Best 0% Instalment Credit Cards 2024

Large purchases can be essential–perhaps if you're planning a wedding or buying a big gift–but paying all at once may not be feasible. In this case, an ideal credit card would come with an interest-free instalment plan enabling smaller payments over time. Our research team reviewed every 0% instalment plan on the market, analysing processing fees, instalment duration, and rewards for plan purchases, to identify the best options for consumers who want to split payments over time.

| Best Credit Cards for 0% Interest Instalment Plans | ||

|---|---|---|

| Best 0% Plan | OCBC Cashflo | 1% rebate on instalments, no processing fee |

| Online Shopping | DBS Woman's World | 4 miles/S$1 spend on online shopping w/ fee waiver |

| DBS Live Fresh | 5% cashback on online & contactless spend | |

| SC SP Spree | 3% cashback on foreign online & vPost spend, no minimums | |

| Best for Cashback | POSB Everyday | Rebates on essentials + transit perks |

| SC Unlimited | 1.5% unlimited cashback, locally & overseas | |

| HSBC Advance | 3.5% flat rebate, up to S$125/mo | |

| Travel & Overseas | DBS Altitude | 1.2 miles/S$1 locally, 2 miles overseas |

| CIMB Visa Infinite | Unltd. 2% rebate on travel & overseas | |

Best Credit Card for 0% Instalment Plan: OCBC Cashflo Card

- Pros

- 0% Interest instalment plan, no processing fee

- Trigger scheme automatically splits payments which earn rebates

- Fee waiver with S$10,000 annual spend

- Cons

- Just 0.5% rebate with spend below S$1,000 minimum

- Few additional benefits or perks

Here is why OCBC Cashflo Card is the best credit card in Singapore for 0% Instalment Plan.

If you’re looking for a dedicated credit card for shopping with a 0% interest instalment plan, OCBC Cashflo Card is the absolute best option. Not only does it waive processing fees–most plans charge 3% to 5% of the transaction amount–it also rewards split payments with one of the highest rebate rates on the market. All spend, including these payments, earns 1% flat cashback after S$1,000 spend (0.5% if below). The few competitors who do reward payments have processing fees that cancel out any gains.

Another unique benefit of OCBC Cashflo Card is its unique trigger system that automatically splits large transactions into instalments of 3-to-6 months. Most plans require cardholders to call ahead to apply or call in after to request approval retroactively, which is far less convenient. Finally, unlike most alternatives, OCBC Cashflo Card offers a fee waiver with just S$10,000 annual spend. Ultimately, this card is the only option that allows you to earn a net gain from splitting payments, and even offers market-leading convenience and a fee-waiver.

- Annual fee: S$160.50 (waived for two years)

- 1% flat rebate with S$1,000 minimum spend (0.5% if below), capped at S$100/mo

- 0% Interest Instalment Plan with no processing fee, payments earn rebates

- Trigger scheme automatically splits payments into 3- or 6-month instalments, at no extra cost

- 1% processing fee imposed on GE premiums under 12-month instalment plan

- Annual fee: S$160.50 (waived for two years)

- 1% flat rebate with S$1,000 minimum spend (0.5% if below), capped at S$100/mo

- 0% Interest Instalment Plan with no processing fee, payments earn rebates

- Trigger scheme automatically splits payments into 3- or 6-month instalments, at no extra cost

- 1% processing fee imposed on GE premiums under 12-month instalment plan

Best Online & Shopping Cards with 0% Instalment Plan

For those who like to shop online with 0% interest instalment plans, we’ve hand-selected the following cards.

Online Shopping Card with 0% Instalment Plan: DBS Woman’s World MasterCard

- Pros

- 0% interest payment plans available

- Good rewards for online shopping

- Online purchase protection

- Cons

- Lacks travel perks

- Limited rewards categories

Here is why DBS Woman’s World Card is the best 0% Instalment Plan credit card in Singapore for online shopping.

If you’re a big online shopper and prefer paying for your purchases over time, DBS Woman’s World Card is a great option that offers high rewards rates and a 0% instalment plan with no processing fee. Cardholders earn 4 miles per S$1 spend on online shopping, up to 8,000 miles/month (other spend earns just 0.4 miles per S$1 locally and 1.2 miles overseas, however).

