Citi Cash Back Credit Card: Easy Savings on Dining, Groceries and Petrol

Citi Cash Back Credit Card: Easy Savings on Dining, Groceries and Petrol

ValueChampion Rating ![]()

Pros

- Great dining and groceries rewards

- High petrol discounts

Cons

- Lacks shopping and entertainment rewards

- Not suitable for lower budgets

Citi Cash Back Credit Card is one of the best cards on the market for getting rebates on food and transport. With 6% cash back on dining, 8% cash back on groceries and petrol worldwide–plus discounts of up to 20.88% specifically at Esso & Shell–cardholders have an easy path to saving on a significant part of their household budgets. Relative to its S$800 monthly spend minimum, Citi Cash Back Card also offers one of the highest cashback limits at up to S$80 cashback per month.

Citi Cash Back Credit Card Features and Benefits

|

|---|

Key Features:

|

| Promotions:

|

Our Evaluation: The Easiest Way to Earn Cashback on Food

Citibank’s Citi Cash Back Card is an excellent card for everyday spending, but its best feature is that you can use it to earn cashback on just about any type of food purchase. You can earn 8% cashback on groceries and 6% cashback on restaurants and cafes, both in Singapore and worldwide. Consumers can earn cash back from everything from fine dining to fast food, caterers to convenience stores, supermarkets to specialty markets and more.

The card's petrol cash back is also flexible. You get fuel savings of up to 20.88% at Shell and Esso stations and 8% rebate at any other stations. Both the food and petrol cashback fall under Citi Cash Back Card's overall monthly rewards cap of S$80, which is generous compared to similar cards at other banks. Only the biggest spenders will find the rewards cap too low to maximise their potential cashback. Hence, for most spenders in Singapore, this cashback rebate is relatively attractive.

| Spending Category | Rebate | Total rate per month |

|---|---|---|

| Groceries | 7.75% bonus+ 0.25% | 8% |

| Dining | 5.75% bonus+ 0.25% | 6% |

| Petrol | 7.75% bonus+ 0.25% | 8% |

| All others | 0.25% | Unlimited |

Citibank frequently offers welcome bonuses, privileges, and ongoing promotions that may offset the annual fee for the Citi Cash Back Card. Over the years, we've noticed that this card usually has an active welcome bonus available to new card applicants. Cardholders also get access to Citi World Privileges and Citibank Gourmet Pleasures, which offer exclusive deals that may vary in cash value but definitely add to the card's appeal.

How Citi Cash Back Credit Card's Rebate Program Works

- Every 1 dollar of cash back earned is equal in value to S$1

- Cash back is credited to the cardholder’s account monthly, on the date of the account statement

- The minimum amount for cash back withdrawal is S$50 (and thereafter, multiples of S$10)

- While cash back does not expire, it is automatically forfeited when an account is closed

- Cash back cannot be combined or transferred

Before You Apply: Fees, Limits, and Exclusions

We think the Citi Cash Back Card is excellent in its major cashback categories of food and petrol, but it's no different from other credit cards in that there are certain rules to follow. First, the annual fee of S$194.40 kicks in after your first year. You should make sure that you use Citi Cash Back Card enough to earn at least that much value in cashback every 12 months. Given the monthly cap of S$80, most people should find this fairly easy.

Second, the card's minimum spend requirement of S$800 and the monthly rewards cap of S$80 set up an "ideal zone" of spend: spending too little drops your cashback to just 0.25%, as does any spending that exceeds your rewards cap. Check the table for an example of these different scenarios.

Citi Cash Back Rebates by Monthly Budget

| Low (S$799) | Medium (S$1,100) | High (S$2,000) | |

|---|---|---|---|

| Grocery | S$250 | S$300 | S$500 |

| Dining | S$300 | S$450 | S$1,000 |

| Petrol | S$249 | S$350 | S$500 |

| Total Rebate | S$0.15 | S$80 | S$80 |

As the table shows, missing the S$800 minimum by even a single dollar effectively wipes out your monthly cashback. Spending exactly S$800 divided evenly across groceries, dining and petrol would earn at least S$53. On the other end of the scale, spending more than S$1,100 split evenly in the three major categories won't earn you any further rewards because of the S$80 cap.

And finally, the following expenditures are ineligible for cash back or rebate with Citi Cash Back Card.

