UOB One vs. OCBC 365 Credit Card Comparison 2024

If you're looking to earn cashback on daily essentials, you may have already considered UOB One Card or OCBC 365 Card. After all, these options are amongst the most popular everyday cards currently on the market. While both are quite competitive, they have very different rebate structures and ultimately reward different spending behaviours. To help you to decide which of these cards better suits your lifestyle, we've provided a detailed comparative breakdown in the guide below.

- Details of rebate system & structure

- General & boosted cashback rates

- Minimum spend requirements & monthly rewards caps

- Maximum potential annual earnings

- Travel insurance offerings

- Current petrol promotions & savings

- SimplyGo & mobile pay compatibility

- Extra rebate programmes & card-specific privileges

- Minimum age & minimum income requirements

- Annual fees, spend-based waivers & sign-on bonuses

- Foreign transaction fees

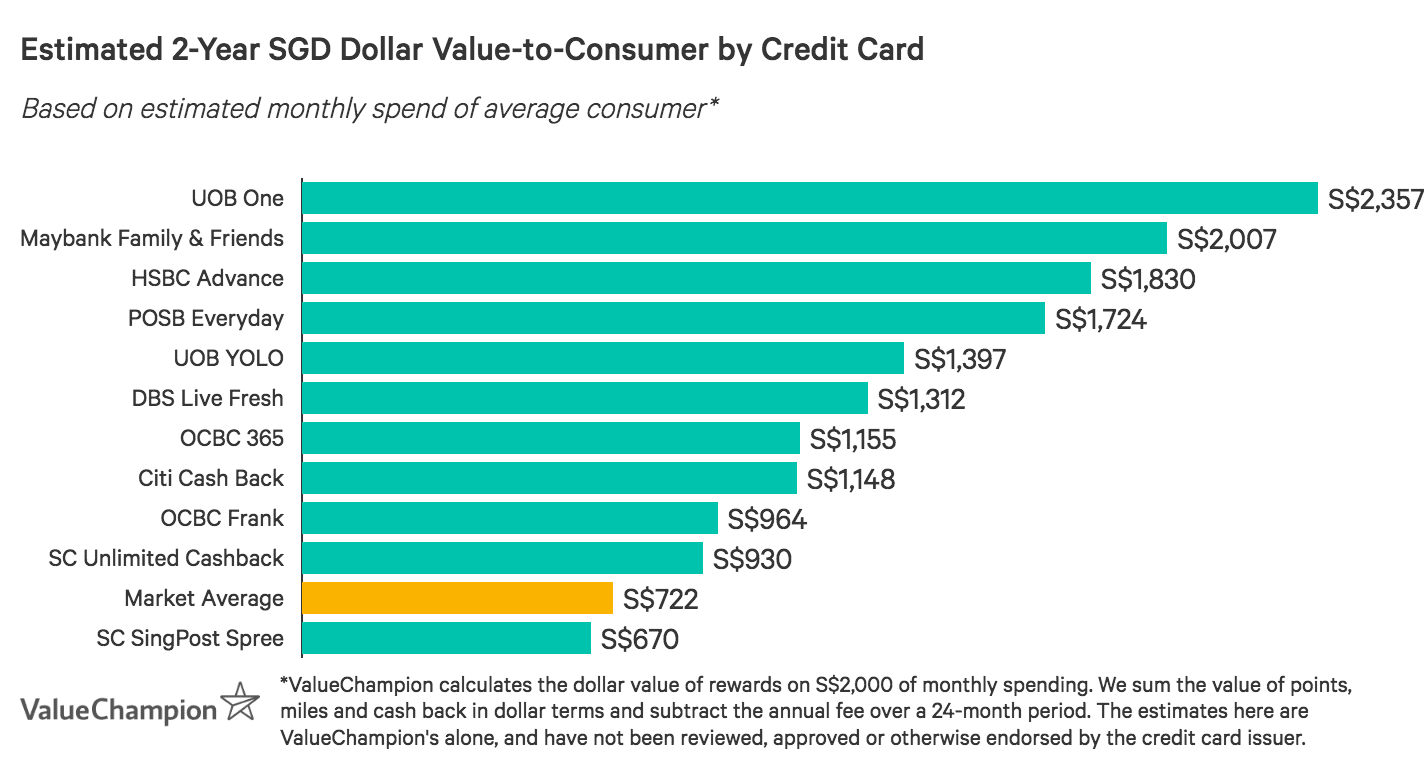

Comparison of Competitive Rebate Cards in Singapore by Dollar Value

Based on an average monthly spend of S$2,000, we analysed some of the most competitive rebate cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Comparison of Competitive Rebate Cards in Singapore by Dollar Value

Based on an average monthly spend of S$2,000, we analysed some of the most competitive rebate cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Overview: UOB One Card vs. OCBC 365 Card

UOB One Card and OCBC 365 Card are amongst the absolute best everyday cashback cards on the market for average consumers. In fact, consumers can earn competitive rebate rates on nearly all of their spend, without having to worry about merchant restrictions or individual category caps.

Summary Comparison Table: UOB One vs. OCBC 365

| Category | Feature | UOB One Card | OCBC 365 Card |

|---|---|---|---|

| Rates | Min. Spend Req. | S$500, S$1k or S$2k/quarter | S$800/mo |

| Rebate Boosts |

|

| |

| Earnings Cap |

|

| |