What really makes DBS Woman’s World Card stand out, however, it that there’s no processing fee for up to 12 months. Most cards charge fees of 3%-to-5% of the transaction amount, which quickly adds up for larger purchases. DBS Woman’s World Card also comes with a fee-waiver with S$25,000 annual spend. Ultimately, this means online shoppers can spend stress-free and make payments over time while avoiding all kinds of added costs, from interest & processing to annual fees.

- Annual fee: S$194.40 (first year- waived)

- Subsequently waived w/ min annual spend of S$25,000

- 20 miles per S$5 spend on online purchase and, 6 miles by S$5 spend on overseas spend

- 2 miles per S$5 spend on all other purchases

- 0% Interest DBS Payment Plans

- e-Commerce protection on online purchases

- Annual fee: S$194.40 (first year- waived)

- Subsequently waived w/ min annual spend of S$25,000

- 20 miles per S$5 spend on online purchase and, 6 miles by S$5 spend on overseas spend

- 2 miles per S$5 spend on all other purchases

- 0% Interest DBS Payment Plans

- e-Commerce protection on online purchases

Credit Card for Online & Mobile Pay: DBS Live Fresh Card

- Pros

- Great rewards on contactless payment methods (Visa payWave)

- Green cashback on eco-eateries and retailers

- Various entertainment discounts and promotions

- Cons

- Lacks travel and overseas spend rewards

- Not suitable for low budgets

- New DBS/POSB cardmembers can get S$150 cashback when you apply through ValueChampion

- Enter the promo code 150CASH and spend a minimum of S$800 within 60 days of card approval to be eligible

Here is why DBS Live Fresh Card is the best 0% Instalment Plan credit card in Singapore for online & mobile pay.

If you’re somewhat tech-friendly and looking for all-in-one convenience, DBS Live Fresh Card is an excellent rebate card that rewards online & contactless purchases. Cardholders earn 5% cashback for online spend and payments made with online wallets via Visa payWave. This makes it easy to earn on just about everything you buy, online or offline.

What’s even better about DBS Live Fresh Card is that bigger purchases can easily be split into interest-free instalments with My Preferred Payment Plan. Transactions as low as S$100 can be split across 3, 6 or 12 months with no processing fee. Most plans only split transactions of S$500+ and charge processing fees of up to 5%. This makes DBS Live Fresh Card’s plan more accessible and affordable, especially for online shoppers.

In addition, DBS Live Fresh Card has SimplyGo functionality. This means you can use this card to earn about just about all of your purchases–including the biggest ones–as well as to make your commute more convenient. While there’s a S$600 minimum requirement, cardholders can earn up to S$60/month, so average spenders comfortable with mobile wallets can definitely benefit with DBS Live Fresh Card.

- Annual fee: S$194.40 (first year - waived)

- 5% rebate on online spend & visa contactless spend, including games purchases and SimplyGo rides

- Additional 5% cashback on sustainable spend (eco-eateries, eco-retailers and eco-transport)

- 0.3% cashback on all other spend

- Split your income tax, education and insurance payments with 0% interest and no fees with DBS Payment Plan

- Cashback capped at S$75/month

- Annual fee: S$194.40 (first year - waived)

- 5% rebate on online spend & visa contactless spend, including games purchases and SimplyGo rides

- Additional 5% cashback on sustainable spend (eco-eateries, eco-retailers and eco-transport)

- 0.3% cashback on all other spend

- Split your income tax, education and insurance payments with 0% interest and no fees with DBS Payment Plan

- Cashback capped at S$75/month

Foreign Currency Online Shopping Card with 0% Interest Instalment Plan: Standard Chartered SingPost Spree Card

- Pros

- Great for monthly budgets below S$500

- Rewards overseas retailer shopping

- Cons

- Not suitable for monthly budgets of S$500+

- Lacks local shopping rewards

Here is why Standard Chartered SingPost Spree Card is the best 0% Instalment Plan credit card in Singapore for foreign currency online shopping.

Standard Chartered SingPost Spree Card is an excellent option for online shoppers who mostly spend with merchants overseas. Cardholders earn 3% cashback on foreign online & vPost transactions, 2% for local online & contactless purchases, and 1% on general spend, with no minimum requirement–making this card a great option for lower spenders.

