UOB EVOL Card: Cashback for Young Adults

ValueChampion Rating ![]()

Pros

- Easy to use cashback card

- Great for budgets of at least S$600/month

- Rewards all online and mobile spend

Cons

- Cashback capped at S$60/mo

Update: UOB has replaced the YOLO Card with the new EVOL Card. Existing YOLO cardmembers will be transitioned to EVOL Cards as of June 17, 2021.

UOB EVOL, formerly known as UOB YOLO Card, is in many ways the new and improved version of its predecessor. Cardholders can now earn 8% rebate on all mobile and contactless spend on weekdays and weekends alike, which includes dining, shopping, travel, entertainment and much more. The minimum required spend remains at S$600 per month, and cashback cap is now S$20 per category, with a total of S$60 per month (S$720/year). UOB EVOL is also Southeast Asia's first bio-sourced card supporting green initiatives and offering a variety of sustainable deals. UOB EVOL Card is a great option if you want to maximise rewards with sustainable spending, making it one of the best cashback credit cards in Singapore for young professionals.

UOB EVOL Credit Card Features and Benefits

|

|---|

Key Features:

|

Our Evaluation: Strong Rewards Tailored to Young Adults

UOB EVOL Card is an excellent cashback card for young adults whose transactions are primarily limited to online and contactless spend. Cardholders earn 8% cashback on online spend which includes dining, entertainment, shopping, fashion, Grab and hotels. Mobile contactless spend which includes Apple Pay, Google Pay, Samsung and Fitbit Pay also earn 8% cashback. All other spend earns 0.3% cashback. One unique feature of this card is that it's the first bio-sourced card in the region, offering over 1,000 sustainable deals on dining and shopping, further boosting your savings.

UOB EVOL Card Rebates Chart

| Spend Category | Rewards Rate |

|---|---|

| Online spend: Dining, Entertainment, Shopping, Grab, Hotels | 8% |

| Mobile contactless spend: Apple Pay, Google Pay, Samsung Pay, FItbit Pay | 8% |

| All other spend | 0.3% |

In order to access these rates, however, cardholders must spend at least S$600 per month. While this spend requirement is quite manageable for the average young adult who spends at least S$600 per month, the cashback cap of S$60 per month is split between online, mobile and other spend. In order to reach these caps, S$250 spend is required on online purchases and S$250 on mobile purchases. In order to earn S$20 with a rate of 0.3%, other spend has to reach S$6,667. It is therefore safe to say that most monthly cashback will be just above S$40.

While the card's annual fees remain at S$192.60, and waived in the first year, annual fees due before June 1, 2022 will enjoy an annual fee waiver with S$12,000 min spend per year. Annual fees due after June 1, 2022 will be waived completely with minimum 3 transactions per statement months for the duration of one year.

How Does UOB EVOL Credit Card Rewards Program Work?

- Every 1 dollar of cashback earned is equal to S$1

- Cashback earned in the current month will be credited to the cardholder's account the following month

- Transactions incurred by the supplementary cardholder are considered in the calculation of qualifying spend

- Cashback can only be used to offset against the billed amount for your card the following month

- Cashback cannot be withdrawn as cash or transferred to any other UOB accounts

- Cashback expires 2 calendar years from the month in which it was earned

- Cashback is automatically forfeited and is non-transferable when an account is closed

What You Should Know: Limits, Minimums and Exclusions

UOB EVOL Card, like many others, has certain limits and exclusions when it comes to its rewards programme. In order to earn 8% cashback, members must spend at least S$600 per month, otherwise cashback rate drops to 0.3%. In addition, each cashback category has its own individual caps of S$20 each, adding up to a maximum monthly cashback of S$60.

| Rebate | Monthly Cap | Spend Required | |

|---|---|---|---|

| Online spend | 8% | S$20 | S$250 |

| Mobile contactless spend | 8% | S$20 | S$250 |

| All other spend | 0.3% | S$20 | S$6,667 |

| Total spend to reach cap | S$7,167 |

Taking into account the minimum spend requirement of S$600, the rewards system allows you to easily earn S$40 each month just by reaching that cap and spending at least S$250 on mobile and S$250 on online spend. Reaching the additional S$20 at 0.3% on other spend, is a bigger challenge, as it requires an additional S$6,667 monthly spend.

How UOB EVOL Credit Card Compare Against Other Cards

Read our comparisons of UOB EVOL Card with other cards and learn what makes each card unique in their own way. We compare and contrast each card to highlight its uniqueness to help you identify the card that you need. In case you would like to compare the rewards value of this or any other card yourself, go to our RealValue Credit Card Rewards Calculator to compare the cards' rewards, promotions, rates and other unique features.