| Perks | Petrol Savings | Up to 22.66% fuel savings at SPC, 21.15% at Shell | Up to 22.1% savings at Caltex, 20.2% at Esso, 26.8% at Sinopec and 5% cashback at all other petrol stations |

| Compatibility | SimplyGo & Mobile Pay Compatible | SimplyGo & Mobile Pay Compatible | |

| Card Privileges | UOB SMART$, UOB Travel & Dining Advisor | Visa Concierge & Luxury Hotels Privileges | |

| Fees | Annual Fee | S$194.40 | S$194.40 |

| Waiver Option | Waived for 1 year | Waived for 2 years with min spend of S$10,000/year |

Nonetheless, UOB One Card and OCBC 365 Card also have their differences. In fact, their actual rebate structures vary significantly, ultimately catering to consumers with very different spending behaviours. We've outlined these differences in our analyses below so you can determine which option better aligns with your own needs and habits.

Rewards Rates: UOB One Card vs. OCBC 365 Card

While both competitive, UOB One Card and OCBC 365 Card have very different rebate structures. UOB One Card has a quarterly system, meaning that cashback rates are contingent on spending behaviour across 3 consecutive months and rewards are allocated to the consumer's account at the end of the period. Cardholders who consistently spend S$2k+/month every month for the full quarter to unlock the 6.67% rebate rate for selected merchants. Those who spend even slightly less during one of those months will earn just 5%, drastically reducing the earning-potential of the card. However, as consumers earn at a flat rate, there's no need to track categories, making UOB One quite convenient.

OCBC 365 Card, on the other hand, has a monthly rebate system and offers rate boosts in specific spend categories. This is great for consumers with variable budgets because one month's spend total will not influence the next's. As long as cardholders meet the S$800/month minimum requirement, they'll have access to OCBC 365 Card's high advertised rates. OCBC 365 Card does have category-driven rebates, however, so consumers should pay attention to what they're charging. This is especially true for frequent online shoppers, who will not earn elevated cashback on shopping sprees with this card.