SC SingPost Spree Card also comes with the EasyPay, a 0% interest instalment plan that splits transactions of S$500+ across 6 or 12 months. Unlike with most competitors, cardholders earn rewards upfront on purchases made on the plan. There is a 5% processing fee, however, which is worth keeping in mind. Ultimately, SC SingPost Spree Card is a great option if you make purchases on sites like Amazon in foreign currency, and want to earn rewards for these purchases even if you split payments into instalments.

- Annual fee: S$192.60 (waived for the first 2 years)

- 3% cashback on foreign online & vPost transactions, 2% local online & contactless transactions

- 1% cashback on general spend

- Up to 25% discounts with vPost

- Online Price Guarantee

- Up to 16% fuel savings with Caltex

- Annual fee: S$192.60 (waived for the first 2 years)

- 3% cashback on foreign online & vPost transactions, 2% local online & contactless transactions

- 1% cashback on general spend

- Up to 25% discounts with vPost

- Online Price Guarantee

- Up to 16% fuel savings with Caltex

No-Fee Cashback for Beauty & Online Fashion: CIMB Visa Signature Card

- Pros

- Rewards online shopping, groceries and beauty spend

- Rewards pet spend and cruises

- No annual fee credit card

- Cons

- Lacks discounts on transport & petrol

- Speciliazed spend

- Doesn't fit frequent travellers

Here is why CIMB Visa Signature Card is the best no-fee cashback credit card in Singapore for beauty and online fashion.

If you’re interested in a 0% interest instalment plan but also want to maximise overall cashback, CIMB Visa Signature Card is worth considering. Cardholders earn a market-leading 10% rebate on a variety of expenses, after just a S$800 minimum: groceries, online fashion shopping, beauty spend, petcare, and transactions with cruise lines. Cumulatively, cardholders can earn up to S$100/month, which is quite respectable by market standards.

Cardholders also earn cashback for purchases made on the card’s 0% i.Pay Plan. While the rebate is just 0.2%, few cards reward such purchases at all. Transactions of S$500+ can be split into 6-to-12 month instalments with a 3% processing fee–which is lower than with many alternatives–and larger transactions of S$1,000+ can be split across 24 months with a 5% processing fee. CIMB Visa Signature Card stands out because you can earn top rates as you shop, earn on payments, and never pay an annual fee–making it an exceptional option for those seeking maintenance free cashback and a 0% interest instalment plan.

- Annual fee: free for life

- 10% cashback on groceries, online shopping, beauty, petcare & cruises

- Unlimited 0.2% cashback on all other retail purchases

- Free travel insurance & global concierge

- CIMB 0% Interest i.Pay Instalment Plan

- Annual fee: free for life

- 10% cashback on groceries, online shopping, beauty, petcare & cruises

- Unlimited 0.2% cashback on all other retail purchases

- Free travel insurance & global concierge

- CIMB 0% Interest i.Pay Instalment Plan

Best Cards with 0% Interest Instalment Plans for Cashback

No matter the size of your budget, sometimes it’s best to split purchases into instalments. We’ve identified cards with 0% interest instalment plans that also offer great benefits for high spenders.

Best Rebate Card for Essentials + Transit Perks: POSB Everyday Card

- Pros

- Benefits highly diversified spend with large food budgets

- Great fit for commuters seeking a convenient, an all-in-one card

- Cons

- Not suitable for consistent spend of S$2k+/mo

- Lacks travel rewards

- Has an annual fee

Here is why POSB Everyday Card is the best rebate credit card in Singapore for rebates on essentials & transit perks.

With POSB Everyday Card, you can earn some of the highest cashback rates on the market for daily essentials. So long as you spend S$800 per month, you can earn up to 10% rebate on dining, groceries, transport, personal care and even recurring bills. Another perk of POSB Everyday Card is its all-in-one convenience. Not only does the card have ATM and credit capabilities, it can also be used for contactless payments for public transit fares.

In terms of its 0% interest instalment plan, POSB Everyday cardholders can split payments as low as S$100 across up to 12 months with no interest and no processing fee. This makes shopping nearly stress-free. Ultimately, if you’re making purchases for your family or just want rebates on daily essentials, POSB Everyday Card is one of the best options to maximise rewards.