UOB EVOL Card v. UOB One Card

- Pros

- Good fit for budgets of at least S$2,000 per month

- Easy cashback on daily spend

- Gives rebates for paying bills

- Cons

- Doesn't fit inconsistent budgets

- Annual fee

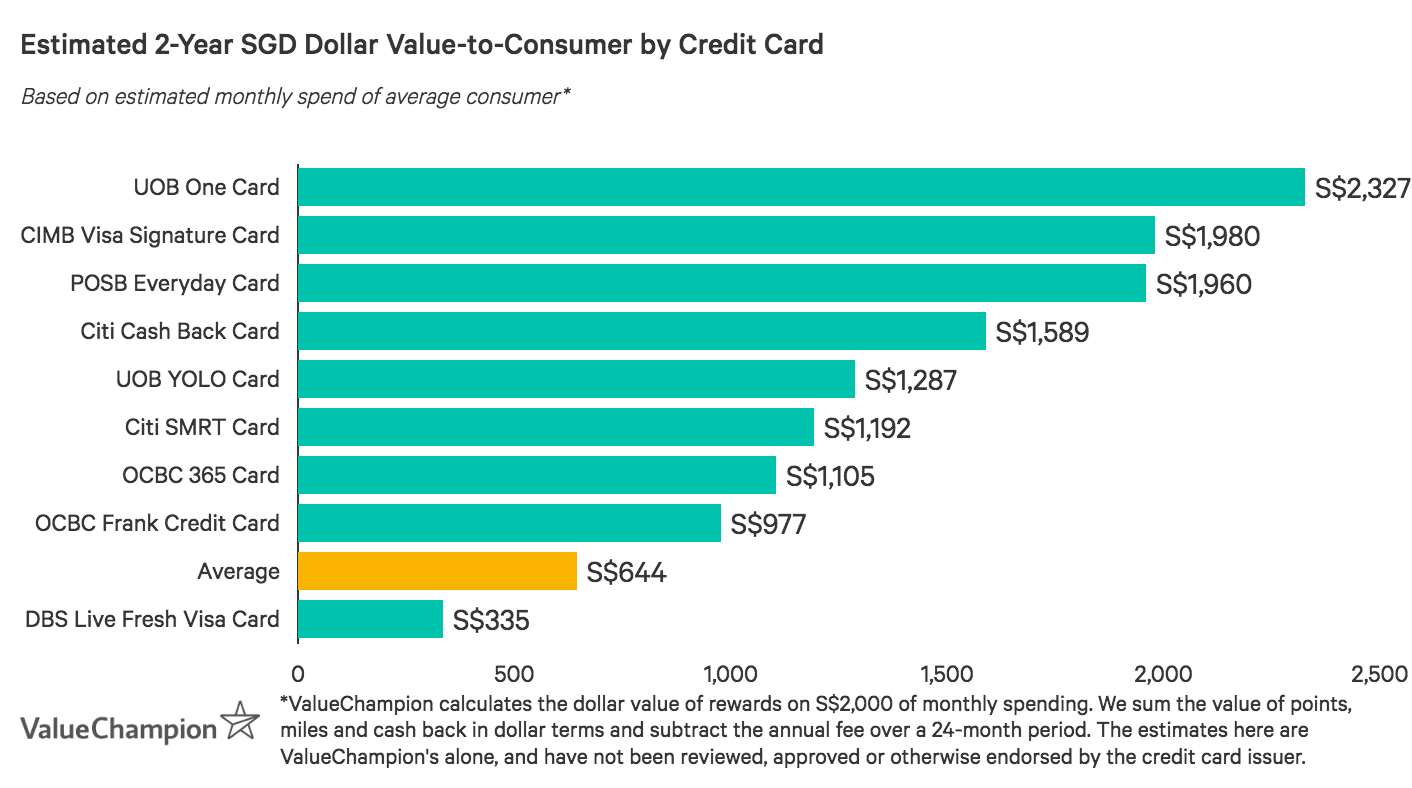

Consumers who consistently spend at least S$2,000 month can maximise cashback with UOB One Card. Cardholders earn cashback based on tiers of monthly spend, with S$2,000/month for 3 consecutive months earning S$300 quarterly cashback–averaging to S$100/month, compared to S$60 for UOB EVOL Card. The card is also flexible, with nearly all spend counting towards reaching a rebate tier.

Despite this simplicity, spending even a dollar below S$2,000 drops cardholders' rewards potential to S$33/month (with spend below S$1,000 earning only S$17/month). Therefore, consumers who spend more than S$600/month but less than S$2,000/month would earn far more in cashback from UOB EVOL Card than with UOB One Card.