Comparison Table: Cashback Rewards

| Feature | UOB One Card | OCBC 365 Card |

|---|---|---|

| Rebate Structure | Quarterly System | Monthly System |

| Rate Structure | Flat Rebate | Category Boosts |

| Base Rate | 0.03% | 0.30% |

| Min. Spend Req. | S$500, S$1k or S$2k | S$800 |

| Boosts |

|

|

| Mo. Rewards Cap |

|

|

| Max Annual Earnings | S$800+ | S$960 |

UOB One Card and OCBC 365 Card also differ in terms of rewards caps. UOB One Card's rebates are technically awarded on a quarterly basis; cardholders can earn up to S$200/quarter (averaging to S$66.67/month) if they've consistently spent at least S$2k/month. Earnings caps drop precipitously for lower spenders. In fact, those who spend less than S$1k any given month will only be eligible for a max rebate of S$50/quarter (averaging to S$12.50/month). OCBC 365 Card is a bit more forgiving. Cardholders can earn up to S$80/month, which can be achieved with as little as S$1.3k monthly spend. Ultimately, while stable spenders can earn more annually with UOB One Card (S$1.2k+), variable spenders are more likely to max out rewards with OCBC 365 Card.

Perks & Privileges: UOB One Card vs. OCBC 365 Card

UOB One Card and OCBC 365 Card have similar perks and privileges. Both offer competitive petrol savings, have SimplyGo compatibility, and can be used for "tap and pay" through a variety of channels. These are great for on-the-go consumers who value convenience. However, these cards do still have slight differences in their offerings.

Unlike OCBC 365 Card, UOB One Card comes with access to an ancillary rebate programme, called UOB SMART$. Cardholders earn SMART$ ("points" that can be redeemed to offset future purchases) for spend with merchants like BreadTalk, Cathay Cineplexes, Air Asia and more. This boost, paired with 1-for-1 dining deals and restaurant discounts through UOB Dining Advisor, ultimately makes UOB One Card a great match for consumers focused on savings.

Comparison Table: Card Perks & Privileges

| Feature | UOB One Card | OCBC 365 Card |

|---|---|---|

| Travel Insurance | S$500k Personal Accident; S$50k Medical, Evac & Repatriation incl. COVID-19 | S$200k Personal Accident; S$500 Medical; Travel Inconvenience |

| Petrol Savings | Up to 22.66% fuel savings at SPC, 21.15% at Shell | Up to 22.1% savings at Caltex, 20.2% at Esso, 26.8% at Sinopec and 5% cashback at all other petrol stations |

| Transit Perks | SimplyGo Compatible | SimplyGo Compatible |

| Mobile Pay | Google Pay, Apple Pay, Samsung Pay, UOB Mighty & more | Google Pay, Apple Pay, Samsung Pay, Fit Bit, Garmin & more |

| Card Privileges | UOB SMART$ Rebate Programme, UOB Travel Advisor, UOB Dining Advisor | Visa Concierge Services, Visa Luxury Hotels Privileges |

OCBC 365 Card, on the other hand, caters a bit more to travellers. Even though it's a cashback card, it offers a rather impressive free travel insurance plan that even includes travel inconvenience coverage. Cardholders are covered up to S$400 per person for flight delays, missed connections, baggage delays and baggage loss. OCBC 365 cardholders also have access to the Visa Luxury Hotels programme, which provides consumers with room upgrades, dining credits, free in-room WiFi, late checkout and more.

Fees, Promos & Requirements: UOB One Card vs. OCBC 365 Card

Another key point of difference between UOB One Card and OCBC 365 Card is their annual fee. UOB One Card has a S$192.6 annual fee, waived just the 1st year. OCBC 365 Card's S$192.60 fee is waived 2 years, then subsequently with just S$10,000 annual spend. While avoiding an annual fee is attractive, UOB One Card is still a better bet for most stable spenders. After all, consumers spending S$2,000/month can earn over S$1,000/year in rewards even after factoring in the fee.