- Annual fee: S$194.40 (first year - waived)

- 10% cash rebates on online food delivery (foodpanda, Deliveroo and WhyQ ) and 3% on other dining spend

- 5% cash rebates on online shopping (Amazon, Lazada, Qoo10, Shopee, RedMart, iHerb & Taobao)

- 3% cash rebates on dining spend

- 0.3% cash rebate on all other spend

- DBS Payment Plan: pay 0% interest, up to 24 months

- Annual fee: S$194.40 (first year - waived)

- 10% cash rebates on online food delivery (foodpanda, Deliveroo and WhyQ ) and 3% on other dining spend

- 5% cash rebates on online shopping (Amazon, Lazada, Qoo10, Shopee, RedMart, iHerb & Taobao)

- 3% cash rebates on dining spend

- 0.3% cash rebate on all other spend

- DBS Payment Plan: pay 0% interest, up to 24 months

Best Unlimited Cashback Card + Transport Perks: Standard Chartered Unlimited Cashback Card

- Pros

- Unlimited 1.5% flat cashback

- No minimum spend requirement

- Up to 21% fuel savings with Caltex

- Cons

- No boosted rates in specific categories

- No travel perks

Here is why Standard Chartered Unlimited Cashback Card is the best unlimited cashback credit card in Singapore with transit perks.

If you’re a high spender, you’re earnings may be constrained by typical cashback caps–in this case, it’s worth considering Standard Chartered Unlimited Cashback Card. Not only do cardholders earn 1.5% unlimited cashback on all spend, they’re also privy to great transport benefits. Similar cards come with very few perks, so SC Unlimited Cashback Card stands out for its SimplyGo functionality and fuel savings up to 21% with Caltex.

Another benefit of SC Unlimited Cashback Card is that cardholders can access EasyPay, a 0% interest instalment plan that rewards purchases upfront. Consumers can split purchases of at least S$500 across 6 or 12 months and immediately earn cashback. Most plans exclude such transactions from earning rewards at all. However, it’s worth noting that instalments come with a 5% processing fee, which detracts from the value of cashback earned. Ultimately, SC Unlimited Cashback Card is the best option for high spenders looking for transport benefits, and who want to earn cashback on all spend–even purchases split into instalments.

- Annual fee waived for two years

- Unlimited 1.5% cashback on all spend

- Caltex petrol discounts up to 21%

- Annual fee waived for two years

- Unlimited 1.5% cashback on all spend

- Caltex petrol discounts up to 21%

Best Rebate Card for Affluent Advance Customers: HSBC Advance Card

- Pros

- Great fit for budgets between S$2,000 and S$8,000/month

- Easy, low-maintenance cashback

- Cons

- Lacks travel perks

- Doesn't fit highly specialised spend behaviors

Here is why HSBC Advance Card is the best rebate credit card in Singapore for affluent HSBC advance customers.

HSBC Advance Card is one of the best flat rebate cards on the market for higher spenders with no minimum spend requirements. With a recent update to the HSBC Advance Credit Card cashback programme, all customers regardless of whether they have an HSBC Advance banking relationship or not can earn the same cashback for their spend. Base cashback is at 1.5% for S$2,000 and below, and 2.5% for spend above S$2,000 with cashback capped at S$70 per month.

Customers can also earn an additional 1% bonus cashback when they deposit a minimum of S$2,000 per month in fresh funds and charge five transactions to their HSBC Advance Credit Card monthly. When these qualifying criteria are met, you can earn a total cashback of 3.5% with a monthly cap of S$300, which is S$3,600 savings per year – the highest earning potential for a capped card on the market.

Cardholders in good credit standing can also enjoy HSBC’s 0% Card Instalment Payment Plan, which splits transactions of S$500 and above into instalments across 6, 12, or 24 months–all with no interest and no processing fee. Many cards charge fees up to 5% of the transaction amount, which can add up quickly for larger purchases.