UOB EVOL Card v. OCBC Frank Card

- Pros

- 6% rebate on online, mobile contactless, and FX spend

- Fee waiver with S$10,000 annual spend

- Cons

- 0.3% rebate on general purchases

- Annual fee after 2 years

- Capped cashback at S$75

Mid-to-lower spenders looking for no-fee cashback on online shopping and entertainment might be interested in OCBC Frank Card. OCBC Frank Card rewards online and mobile spend as well as foreign currency spend with 6% cashback, capped at S$75/month after a minimum spend of S$600. While qualifying spend is for the two cards is the same, OCBC Frank Card's rewards rates are lower although its monthly caps are higher (S$75 vs S$60) than UOB EVOL Card's. While the two cards cover all the same spend categories, OCBC Frank also rewards foreign currency spend which is convenient for frequent travelers.

OCBC Frank Card's annual fee of S$80 is waived for 2 years, then subsequently with each annual spend of S$10,000–which is reasonable for most consumers. UOB EVOL Card's annual fee of S$192.6 is waived for the first year, and then subsequently waived altogether with 3 monthly transactions, making the card more affordable. OCBC Frank Card may be a better fit for consumers who frequently pay online and travel, whereas UOB EVOL Card is better suited to those who primarily spend in Singapore.

UOB EVOL Card v. OCBC 365 Card

- Pros

- 6% rebate on dining, 3% on groceries, transport, utilities, online travel

- Fee waiver with S$10,000 annual spend

- Up to 22.1% fuel savings at Caltex, 20.2% at Esso

- Cons

- 0.3% rebate on general spend

- High S$800 minimum spend requirement

OCBC 365 Card is a well-rounded cashback card for consumers seeking no-fee rewards on essentials (like utility bills) and leisure (like online travel bookings). Like UOB EVOL Card, OCBC 365 Card rewards dining and online food delivery (6%), private hire rides (3%), and online travel bookings (3%)–though at lower rates. It stands apart, however, by rewarding essentials like groceries (3%), petrol (up to 23%), and recurring bills (3%).

While OCBC 365 cardholders can avoid paying the S$192.6 fee with each annual spend of S$10,000, UOB EVOL waives the fee with min 3 transactions per month. OCBC 365 Card may not reward a social lifestyle as much as UOB EVOL Card, but it offers cashback for essentials missing from UOB EVOL Card's offerings. Young families or average spenders looking for a balanced card might consider OCBC 365 Card.

UOB EVOL Card v. Citi SMRT Card

- Pros

- Good rewards rates for modest budgets

- SMRT$ rewards on EZ-Reload transactions

- Cons

- Not suitable for higher budgets

- Lacks travel and overseas rewards

Citi SMRT Card is a great card for young professionals seeking convenience and cashback on their commute. Both Citi SMRT Card and UOB EVOL Card appeal to average-to-lower-spenders and provide cashback tailored to younger lifestyles. For example, Citi SMRT Card has no minimum spend requirement and offers 5% cashback on coffee, fast food, and cineplex transactions, and 3% cashback for online shopping.

Citi SMRT Card, however, appeals more to young professionals than to social individuals committed to leading a sustainable lifestyle. Cardholders enjoy all-in-one functionality and 2% cashback on Auto Top-Ups to support their commute, plus up to 14% in petrol discounts. They also earn 5% on groceries and 1% on select recurring bills through One Bill. Citi SMRT Card does not offer any privileges or discounts on eco-friendly spend. Young adults and average-to-lower-spenders who'd like accessible cashback that balances leisure and essentials, rather than spending mostly online and via mobile payments, might consider Citi SMRT Card.

Methodology: How We Review Credit Cards

ValueChampion analyses nearly every credit card available in Singapore. We do this by weighing the value of each card's rewards rates, bonuses, and benefits against the its spending requirements, monthly rewards caps and annual fees.

Most cards earn miles or cashback at different rates depending on the category that your spend falls into. Different spend categories can also have different monthly caps on how much you earn. Finally, some cards require that you spend a certain amount each month in order to activate their full rewards rates.

Applying all of these factors to a typical budget allows us to estimate how much the credit card will earn in rewards. Annually recurring fees and bonuses are also considered in our calculation. We use our results to evaluate how effective the card is compared to other options.

To try our calculations for yourself, use our RealValue Rewards Calculator and find out how easy it is to compare the rewards potential of every credit card in Singapore.

To view the best cashback credit cards available in Singapore, check over here for more!

Read Also:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.