Best CIMB Credit Cards 2024

CIMB’s credit cards represent some of the most value-oriented products in Singapore, and they don’t pull punches in terms of rewards. CIMB offers a number of cards that have neither annual fee nor complications, making them the cheapest credit cards to use in Singapore. Here, we drill down on what makes CIMB’s credit cards brilliant and who may find them appropriate for their circumstances.

- CIMB Visa Infinite: Unlimited 2% cashback on travel, overseas and online spend in foreign currencies

- CIMB World MC: Unlimited 2% cashback on wine and dine, food delivery, entertainment, taxi & automobile, luxury goods and 50% off green fees

- CIMB Visa Signature: 10% cashback on online shopping, groceries, beauty and wellness, pet shops and cruises

- CIMB AWSM: Unltd 1% rebate on dining, entertainment & more for students

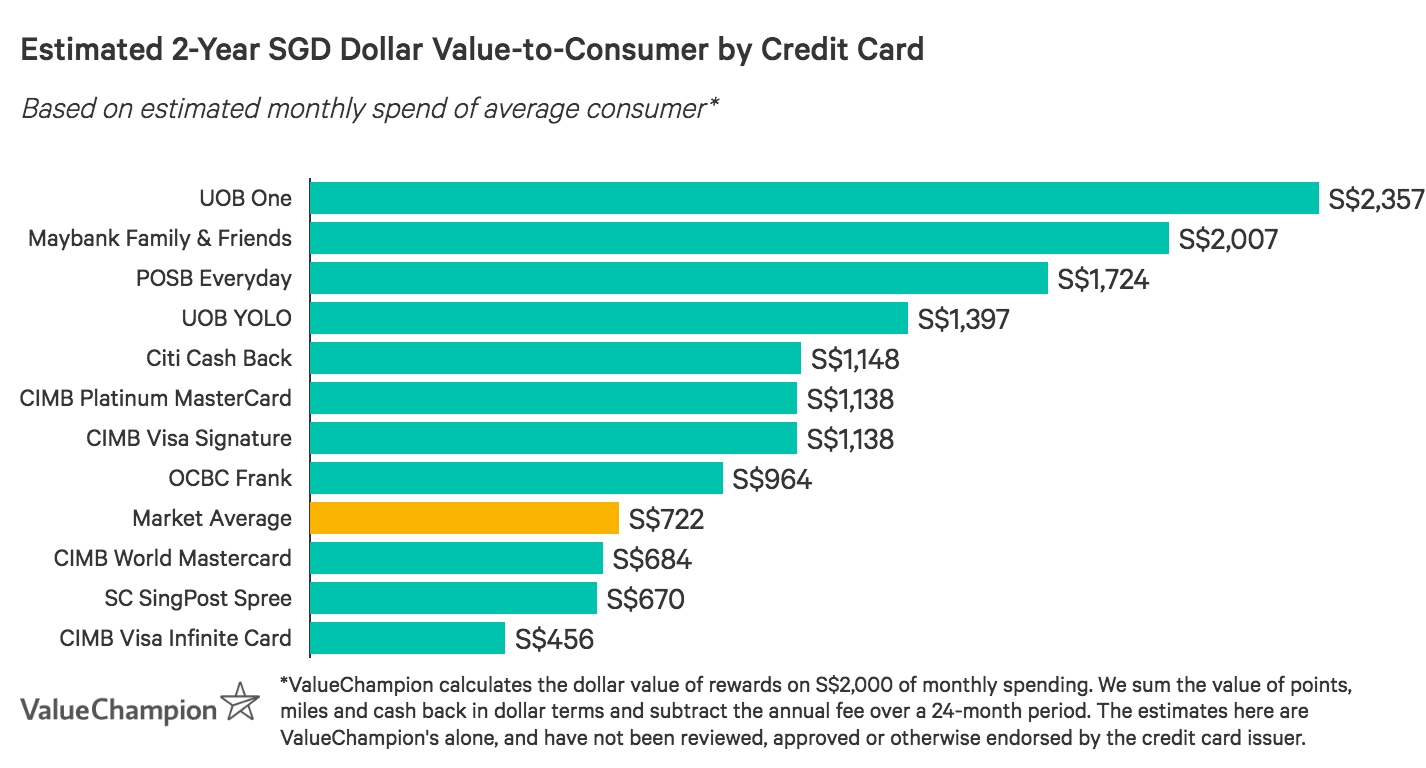

Compare Best CIMB Credit Cards by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best CIMB credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

- Unlimited 2% cashback on travel, overseas and online spend in foreign currencies

- Unlimited 2% cashback on wine and dine, food delivery, entertainment, taxi & automobile, luxury goods and 50% off green fees

- 10% cashback on online shopping, groceries, beauty and wellness, pet shops and cruises

- Unltd 1% rebate on dining, entertainment & more for students

Compare Best CIMB Credit Cards by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best CIMB credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

CIMB Visa Infinite Card: Unlimited Rebates for Travellers

| |

High-spending travellers can earn maintenance-free cashback with CIMB Visa Infinite Card. Cardholders earn unlimited 1% cashback on general spend with no minimum requirement, and 2% on travel and overseas spend after S$2,000 spend. This card is great for consumers who prefer rebates to miles, and who don't want to keep track of earning caps by category.

| |

|

|

High-spending travellers–especially those who enjoy golfing–can earn maintenance-free cashback with CIMB Visa Infinite Card. Cardholders earn unlimited 1% cashback on general spend with no minimum requirement, and 2% on travel and overseas spend after S$2,000 spend. This card is great for consumers who prefer rebates to miles, and who don't want to keep track of earning caps by category.

