Everything to Know about Foreign Transaction Fees

Get the Best Credit Cards in Singapore

If you’ve ever used your credit card outside the country, then you may already have paid a foreign transaction (FX) fee. While this fee is typically explained in your card's Terms and Conditions, it is not immediately obvious what it is and how it is calculated.We have compiled this guide to address all the questions you may have about foreign transaction fees and how they are applied.

Table of Contents:

An Overview of Foreign Transaction Fees

A foreign transaction fee is an extra charge you have to pay when you buy something overseas, make a payment that is processed by a foreign bank or purchase something in a currency other than the Singapore dollar (SGD). A foreign transaction fee which is often referred to as an FX fee is generally around 2.5%–3.5% of your payment

A foreign transaction fee has two components

| Bank | Foreign Transaction Fee |

|---|---|

| CIMB | 2% |

| Citibank | up to 3.3% |

| DBS | up to 2.65% |

| OCBC | 2.25% |

| HSBC | 1.8% |

| Maybank | up to 1.75% |

| UOB | up to 2.25% |

To help you understand how transaction fees work, here is an example. Imagine that you are on vacation in the Netherlands. Using your HSBC Revolution Card you pay a S$100 for lunch. First, your credit card network –in this case, Visa–will charge 1% of the bill you paid which is S$1. Then your card issuer, HSBC, will charge 1.8% on your bill which is S$1.8. So, in total you will be paying $100 + (0.01100) + (0.018100) = $102.8.

Exchange rates are also applied to foreign transactions. Your card will not be charged S$10 when you buy an item that costs €10. Both Visa and MasterCard calculate the foreign exchange rates, and the FX fee is charged after the conversion is made. Sometimes, you may have the option to pay the expenditure in SGD through a system named 'Dynamic Currency Conversion,' but we advise that you avoid this process. More discussion on 'Dynamic Currency Conversion' is featured below.

How to Spot Credit Card Foreign Transaction Fees

Most banks do not advertise foreign transaction fees upfront unless they charge lower fees than market level. For the most part, you'll need to look at the Pricing and Information or the Terms and Conditions documents for your credit card to find the related information. The FX fees are typically listed under the ‘Fees’ section, near the cash advance and balance transfer fees.

When is an FX Fee Charged? Which Transactions are Foreign Transactions?

It is a bit tricky to explain what constitutes a foreign transaction. About a decade ago, a transaction was considered as a foreign transaction only if the transaction occurred on foreign soil. Now, however, a transaction is considered foreign if it requires involvement of a foreign bank in any part of the process.

In other words, some purchases – such as online purchases – may be considered foreign transactions even if they're made from your own country. Even the transactions that are executed in SGD may be processed through a bank overseas. In such cases, it is nearly impossible to find out about the fees ahead of time since very few companies provide such information.

Do FX Fees Count When Earning Credit Card Rewards? Are FX Fees Considered in Earning Credit Card Rewards?

Foreign transaction fees do not count toward rewards spending. Going back to the example we used earlier, you will only earn cashback on the actual lunch expenditure of $100, not on the added FX fee you also pay. The FX fee will be listed separately on your credit card bill. An FX fee is not eligible for any rewards like annual fees, late fees and interest fees. In fact, foreign exchange fees eat away your reward earnings and in some cases, can even leave you with a negative net total.

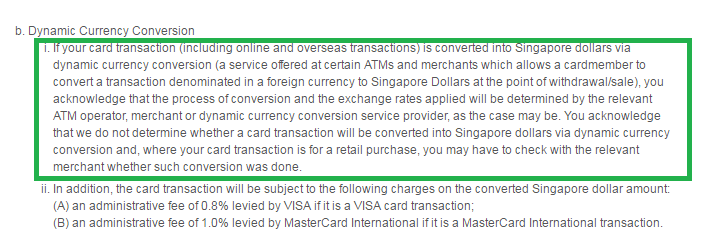

Dynamic Currency Conversion: Charges in SGD vs Local Currency

Sometimes while shopping in a foreign country you get the option of paying with SGD instead of the local currency. This process is called Dynamic Currency Conversion (DCC). While convenient, using DCC raises your expenses because of both the included FX fee and the higher exchange rate it uses.

Firstly, when you use DCC, you are charged high exchange rates since the merchant gets to set the currency exchange rate manually. They choose high rates to increase their profits. When you pay using the local currency instead, the transaction is handled by your credit card network and you receive the standard currency conversion rate. This way, you are not charged a higher exchange rate.

Dynamic Currency Conversions are not free of FX fees. You might think to use DCC as a way of avoiding foreign exchange fees, but that is not always the case. Some credit card companies will still charge you the fee while paying inSGD, because the transaction can still be processed by a foreign bank while using DCC. When that happens, it will be counted as a foreign exchange.

Where can you find how your bank handles foreign exchange fees? If you check the Terms and Conditions section you can find the foreign transaction fee represented in SGD or local currency.

If only local currency fees are listed in that section, it means your card issuer doesn’t charge aforeign transaction fee. DCC is a bad deal for you even if your credit card issuer doesn’t charge foreign exchange fees. The exchange rate in DCC might cost you higher than the 2.5% foreign exchange fee.

Finally, remember that you have the right to turn down a DCC offer from your merchant. Check your receipt before signing to make sure the total price is expressed in the local currency. If it is represented in SGD, inform your merchant and make sure you are charged in the local currency. If the receipt shows the total price in both SGD and the local currency, let them know that you prefer to pay in the local currency.

Summary

If you’re still confused about the whole process, just keep the following two points in mind.

- When traveling overseas, be sure to check how your credit card company is charging you.You can find this information online on their website in the ‘Terms and Conditions’ section.

- Don’t use dynamic currency conversion. The merchants will choose a high conversion rate, and despite using the DCC you may still have to pay an FX fee.

Read More:

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.