- Annual fee: S$194.40 (first year- waived)

- 2.5% base cashback when you spend above SGD2,000

- 1.5% base cashback with no minimum spend

- 1% bonus cashback on your eligible credit card spending if you are HSBC Everyday Global Account holder and qualified for the HSBC Everyday+. T&Cs apply. SGD deposits are insured by up to S$75K by SDIC

- Receive complimentary access to the ENTERTAINER with HSBC app, with over 1,000 1-for-1 deals on dining, lifestyle and travel worldwide

- Annual fee: S$194.40 (first year- waived)

- 2.5% base cashback when you spend above SGD2,000

- 1.5% base cashback with no minimum spend

- 1% bonus cashback on your eligible credit card spending if you are HSBC Everyday Global Account holder and qualified for the HSBC Everyday+. T&Cs apply. SGD deposits are insured by up to S$75K by SDIC

- Receive complimentary access to the ENTERTAINER with HSBC app, with over 1,000 1-for-1 deals on dining, lifestyle and travel worldwide

Best Travel Cards with 0% Interest Instalment Plans

Some of the best travel cards on the market also offer excellent 0% interest instalment plans. We’ve identified our top picks below.

No-Fee Miles Card with Affordable Perks: DBS Altitude Visa Card

- Pros

- Great for online travel bookings

- Cons

- Those willing to pay an annual fee for more bonus miles

- Affluent travellers who are willing to pay a high fee for luxury travel perks

Here is why DBS Altitude Visa Card is the best No-Fee Miles credit card in Singapore with affordable perks.

DBS Altitude Visa Card offers travellers respectable miles rates and affordable perks, paired with a potential fee-waiver. Cardholders earn a 1.2 miles per S$1 locally, 2 miles overseas, and 3 miles for online travel booking; miles earned never expire. Consumers also receive free travel insurance, 2 lounge visits/year, golfing privileges & more. While most travel cards with similar benefits have S$250+ fees, DBS Altitude Card is just S$192.6/year, and this fee can be waived completely with S$25,000 annual spend.

DBS Altitude Card is not only affordable in terms of card fees, it’s also offers a great 0% interest instalments through My Preferred Payment Plan. Transactions as little as S$100 can be split across up to 12 months with no processing fee. While purchases on the plan do not earn rewards, the waived processing fee is an even better benefit–many plans charge up to 5% of the transaction amount, which eclipses value earned by rebates anyways. Ultimately, DBS Altitude Card is a great, affordable travel card that allows consumers to make large purchases fee and stress free.

- Annual fee: S$194.40

- Alternative: pay the annual fee and receive 10,000 bonus miles or charge min S$25,000/year and receive annual fee waiver

- 1.2 miles per S$1 locally, 2 miles overseas

- 3 miles per S$1 spend on online flights and hotel transactions

- 6 miles per S$! spend on flight and hotel transactions at Expedia

- 10 miles per S$1 spend on hotel transactions at Kaligo

- Miles earned never expire

- 2x lounge visits

- DBS My Preferred Payment Plan (0% interest instalments)

- Annual fee: S$194.40

- Alternative: pay the annual fee and receive 10,000 bonus miles or charge min S$25,000/year and receive annual fee waiver

- 1.2 miles per S$1 locally, 2 miles overseas

- 3 miles per S$1 spend on online flights and hotel transactions

- 6 miles per S$! spend on flight and hotel transactions at Expedia

- 10 miles per S$1 spend on hotel transactions at Kaligo

- Miles earned never expire

- 2x lounge visits

- DBS My Preferred Payment Plan (0% interest instalments)

Best Unlimited Cashback for Affluent Golfers & Travellers: CIMB Visa Infinite Card

- Pros

- Best fit for monthly budgets above S$2,000

- Unlimited 2% cashback on travel, overseas and online

- No annual fee credit card

- Cons

- Not suitable for spenders with local budgets

- Doesn't fit specialised budgets (ie dining, shopping) and infrequent travellers

Here is why CIMB Visa Infinite Card is the best unlimited cashback credit card in Singapore for affluent golfers and travellers.

CIMB Visa Infinite Card is the best cashback card for affluent travellers because it offers unlimited earning potential as well as top-notch travel perks. Cardholders earn 1% unlimited cashback on general spend (no minimum requirement) and 2% on travel & overseas transactions (after S$2,000 spend). Perks include free travel insurance, lounge access and discounted limo transfers, which are usually offered by travel cards, rarely by cashback cards.

