Best Standard Chartered Credit Cards 2024

Every card is different, and every person wants different credit card. When you combine this with the fact that there are hundreds of credit cards available, it becomes clear that shopping for a credit card in Singapore is extremely difficult. To help you navigate this complex process, our credit card experts handpicked and featured a few cards from Standard Chartered that we regard highly below.

- SC Smart Card: 6% Cashback on Eligible Purchases

- SC Simply Cash: 1.5% unlimited rebate + transport perks

- SC Visa Infinite X: Bonus S$6,000 w/ S$200k fund placement

- SC Rewards+: 2.9 miles per S$1 overseas, 1.45 for dining

- SC Visa Infinite: 3 miles per S$1 overseas, rewards for tax-pay

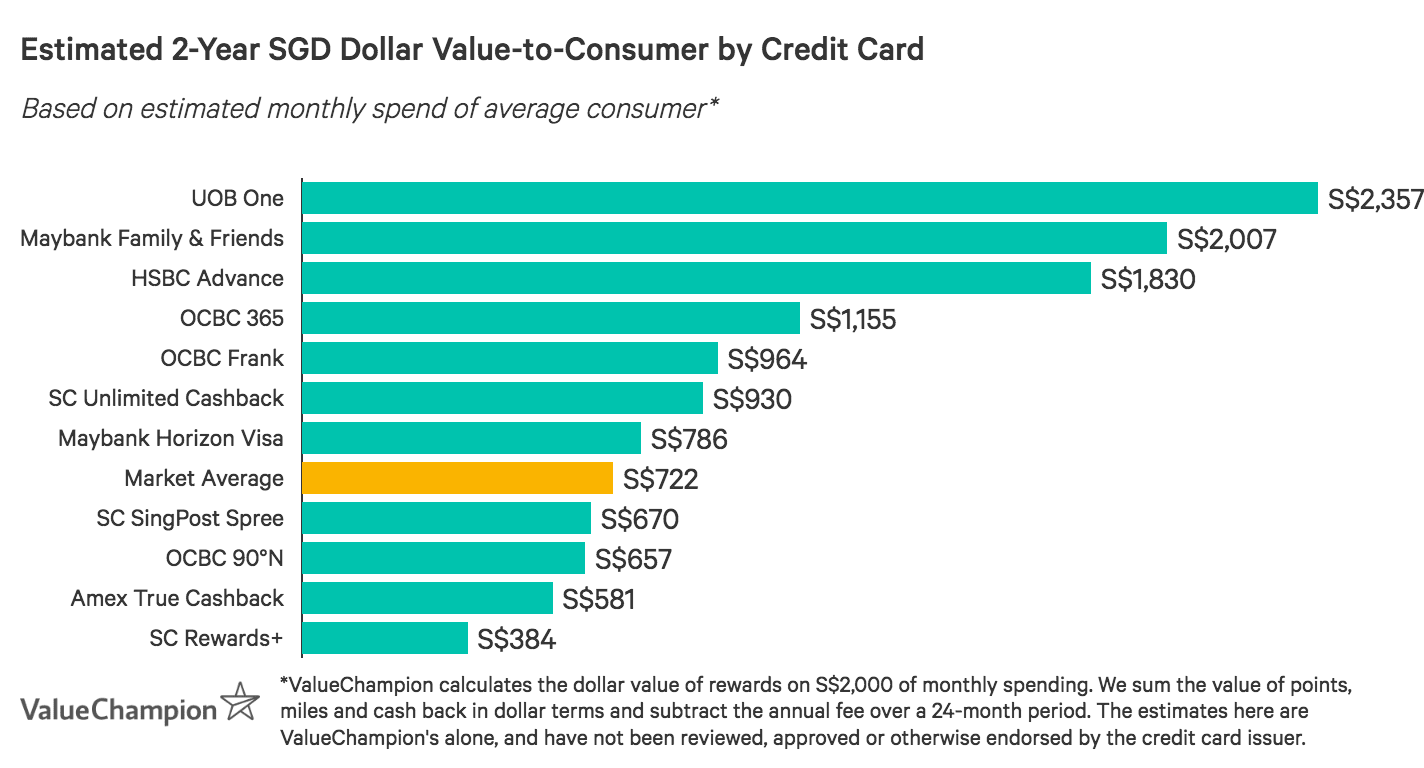

Compare Best Standard Chartered Credit Cards by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best Standard Chartered credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

- 6% Cashback on Eligible Purchases

- 1.5% unlimited rebate + transport perks

- Bonus S$6,000 w/ S$200k fund placement

- 2.9 miles per S$1 overseas, 1.45 for dining

- 3 miles per S$1 overseas, rewards for tax-pay

Compare Best Standard Chartered Credit Cards by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best Standard Chartered credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Standard Chartered Smart Credit Card: 6% Cashback On Qualifying Transactions With No Minimum Spend

| |

If you want to want to maximise rewards from your everyday-lifestyle purchases, consider Standard Chartered Smart Card. Standard Chartered Smart Credit Card offers an attractive 6% cashback on qualifying transactions with no minimum spend required. Moreover, you can divide your payments into three interest-free instalments with EasyPay. With no annual fees and cash advance fees, the Standard Chartered Smart Credit Card does seem appealing. However, the cashback is only applicable to limited transactions, such as fast food, digital streaming subscriptions, breakfast joints and public transport. Overall, the SC Smart Credit card is a good option for those who want to maximise rewards from their everyday-lifestyle purchases.