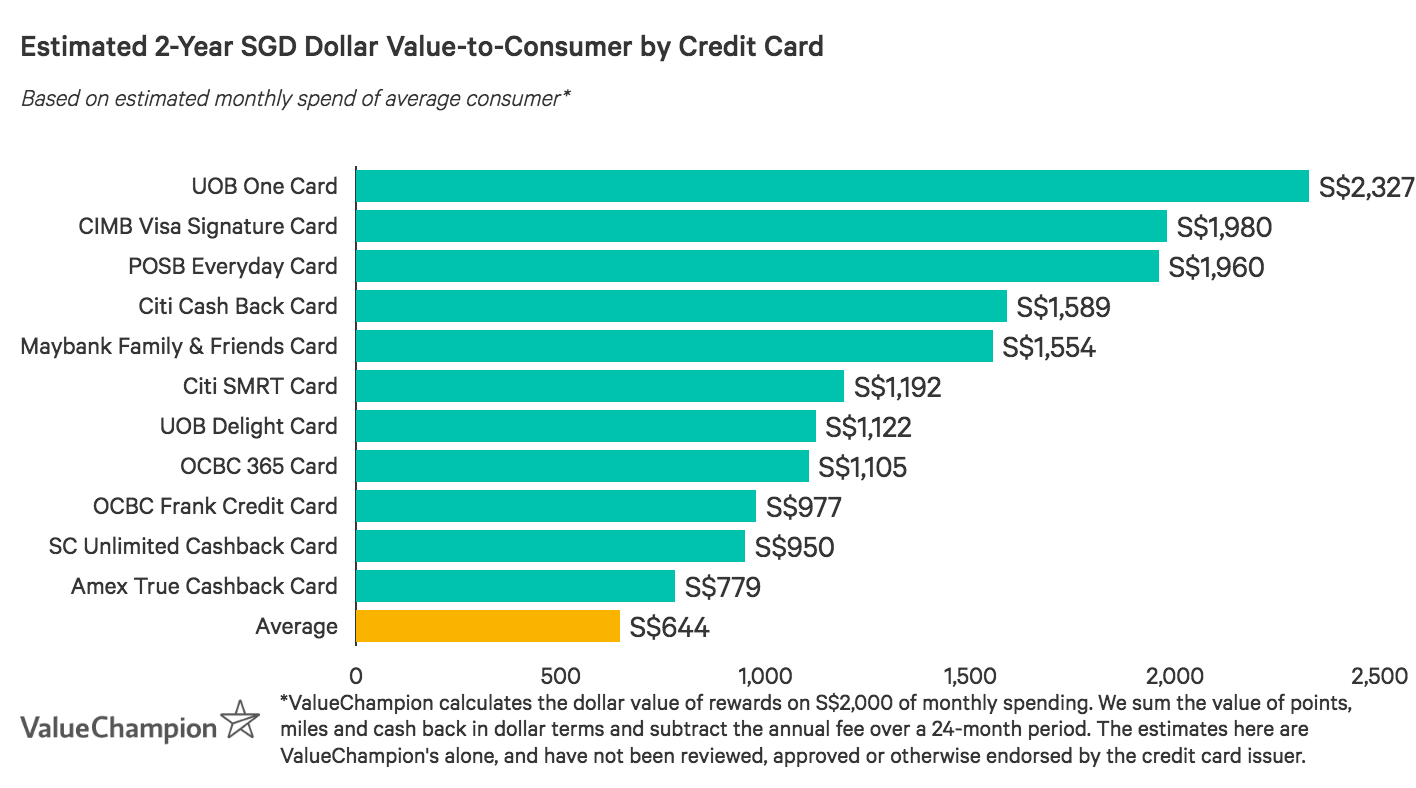

How the Citi Cash Back Credit Card Compares to Other Cards

- Pros

- Great dining and groceries rewards

- High petrol discounts

- Cons

- Lacks shopping and entertainment rewards

- Not suitable for lower budgets

Read our comparisons of Citi Cash Back Card with other cards and learn what makes each card unique in their own way. We compare and contrast each card to highlight its uniqueness to help you identify the card that you need.

Citi Cash Back Credit Card vs OCBC 365

- Pros

- 6% rebate on dining, 3% on groceries, transport, utilities, online travel

- Fee waiver with S$10,000 annual spend

- Up to 22.1% fuel savings at Caltex, 20.2% at Esso

- Cons

- 0.3% rebate on general spend

- High S$800 minimum spend requirement

Compared to Citi Cash Back Card, OCBC 365 offers elevated cash back rates across a broader range of spend categories, including travel transactions, transportation and recurring bills. This card also provides an annual fee waiver for those who spend S$10,000 per year. OCBC 365 also caps cashback at S$80 per month, which is the same as Citi Cash Back Card. Overall, consumers with decentralized spending across food, transport, utilities and online travel bookings could benefit more from the OCBC 365 Card, while those who spend a significant portion of their budget on food and petrol might be better served by Citi Cash Back Card.