Another benefit of CIMB Visa Infinite Card is that larger purchases split into instalments can still earn 1% cashback, through the 0% i.Pay Plan. Transactions of $500+ can be split across 6 or 12 months (S$1,000+ for 24 months), for a processing fee of 3% (5% for 24 months). Few cards reward purchases made on a plan, and even fewer offer rebates as high as 1%. And, because CIMB Visa Infinite Card has no annual fee, cardholders can earn on all of their spend maintenance-free. If you’re a high-spending traveller looking for cashback, even on split purchases, CIMB Visa Infinite Card is the best option for you.

- Annual fee: free for life

- Unlimited 2% cashback on all travel and overseas spend

- Unlimited 2% cashback on online spend in foreign currencies

- Unlimited 1% cashback on all other spend

- Free travel insurance, 3 complimentary access to airport lounges

- Visa Infinite Concierge

- CIMB 0% Interest i.Pay Instalment Plan

- Annual fee: free for life

- Unlimited 2% cashback on all travel and overseas spend

- Unlimited 2% cashback on online spend in foreign currencies

- Unlimited 1% cashback on all other spend

- Free travel insurance, 3 complimentary access to airport lounges

- Visa Infinite Concierge

- CIMB 0% Interest i.Pay Instalment Plan

Cashback for Small Dining & Overseas Budgets: Standard Chartered Rewards+ Card

- Pros

- People with S$250-350/month dining & overseas budget

- Supplementary card for lower spend areas

- Cons

- People seeking to maximise rewards for everyday spend

- Those with cards that already reward dining & overseas

- People who spend S$350+/month on dining alone

Here is why Standard Chartered Rewards+ Card is the best unlimited cashback credit card in Singapore for small dining & overseas budgets.

If you’re looking for a supplemental card that maximises a smaller overseas & dining budget, Standard Chartered Rewards+ Card is likely the best option. Consumers spending S$250–S$350/month in these categories can earn higher rewards rates without worrying about a minimum spend requirement. While other cards would only offer 0.3% cashback at this spend level, SC Rewards+ Card offers consumers 2.9 miles per S$1 overseas and 1.45 miles on dining (approx. 2.9% and 1.45% cashback). Earnings are capped at a low 8,000 miles/year (about S$80 value), so higher spenders may be better off with alternative cards. However, access to the EasyPay 0% instalment plan may be of added interest; transactions of S$500+ can be split across up to 12 months for a 5% processing fee, and purchases are still eligible to earn rebates.

- Annual fee: S$192.60 (first 2 years - waived)

- 10 pts (2.9 mi) per S$1 overseas, 5 pts (1.45 mi) on dining, 1 pt (0.29 mi) on general spend

- Free travel insurance

- Up to 16% fuel savings with Caltex

- Annual fee: S$192.60 (first 2 years - waived)

- 10 pts (2.9 mi) per S$1 overseas, 5 pts (1.45 mi) on dining, 1 pt (0.29 mi) on general spend

- Free travel insurance

- Up to 16% fuel savings with Caltex

Best Health & Transport Card with 0% Interest Instalment Plan: CIMB Platinum MasterCard

- Pros

- Awards cashback for global transport

- Cashback for medical expenses and travel spend in foreign currency

- No annual fee credit card

- Cons

- Doesn't award cashback on everyday essentials

- No cashback on online spend

Here is why CIMB Platinum MasterCard is the best 0% Interest Instalment Plan credit card in Singapore for health & transport.

No card offers a higher rewards rate for health, transport and dining spend than CIMB Platinum MasterCard. Cardholders earn 10% cashback on medical spend ranging from doctors visits to personal care facilities & beyond–few other cards, in comparison, reward health spend at all. In addition, cardholders earn 10% cashback on transport & petrol, global dining, travel spend in foreign currency, and transactions with select electronics/furnishings vendors, which is quite a broad range. Earnings can reach up to S$20/category, adding to a potential S$100/month.

Cardholders also have access to the CIMB 0% i.Pay Plan, which splits transactions of S$500+ across 6 or 12 months (S$1,000+ for 24 months). There’s a 3% processing fee (5% for 24 months), but purchases on the plan earn cashback. While the rebate for such transactions is just 0.2%, few plans reward such transactions at all. CIMB Platinum MasterCard is also free forever, making shopping just a bit more stress-free. Ultimately, CIMB Platinum MasterCard is an excellent option if you want to earn on all of your spend, even for transactions split into instalments.