| |

|

|

If you want to want to maximise rewards from your everyday-lifestyle purchases, consider Standard Chartered Smart Card. Standard Chartered Smart Credit Card offers an attractive 6% cashback on qualifying transactions with no minimum spend required. Moreover, you can divide your payments into three interest-free instalments with EasyPay. With no annual fees and cash advance fees, the Standard Chartered Smart Credit Card does seem appealing. However, the cashback is only applicable to limited transactions, such as fast food, digital streaming subscriptions, breakfast joints and public transport. Overall, the SC Smart Credit card is a good option for those who want to maximise rewards from their everyday-lifestyle purchases.

|

Standard Chartered Simply Cash Credit Card: Uncapped Cashback + SimplyGo

| |

If you’re a high spender and typically feel constrained by earnings caps, consider Standard Chartered Simply Cash Credit Card. Cardholders earn 1.5% unlimited cashback on all spend, with no limitations on rewards earned. While other credit cards offer this same rate, few offer the travel perks provided by SC Unlimited Cashback Card. Not only is it SimplyGo functional, it also offers fuel savings up to 21% with Caltex. While there’s a S$194.40 fee, it’s waived 2 years. Overall, if you want unrestricted rewards paired with top-notch transport perks, SC Simply Cash Credit Card may be the perfect choice for you.

| |

|

|

If you’re a high spender and typically feel constrained by earnings caps, consider Standard Chartered Simply Cash Credit Card. Cardholders earn 1.5% unlimited cashback on all spend, with no limitations on rewards earned. While other credit cards offer this same rate, few offer the travel perks provided by SC Unlimited Cashback Card. Not only is it SimplyGo functional, it also offers fuel savings up to 21% with Caltex. While there’s a S$194.40 fee, it’s waived 2 years. Overall, if you want unrestricted rewards paired with top-notch transport perks, SC Simply Cash Credit Card may be the perfect choice for you.

|

Standard Chartered Visa Infinite X: Biggest Sign Up Bonus

| |

Standard Chartered Visa Infinite X Card provides the absolute best sign-on bonus for wealthy consumers. Those who can place S$300k fresh funds in Standard Chartered's Priority Banking account and maintain this amount for 3 months can receive an incredible 100,000 KrisFlyer miles as a welcome bonus. This is worth approximately S$10k if redeemed for business or first class tickets. This bonus increases even further for those who can place up to $1.5mn to a total of 300,000 miles (worth S$30k). Though SC Vi X Card's S$702 non-waviable fee is quite expensive, these bonuses far exceed any other offering on the market and is well worth it for those who can afford it.

| |

|

|

Standard Chartered Visa Infinite X Card provides the absolute best sign-on bonus for wealthy consumers. Those who can place S$300k fresh funds in Standard Chartered's Priority Banking account and maintain this amount for 3 months can receive an incredible 100,000 KrisFlyer miles as a welcome bonus. This is worth approximately S$10k if redeemed for business or first class tickets. This bonus increases even further for those who can place up to $1.5mn to a total of 300,000 miles (worth S$30k). Though SC Vi X Card's S$702 non-waviable fee is quite expensive, these bonuses far exceed any other offering on the market and is well worth it for those who can afford it.

|

Standard Chartered Rewards+: Miles for Overseas & Dining

| |

If you currently have a specialised card–like a shopper credit card – you may be earning just a base rate of 0.3% rebate for all of your dining spend. If this is the case, you can easily multiply your earnings by adding Standard Chartered Rewards+ Card as a supplementary credit card. Cardholders earn 2.9 miles per S$1 for overseas spend and 1.45 miles on dining (equal to about 2.9% and 1.45% rebate, respectively) with no minimum spend requirement. This is much higher than a base cashback rate, and also higher than typical travel credit card rates. In fact, most travel cards offer just 2–2.4 miles per S$1 overseas and 1.1–1.4 miles locally.

| |

|

|

If you currently have a specialised card–like a shopper credit card – you may be earning just a base rate of 0.3% rebate for all of your dining spend. If this is the case, you can easily multiply your earnings by adding Standard Chartered Rewards+ Card as a supplementary credit card. Cardholders earn 2.9 miles per S$1 for overseas spend and 1.45 miles on dining (equal to about 2.9% and 1.45% rebate, respectively) with no minimum spend requirement. This is much higher than a base cashback rate, and also higher than typical travel credit card rates. In fact, most travel cards offer just 2–2.4 miles per S$1 overseas and 1.1–1.4 miles locally.

|

Standard Chartered Visa Infinite: Miles for Tax-Pay

| |

Standard Chartered Visa Infinite Card is by far one of the best credit travel cards on the market. To begin with, it offers the highest rewards rates on the market–1.4 miles per S$1 locally, and an astounding 3 miles per S$1 overseas. For context, most credit travel cards offer 2–2.4 miles per S$1 overseas. Even further, cardholders enjoy 35,000 welcome miles (worth S$350) and earn rewards for banking activities, like paying taxes. Most credit cards exclude such transactions from earning rewards.

