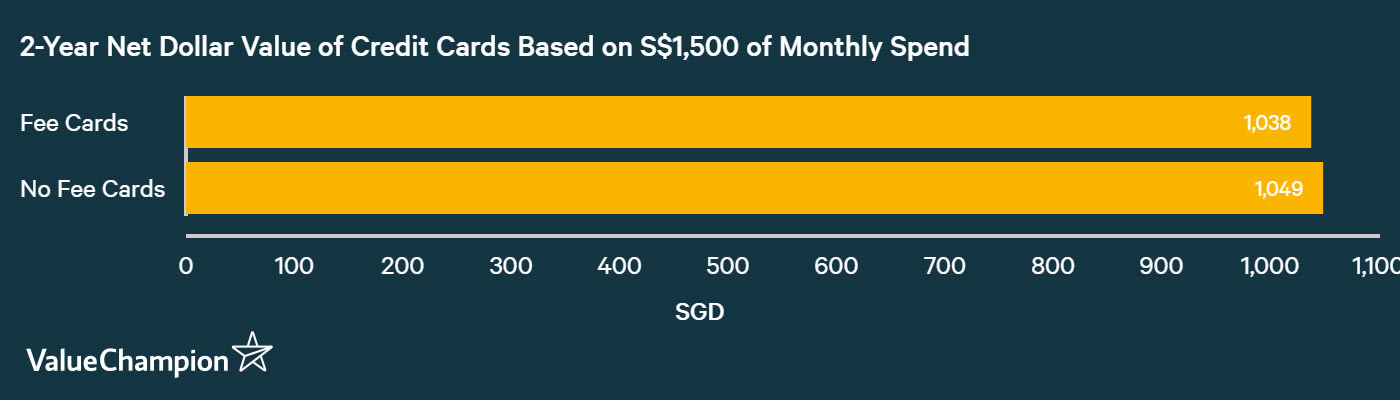

- For a consumer to prefer a no fee card to a fee credit card, he should spend less than S$1,500 per month (or S$18,000) on his credit card.

No Fee Credit Cards Yield Less Rewards Than Fee Cards

Unless you spend less than S$1,500 per year (or S$18,000 per year) on your credit card, you are likely to be better off with a card that charges an annual fee than with a card either does not charge a fee or provides an easy fee waiver. Since an average household spends about S$2,000 per month (according to the household expenditure conducted by the Singporean government), this rule of thumb should be applicable for most people in Singapore.

To get to this conclusion, we calculated how much a person can earn in cash back and miles (or points converted into miles) minus annual fees if he were to spend S$2,000 per month for 2 years for 10 of the best credit cards in Singapore. We also calculated how much one would earn on these cards if he were to spend S$1,500 per month instead of S$2,000. The result was quite interesting: the top 5 credit cards that carge an annual fee fee credit cards yielded about 20% more value than the best no annual fee credit cards in Singapore.

This is because many credit cards provide enough rewards to more than make up for the difference in annual fees. For instance, consider Citi PremierMiles Card or UOB One Card, easily two of the best credit cards in the market. Because they provide a tremendous amount of bonus miles and/or cash rebate, they tend to do better for most consumers than some of the best no fee credit cards.

Who Should Get a No Fee Credit Card?

This does not mean, however, that fee credit cards are always better than no fee cards. In fact, people who spend less than S$1,500 per month would be better off using a no fee card on average. This is because the rewards earned on the incremental S$500 of monthly spend (or S$6,000 annually) is just enough to make up for the annual fees that one has to pay for 2 years. For instance, most cards charge an annual fee of about $200 per year, which can increase up to S$600 in some cases. Since the best credit cards in Singapore do yield 2-5% on your spending, you have to spend about S$12,000 over 2 years to earn S$400 in cash rebate or miles and make up for the annual fee. Not only that, many "no fee" credit cards in Singapore come with a minimum annual spending requirement to qualify for an annual fee waiver. Spending less than S$1,000 per month can often lead to the loss of this fee waiver, leading to a lower "net dollar value" of a card.

For example, HSBC Revolution Card can match Citi PMV Card in terms of the amount of miles you can earn on your expenditures, while entirely waiving their annual fees for customers who meet a certain level of minimum spend requirement. Therefore, although you lose out on Citi PMV's rich bonus sign up bonuses, you can still net more miles with HSBC Revolution Card in the end by saving on your annual fee, especially if you spend less than S$1,500 per month. Not only that, a no-fee miles card like DBS Altitude Card is pretty much equivalent to Citi PMV Card even for people who spend S$2,000 or more, so your choice could depend entirely on your preference between bonus miles and annual fee waiver.

Conclusion

Though free is generally good, it's not necessarily the case for credit cards. If you spend more than S$1,500 on your card every month, cards that charge an annual fee will result in higher rewards rates (net of fees) than no fee cards. You can read more about how to choose the best credit card for your needs in our guide at the link.

Methodology

In order to calculate the value of rewards from each card, we assumed a monthly spending of S$2,000 of an average consumer, spread out across expenditure categories like travel, dining and groceries. Then, we were able to model out exactly how much cash rebate, miles or points one could earn by using a card over 2 years. We converted miles into dollars at rate of 1 Krisflyer mile to S$0.01; when a card provided points, we converted them into miles according to the bank and the card's specific conversion rates. By adding up all the values of cash rebate and miles (including bonus rebates and mile awards) minus the annual fee over 2 years, we were able to calculate how much value a card could generate for its user. For cards that offered fee waivers given a certain amount of annual expenditure, we considered them to be "no-fee" cards as long as the spending requirement was within range of the S$24,000 of annual spend for an average consumer (S$2,000 x 12 months).

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.