Citi Cash Back Credit Card vs Citi SMRT Card

- Pros

- Good rewards rates for modest budgets

- SMRT$ rewards on EZ-Reload transactions

- Cons

- Not suitable for higher budgets

- Lacks travel and overseas rewards

Young professionals with a limited budget looking for cash back on daily purchases (including EZ-Reload auto top-ups) may benefit from Citi SMRT Card. Citi SMRT Cardholders immediately earn high cash back rates, with a minimum spend of S$500, across a broad range of spend categories (including online shopping and entertainment). The card also offers up to 5% SMRT$ on EZ Auto top-up SimplyGo. However, the Citi SMRT Card is not as flexible as the Citi Cash Back Card, which is not limited to specific merchants. Those who regularly spend at least S$800 monthly, however, can earn cash back more easily and without merchant restrictions through the Citi Cash Back Card.

Citi Cash Back Credit Card vs POSB Everyday Card

- Pros

- Benefits highly diversified spend with large food budgets

- Great fit for commuters seeking a convenient, an all-in-one card

- Cons

- Not suitable for consistent spend of S$2k+/mo

- Lacks travel rewards

- Has an annual fee

The POSB Everyday Card would especially benefit mothers and families with rebates for spend with select merchants across most spend categories. While the Citi Cash Back Card offers higher cash back rates for specific categories, the POSB Everyday Card offers rebates across a broader range including food, utilities, telecom bills and personal care. This wide variety of benefits allows mothers and families who spend on essentials to earn rewards quickly.

Citi Cash Back Credit Card vs Maybank Family & Friends Card

- Pros

- Good for budgets of S$800/month

- Awards 8% cashback on 5 categories of your choice

- 3 year annual fee waiver

- Great to use in Singapore, Malaysia, Indonesia and the Philippines

- Cons

- Merchant restrictions

- Lacks miles & travel perks

Consumers who frequently travel between Singapore and Malaysia would benefit from the cross-border flexibility of the Maybank Family & Friends Card. Maybank Family & Friends Card offers cash back rates up to 8% on fast food & food delivery, groceries, transport, petrol, data communications/online TV streaming & more in both countries. If your monthly spend falls below S$800, Citi Cash Back rate falls to 0.25%, whereas Maybank Family & Friends Card offers 5% cashback if monthly spend is between S$500 and S$799 (and 0.3% if below S$499). Both cards however, have the same S$800 monthly spend to qualify for bonus cashback rates and the same monthly cashback cap of S$80. Finally, Maybank F&F Card comes with a relatively easy fee-waiver. Nonetheless, rates apply only to spend in Singapore and Malaysia, so frequent travellers may prefer Citi Cash Back Card, which offers high rates both locally and overseas.

Citi Cash Back Credit Card vs UOB One Card

- Pros

- Good fit for budgets of at least S$2,000 per month

- Easy cashback on daily spend

- Gives rebates for paying bills

- Cons

- Doesn't fit inconsistent budgets

- Annual fee

The UOB One Card can be a great option for those who consistently spend about S$2,000 every single month. For instance, those who spend at least S$2,000 per month for 3 consecutive months are eligible for the greatest cash back rate of 5% on all spend, capped at S$100 per month (S$300 per quarter). This feature is especially helpful for those whose expenditures are spread out across many different spending categories outside of food & transportation. However, this reward decline dramatically to S$50/month for those who miss the S$2,000 requirement even for 1 month. But, if your spend is mostly concentrated in food & petrol, Citi Cash Back Card is still a great option to consider.

Methodology: How We Evaluate Credit Cards

Our analysis of consumer credit cards involves calculating the total value of a card's rewards rates, bonuses, and discounts minus the cost of its annual fee, rewards caps, and required spend. Temporary promotions and intangible perks are considered, but do not necessarily enter the equation when we calculate final value.

ValueChampion makes certain assumptions when estimating the rewards value of credit cards. These matter because most cards offer different cashback or miles rates based on the type of spend involved. Our profiles reflect a best guess at the spend decisions of a typical consumer on an average budget.

If you would like to see how our calculations work on your own budget, head over to our RealValue Rewards Calculator and type in how much you spend in various categories to see an instant comparison of the predicted rewards value of dozens of cards.

Read Also:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.