| |

|

|

Standard Chartered Visa Infinite Card is by far one of the best travel credit cards on the market. To begin with, it offers the highest rewards rates on the market–1.4 miles per S$1 locally, and an astounding 3 miles per S$1 overseas. For context, most travel credit credit cards offer 2–2.4 miles per S$1 overseas. Even further, cardholders enjoy 35,000 welcome miles (worth S$350) and earn rewards for banking activities, like paying taxes. Most credit cards exclude such transactions from earning rewards.

|

Learn More About Maximising Your Rewards with Standard Chartered

SC Simply Cash Credit Card v. Amex True Cashback Card

|

|

| American Express True Cashback Card is a great option for high spenders because of its unlimited earning potential. Cardholders earn 1.5% flat cashback on all spend. This is the same rate as offered by SC Simply Cash Credit Card. For Amex True Cashback Cardholders, however, this rate is doubled to 3% for the first 6 months (up to S$150). This makes it a great credit card for those with large, immediate expenses–such as planning a wedding or paying large hospital bills.

| |

SC Simply Cash Credit Card v. Maybank FC Barcelona Card

| |

| Maybank FC Barcelona Visa Signature Card offers the highest unlimited local rate on the market, at 1.6% (v. 1–1.5%). It’s an excellent match for high-spenders who primarily spend at home, rather than abroad. In fact, overseas spend earns just 0.8 miles per S$1 (equal to about 0.8% rebate), which isn’t very competitive. However, Maybank FC Barcelona Card does come with a fee-waiver; most of its competitors do not. Ultimately, if you spend quite a bit both locally and overseas, you’re likely to earn more with SC Simply Cash Credit Card. If you’re mostly a local spender, however, Maybank FC Barcelona may be a great fit for you. | |

SC Visa Infinite X Card v. Citi Prestige Card

|

|

| Citi Prestige Card offers some of the best luxury travel perks on the market–in addition to great miles rewards rates. Cardholders earn 1.3 miles per S$1 locally and 2 miles overseas, with 25,000 annual renewal miles (worth S$250) and an up to 30% annual bonus based on length of relationship with Citibank. Additionally, they receive unlimited lounge access, access to JetQuay, airport limo transfers, golfing privileges, bonus 4th hotel nights & much more.

| |

SC Visa Infinite X Card v. OCBC Voyage Card

|

|

| OCBC Voyage Card is one of the most flexible travel cards on the market. Cardholders earn 2.3 miles per S$1 overseas, 1.2 miles locally, and a boosted 1.6 miles for local dining. This makes it easy to earn rewards no matter where you are–travelling, or spending an extended period of time at home. In addition, miles can be redeemed with no black-out dates, no transfer fees, and minimal processing time.

| |

| SC Simply Cash Credit Card v. Amex True Cashback |

|---|

|

|

| American Express True Cashback Card is a great option for high spenders because of its unlimited earning potential. Cardholders earn 1.5% flat cashback on all spend. This is the same rate as offered by SC Simply Cash Credit Card. For Amex True Cashback Cardholders, however, this rate is doubled to 3% for the first 6 months (up to S$150). This makes it a great credit card for those with large, immediate expenses–such as planning a wedding or paying large hospital bills.

|

| SC Simply Cash Credit Card v. Maybank FC Barcelona | |

|---|---|

| Maybank FC Barcelona Visa Signature Card offers the highest unlimited local rate on the market, at 1.6% (v. 1–1.5%). It’s an excellent match for high-spenders who primarily spend at home, rather than abroad. In fact, overseas spend earns just 0.8 miles per S$1 (equal to about 0.8% rebate), which isn’t very competitive. However, Maybank FC Barcelona Card does come with a fee-waiver; most of its competitors do not. Ultimately, if you spend quite a bit both locally and overseas, you’re likely to earn more with SC Simply Cash Credit Card. If you’re mostly a local spender, however, Maybank FC Barcelona may be a great fit for you. | |

| SC Visa Infinite X v. Citi Prestige | |

|---|---|

|

| |

| Citi Prestige Card offers some of the best luxury travel perks on the market–in addition to great miles rewards rates. Cardholders earn 1.3 miles per S$1 locally and 2 miles overseas, with 25,000 annual renewal miles (worth S$250) and an up to 30% annual bonus based on length of relationship with Citibank. Additionally, they receive unlimited lounge access, access to JetQuay, airport limo transfers, golfing privileges, bonus 4th hotel nights & much more.

| |

| SC Visa Infinite X Card v. OCBC Voyage | |

|---|---|

|

| |

| OCBC Voyage Card is one of the most flexible travel credit cards on the market. Cardholders earn 2.3 miles per S$1 overseas, 1.2 miles locally, and a boosted 1.6 miles for local dining. This makes it easy to earn rewards no matter where you are–travelling, or spending an extended period of time at home. In addition, miles can be redeemed with no black-out dates, no transfer fees, and minimal processing time.

| |

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.