Comparison Table: Requirements, Promos & Fees

| Feature | UOB One Card | OCBC 365 Card |

|---|---|---|

| Minimum Age | 21 yo | 21 yo |

| Minimum Income |

|

|

| Annual Fee | S$194.40 | S$194.40 |

| Waiver Option | Waived for 1 year | Waived for 2 years with min spend of S$10,000/year |

| Sign-on Bonus | ||

| FX Fee | 3.25% | 3.25% |

Comparison to Similar Rebate Credit Cards

While UOB One Card and OCBC 365 Card are quite competitive, there are still several worthwhile alternatives on the market. We've reviewed a few similar options below to help you identify whether or not they'd match your lifestyle.

POSB Everyday Credit Card: Top Promotional Rebates on Essentials

| |

POSB Everyday Card is well known for offering top rebates on daily essentials, ranging from food to recurring bills. You can typically earn as much as 10% on online food delivery, 5% on online shopping and 3% on dining. Recent changes to the card have made it both simpler to use and stronger in its overall rewards value.

| |

|

|

POSB Everyday Card is well known for offering top rebates on daily essentials, ranging from food to recurring bills. You can typically earn as much as 10% on online food delivery, 5% on online shopping and 3% on dining. Recent changes to the card have made it both simpler to use and stronger in its overall rewards value.

|

Citi Cash Back Card: Boosts for Food & Petrol

| |

Citi Cash Back Card is a great option for average consumers with considerable spend on food and fuel. Cardholders earn 8% cashback on global dining, groceries and petrol after S$800 minimum spend. Consumers can ultimately earn up to S$80/month–or S$960/year.

| |

|

|

Citi Cash Back Card is a great option for average consumers with considerable spend on food and fuel. Cardholders earn 8% cashback on global dining, groceries and petrol after S$888 minimum spend. While earnings are capped at just S$25/category (each maxed out with just S$312.5 spend), consumers can ultimately earn up to S$75/month–or S$900/year.

|

Maybank Family & Friends Card: Leading Rebates in SG & MY

| |

Maybank Family & Friends Mastercard is one of the absolute best options on the market for the average local and regional spender. Cardholders earn 5% rebate in Singapore and Malaysia on fast food & online food delivery, groceries, transport, petrol and data communications/online TV streaming, with just S$500 minimum spend. Those who spend S$800 earn at a boosted 8% rebate rate. Rewards are capped at S$80/month, which can be maxed out with just S$1k spend. At this budget level, cardholders also earn a fee waiver–the S$180.0 fee is waived with S$12k annual spend.

| |

|

|

Maybank Family & Friends Mastercard is one of the absolute best options on the market for the average local and regional spender. Cardholders earn 5% rebate in Singapore and Malaysia on fast food & online food delivery, groceries, transport, petrol and data communications/online TV streaming, with just S$500 minimum spend. Those who spend S$800 earn at a boosted 8% rebate rate. Rewards are capped at S$80/month, which can be maxed out with just S$1k spend. At this budget level, cardholders also earn a fee waiver–the S$180.0 fee is waived with S$12k annual spend.

|

HSBC Advance Credit Card: Top Flat Rate for Affluent Advance Customers

| |

If you're an above-average spender you may want to consider HSBC Advance Card. Customers earn an extraordinary 2.5% flat cashback after reaching a S$2,000 minimum monthly spend, and 1.5% cashback if spend is below S$2,000 with a monthly cap of S$70. An additional 1% bonus cashback can be earned simply by depositing at least S$2,000 in fresh funds to your account and charging five transactions. This additional step will allow you to raise the cashback cap from S$70 to S$300/month, which is S$3,600/year in savings– the highest earning potential for a capped card on the market! Those with above-average budgets can earn more with HSBC Advance Card than with either UOB One Card or OCBC 365 Card.

| |

|

|

If you're an above-average spender you may want to consider HSBC Advance Card. Customers earn an extraordinary 2.5% flat cashback after reaching a S$2,000 minimum monthly spend, and 1.5% cashback if spend is below S$2,000 with a monthly cap of S$70. An additional 1% bonus cashback can be earned simply by depositing at least S$2,000 in fresh funds to your account and charging five transactions. This additional step will allow you to raise the cashback cap from S$70 to S$300/month, which is S$3,600/year in savings– the highest earning potential for a capped card on the market! Those with above-average budgets can earn more with HSBC Advance Card than with either UOB One Card or OCBC 365 Card.