- Annual fee: free for life

- 10% cashback on dining, medical, transport, petrol & overseas travel

- 10% cashback on select electronics/furnishings vendors

- Unlimited 0.2% cashback on all other spend

- CIMB 0% Interest i.Pay Instalment Plan

- Annual fee: free for life

- 10% cashback on dining, medical, transport, petrol & overseas travel

- 10% cashback on select electronics/furnishings vendors

- Unlimited 0.2% cashback on all other spend

- CIMB 0% Interest i.Pay Instalment Plan

Best Card for Affluent Social Spenders with 0% Interest Instalment Plan: CIMB World MasterCard

- Pros

- Great fit for big leisure budgets

- Rewards dining, entertainment and duty free shopping

- Perks for avid golfers

- No-fee & maintenance free cashback card

- Cons

- Lack cashback on essentials (ie groceries, bills)

- Doesn't reward airline & hotel spend

- Doesn't fit monthly budgets of S$3,000/month and below

Here is why CIMB World MasterCard is the best 0% Interest Instalment Plan credit card in Singapore for affluent social spenders.

CIMB World MasterCard offers some of the highest unlimited rebate rates on the market. Cardholders earn 1% unlimited cashback on general spend, which is slightly lower than competitors, but enjoy a boost to 2% cashback on wine & dine (including food deliveries), movies & digital entertainment, taxi & automobile and luxury goods with a minimum monthly spending of S$1,000. These unlimited rewards for leisure pair well with CIMB World Card’s benefits and privileges. Cardholders enjoy free airport lounge access and 50% off green fees at fairways across Asia. And, beyond it all, CIMB World Card is free forever, making the card truly maintenance-free.

Cardholders may also be interested in the CIMB 0% i.Pay Plan. Transactions of S$500+ can be split across 6 or 12 months (S$1,000+ for 24 months), for a 3% processing fee (5% for 24 months). Despite the fee, cardholders earn 1% cashback on purchases made on the plan. Most cards exclude such purchases or offer far lower rebate rates. Overall, CIMB World MasterCard is the best no-fee cashback option for golfers and affluent leisure-spenders, and also offers cardholders a way to earn on even their split purchases.

- Annual fee: free for life

- Unlimited 2% cashback on wine & dine, food delivery, entertainment, taxi & automobile, and luxury goods with min. spend of $1,000 monthly

- Unlimited 1% cashback on all other spend

- 50% off green fees at select fairways in Asia

- Free access to MasterCard Airport Experiences

- CIMB 0% Interest i.Pay Instalment Plan

- Annual fee: free for life

- Unlimited 2% cashback on wine & dine, food delivery, entertainment, taxi & automobile, and luxury goods with min. spend of $1,000 monthly

- Unlimited 1% cashback on all other spend

- 50% off green fees at select fairways in Asia

- Free access to MasterCard Airport Experiences

- CIMB 0% Interest i.Pay Instalment Plan

Summary of Best Credit Cards with 0% Interest Instalment Plans for 2024

Below, we've prepared a summary of our picks for the best credit cards with 0% Interest Instalment Plans for 2024.