|

CIMB World MasterCard: Top Rebates for Affluent Socialites

| |

CIMB World MasterCard Credit Card is an excellent no-fee credit card for high spenders with sizeable leisure budgets. Cardholders earn unlimited 1% cashback on general spend and 2% on wine and dine (including food deliveries), movies & digital entertainment, taxi & automobile and luxury goods–with a minimum monthly spending requirement of S$1,000. Perks include access to MasterCard Airport Experiences and 50% off green fees at fairways across Asia. Even better, there's no annual fee, so cardholders never have to worry about added costs.

| |

|

|

CIMB World MasterCard Credit Card is an excellent no-fee credit card for high spenders with sizeable leisure budgets. Cardholders earn unlimited 1% cashback on general spend and 2% on wine and dine (including food deliveries), movies & digital entertainment, taxi & automobile and luxury goods–with no minimum requirement. Perks include access to MasterCard Airport Experiences and 50% off green fees at fairways across Asia. Even better, there's no annual fee, so cardholders never have to worry about added costs.

|

CIMB Visa Signature: Cashback on Beauty & Online Spend

| |

CIMB Visa Signature Card is a great no-fee cashback credit card for those who spend on groceries but also have a discretionary budget. Cardholders earn 10% cashback on beauty, online fashion, petcare, cruise lines and groceries after an S$800 minimum spend. Few credit cards offer elevated rewards for these spend categories, and none approximate this high of a rate. In addition, cardholders can earn up to S$100/month total–which runs to S$1,200/year.

| |

|

|

CIMB Visa Signature Card is a great no-fee cashback credit card for those who spend on groceries but also have a discretionary budget. Cardholders earn 10% cashback on beauty, online fashion, petcare, cruise lines and groceries after an S$800 minimum spend. Few credit cards offer elevated rewards for these spend categories, and none approximate this high of a rate. In addition, cardholders can earn up to S$100/month total–which runs to S$1,200/year.

|

CIMB AWSM: Best Rebate for Students

|

|

CIMB AWSM Card is one of the best options on the market for students as well as for low-income adults (earning less than S$30,000/year). Cardholders earn an unlimited 1% rebate on a variety of key spend categories: dining, entertainment, online shopping & telco. Even better, there’s no minimum spend requirements and the credit card is free forever. Finally, students also have access to CIMB Deals & Discounts, which offer dining privileges and regional promotions across Singapore, Indonesia & Malaysia.

| |

|

|

|---|

|

|

CIMB AWSM Card is one of the best options on the market for students as well as for low-income adults (earning less than S$30,000/year). Cardholders earn an unlimited 1% rebate on a variety of key spend categories: dining, entertainment, online shopping & telco. Even better, there’s no minimum spend requirements and the credit card is free forever. Finally, students also have access to CIMB Deals & Discounts, which offer dining privileges and regional promotions across Singapore, Indonesia & Malaysia.

|

Learn More About Maximising Your Rewards with CIMB

CIMB Visa Infinite Card v. SC Unlimited Cashback Card

| |

| Standard Chartered Unlimited Cashback Card offers cardholders 1.5% flat rebate with no cap on earnings–which is great for high spenders who typically feel constrained by monthly rewards caps. In addition, cardholders enjoy great transport perks: SC Unlimited Cashback Card is SimplyGo functional and offers up to 21.3% fuel savings with Caltex. There’s a S$192.6 fee, waived 2 years.

| |

CIMB World MasterCard v. Maybank World MasterCard

| |

| Maybank World MasterCard is the best miles-earning credit card on the market for golfers. Cardholders receive 2 free green fees/month at 100 fairways across 19 countries. In addition, every S$1 spend with select dining & retail merchants earns 10 points (4 miles). The annual fee is waived with S$24,000 annual spend.

| |

CIMB Platinum MasterCard v. Citi Cash Back Card

| |

| Both CIMB Platinum MasterCard and Citi Cashback Card reward spend on dining and petrol, but CIMB Platinum MasterCard offers a higher rewards rate (10% v. 8%) and has a lower minimum spend requirement (S$800 v. S$888). In addition, CIMB Platinum MasterCard doesn't charge an annual fee, while Citi Cashback Card charges S$192.6 annually.

| |

| CIMB Visa Infinite v. SC Unlimited Cashback |

|---|

| Standard Chartered Unlimited Cashback Card offers cardholders 1.5% flat rebate with no cap on earnings–which is great for high spenders who typically feel constrained by monthly rewards caps. In addition, cardholders enjoy great transport perks: SC Unlimited Cashback Card is SimplyGo functional and offers up to 21% fuel savings with Caltex. There’s a S$192.6 fee, waived 2 years.

|

| CIMB Visa Infinite v. Maybank World |

|---|

| Maybank World MasterCard is the best miles-earning credit card on the market for golfers. Cardholders receive 2 free green fees/month at 120 fairways across 25 countries. In addition, every S$1 spend with select dining & retail merchants earns 10 points (4 miles). The annual fee is waived with S$24,000 annual spend.

|

| CIMB Platinum MC v. Citi Cash Back |

|---|

| Both CIMB Platinum MasterCard and Citi Cashback Card reward spend on dining and petrol, but CIMB Platinum MasterCard offers a higher rewards rate (10% v. 8%). In addition, CIMB Platinum MasterCard doesn't charge an annual fee, while Citi Cashback Card charges S$192.6 annually.

|

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.