|

Cashback Credit Card Comparison Tables

| Credit Card | Min. Spend | Rebates | Cap |

|---|---|---|---|

| Citi Cash Back | S$800 |

| S$80/mo |

| Citi SMRT | N/A |

| S$50/mo |

| DBS Live Fresh | S$600 |

| S$60/mo |

| OCBC 365 | S$800 |

| S$80/mo |

| OCBC Frank | S$600 |

| S$75/mo |

| POSB Everyday | S$800 |

| S$30 |

| UOB One | S$500-S$2k |

| S$100+/mo |

| UOB EVOL | S$600 |

| S$60/mo |

| Credit Card | Travel Ins | Petrol Savings | Card Perks |

|---|---|---|---|

| Citi Cash Back | Coverage up to S$1M | Up to 20.88% fuel savings at Esso & Shell | Citi World Privileges, Citi Gourmet Pleasures |

| Citi SMRT | N/A | Up to 20.88% fuel savings at Esso & Shell | Citi World Privileges, Citi Gourmet Pleasures |

| DBS Live Fresh | N/A | Up to 14% fuel savings at Esso | #FreshDropFriday Sweeps |

| OCBC 365 | Coverage up to S$500k | Up to 22.1% savings at Caltex, 20.2% at Esso, 26.8% at Sinopec and 5% cashback at all other petrol stations | Visa Concierge & Luxury Hotels |

| OCBC Frank | N/A | Up to 23% fuel savings at Sinopec, 16% at Caltex, 14% at Esso | Frank Hot Deals |

| POSB Everyday | N/A | Up to 20.1% + 2% fuel savings at SPC | POSB Merchant Deals |

| UOB One | Coverage up to S$500k | Up to 22.66% fuel savings at SPC, 21.15% at Shell | UOB SMART$, UOB Travel & Dining Advisors |

| UOB EVOL | N/A | Up to 20% fuel savings at SPC, 14% at Shell | UOB SMART$, Mighty app offers |

| Credit Card | Annual Fee | Spend Waiver | Promotion |

|---|---|---|---|

| Citi Cash Back | S$194.40 | Waived for 1 year | |

| Citi SMRT Back | S$194.40 | Waived for 2 years | |

| DBS Live Fresh | S$194.40 | Waived for 1 year | |

| OCBC 365 | S$194.40 | Waived for 2 years with min spend of S$10,000/year | |

| OCBC Frank | S$80 | Waived 2 years, & subsequently with S$10,000 annual spend | |

| POSB Everyday | S$192.60 | Waived for 1 year | |

| UOB One | S$194.40 | Waived for 1 year | |

| UOB EVOL | S$192.60 | Waived for 1 year, no annual fees if min. 3 transactions per month for 12 consecutive months |

Learn More About Finding the Best Credit Card for You

- In-Depth Comparison: UOB One Card vs. UOB EVOL Card

- In-Depth Comparison: DBS Live Fresh Card vs. UOB EVOL Card

- In-Depth Comparison: DBS Live Fresh Card vs. POSB Everyday Card

- In-Depth Comparison: OCBC Frank Card vs. OCBC 365 Card

- In-Depth Comparison: POSB Everyday Card vs. OCBC 365 Card

- In-Depth Comparison: Citi Cash Back Card vs. Citi Rewards Card

- In-Depth Comparison of Unlimited Cashback Credit Cards

- How to Use a Credit Card

- How to Find the Best Rewards Credit Card

- Comparing Fee Credit Cards to No Annual Fee Cards in Singapore

- Understanding Credit Cards' Minimum Spend Requirements

- Understanding Rewards Caps on Monthly Earnings

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.