| Card | Best for... | Annual Fee | |

|---|---|---|---|

| OCBC Cashflo | Automatic Payment Split | S$160.5 (waiver) | |

| DBS Woman's World | Miles for Online Shopping | S$192.6 (waiver) | |

| POSB Everyday | Rebates on Essentials | S$192.6 | |

| HSBC Advance | Affluent Advance Customers | S$192.6 (waiver) | |

| SC Rewards+ | Overseas & Dining | S$192.6 |

| Card | Best for... | Annual Fee | |

|---|---|---|---|

| OCBC Cashflo | Automatic Payment Split | S$160.5 (waiver) | |

| DBS Woman's World | Miles for Online Shopping | S$192.6 (waiver) | |

| POSB Everyday | Rebates on Essentials | S$192.6 | |

| HSBC Advance | Affluent Advance Customers | S$192.6 (waiver) | |

| SC Rewards+ | Overseas & Dining | S$192.6 |

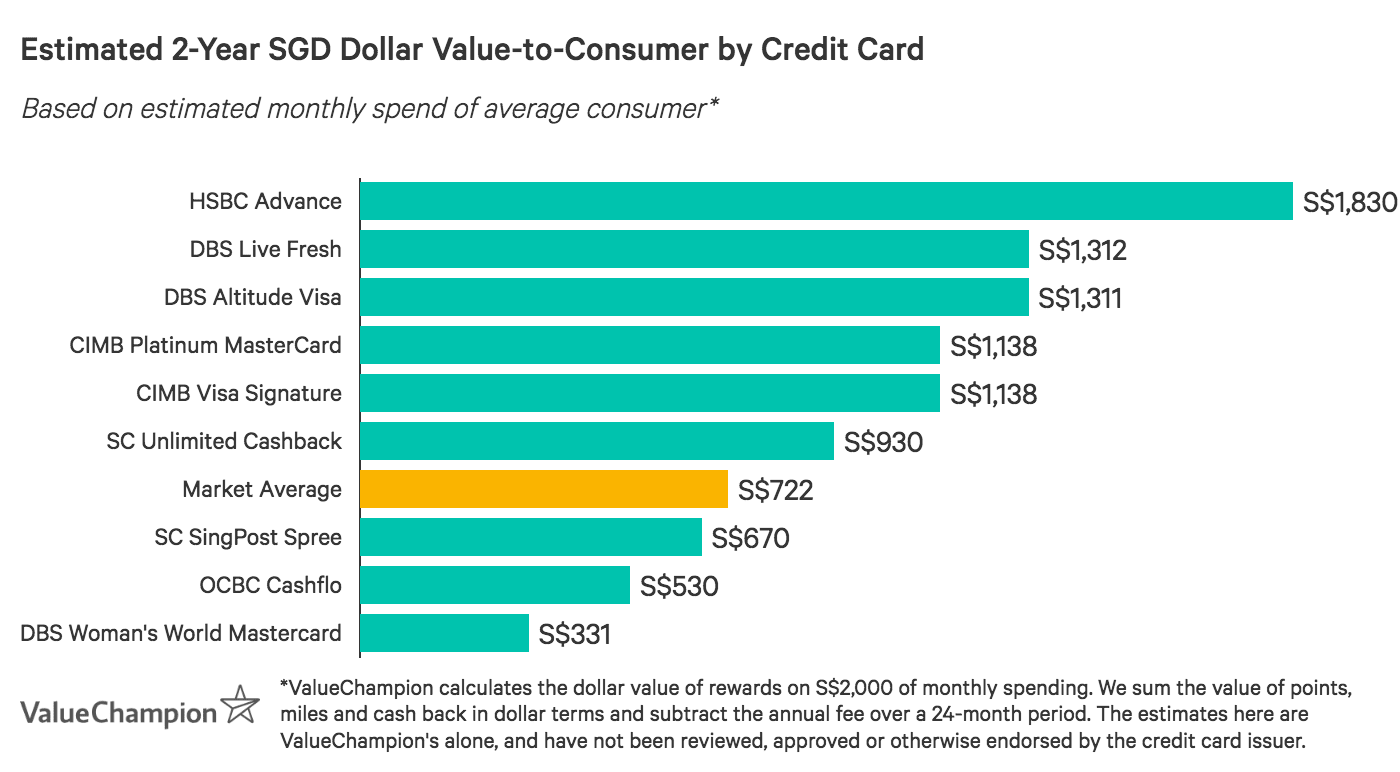

Compare the Best 0% Instalment Credit Cards by Dollar Value

Below is a visual representation of the approximate savings one can earn by using the best credit cards for 0% interest instalment plans in Singapore. These dollar values* represent the approximate amount of rewards a person can earn in cash rebate & air miles when spending S$2,000 per month for 2 years. However, this amount can vary widely depending on what your spending habit looks like and how you redeem your miles.

Footnotes

*ValueChampion calculates the dollar value of rewards based on S$2,000 of monthly spending. We sum the value of points, miles and cashback in dollar terms and subtract the annual fee over a 24-month period. The estimates here are ValueChampion's alone, and have not been reviewed, approved or otherwise endorsed by the credit card issuer.

Read More:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.