Cashback Cards Are Better Than Miles Cards for Most Singaporeans: ValueChampion Analysis

Singaporeans are some of the most travel-avid people in the world. According to a new Criteo study, Singaporeans took an average of 5.2 trips in the last 12 months. This is more than 4x higher than the average number of leisure trips that people in Asia took as of 2015. And while many of these consumers are paying for their trips with credit cards, air miles credit cards aren’t always the best option for most people. In fact, most consumers would get more value by using a cash-back card instead.

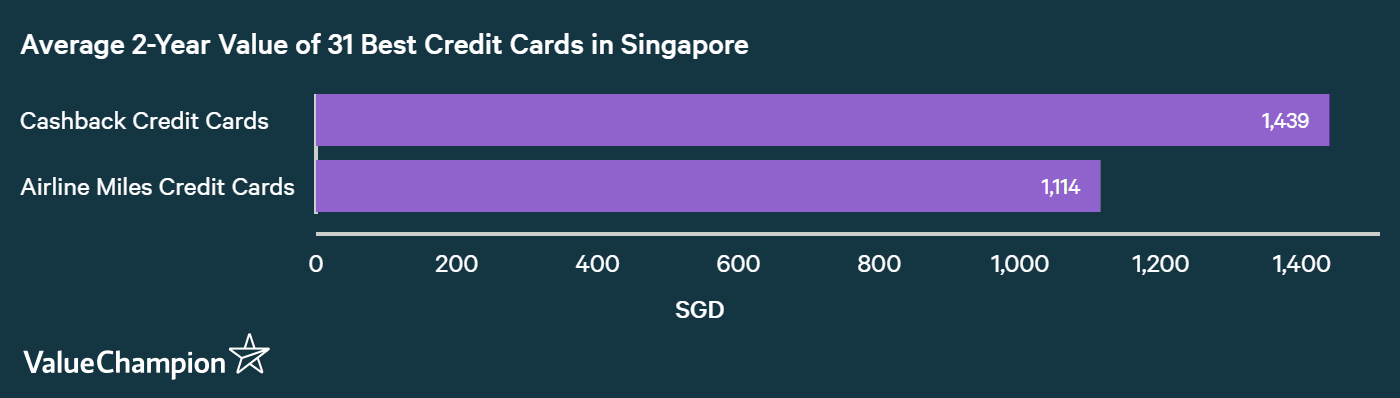

ValueChampion calculated the rewards values of 31 popular travel and cash-back credit cards assuming an average consumer spending. Here’s what our analysis found:

- For an average Singaporean spending around S$2,000 on their credit card per month, the best cashback credit cards in Singapore yield 30% more in rewards than the best miles credit cards.

- For an air miles credit card to be better than cash back card, a consumer has to do either of the following two things:

- Spend more than S$8,000 per year on his travel needs

- Or redeem miles for business class tickets or long-haul tickets only.

Air miles credit cards are not always the best option for travelers

Singaporean travelers who spend less than S$8,000 per year on travel expenses would earn higher overall rewards with a cash-back card than a miles credit card. Since an average household spends about S$2,000 per year on travelling (according to the household expenditure conducted by the Singporean government), it would mean that this rule is generally true for most people in Singapore.

To get to this conclusion, we calculated how much a person can earn in cash back and miles (or points converted into miles) minus fees if he were to spend S$2,000 per month for 2 years for 31 of the best credit cards in the market. Of this, S$150 was geared towards travel bookings and overseas spending, translating to about S$1,800 of annual travel spending. The result was quite interesting: the best cashback credit cards yielded about 30% more value than the best air miles credit cards in Singapore.

This is because travel spending only represents about 3% of an average household's expenditures, compared to 16% for dining, 9% for groceries, or 17% for transportation. Since cashback credit cards reward higher rates for these categories than miles credit cards do, cash rebate cards generally end up being more rewarding for an average consumer.

For instance, consider UOB One Card or POSB Everyday Card, easily two of the best cashback cards in the market. Since these two cards provide rebates ranging from 3% to 13% on different categories of spending, they tend to do better for most consumers than some of the best miles credit cards like Citi PremierMiles card or DBS Altitude Card, which provide roughly 1.2 miles per S$1 of spending (1.2% yield assuming redemption value of S$0.01 per mile), especially for people who don't travel a lot.

But miles credit cards have their own advantages

Of course, there’s more to credit cards than rewards. Consumers should consider whether they use other benefits often offered by miles credit cards but not by most cash rebate cards. For example, those who like to purchase travel insurance, which can easily cost S$20 or more, for their trips could save a lot of money by getting a card with a complimentary travel insurance. Some may also care greatly about getting complimentary lounge access, which can help you save S$40-S$50 per visit. If you take 2 trips per year and enjoy these benefits for free each time, you could be easily saving S$500 that you would've needed to spend to enjoy them otherwise.

Also, frequent travellers could do very well with an air miles card, especially if they spend a lot of travel needs. A study conducted by Visa found that the average traveling household in Singapore spends about S$20,000 on travel per year. While this average is likely quite skewed, it does reflect how there are some Singaporeans who do spend heavily on travelling: the average annual spend on overseas travel per Sinpogrean household is almost 6x higer than the Asia Pacific household average. For these people, an air miles card can definitely be more valuable than a cash back card.

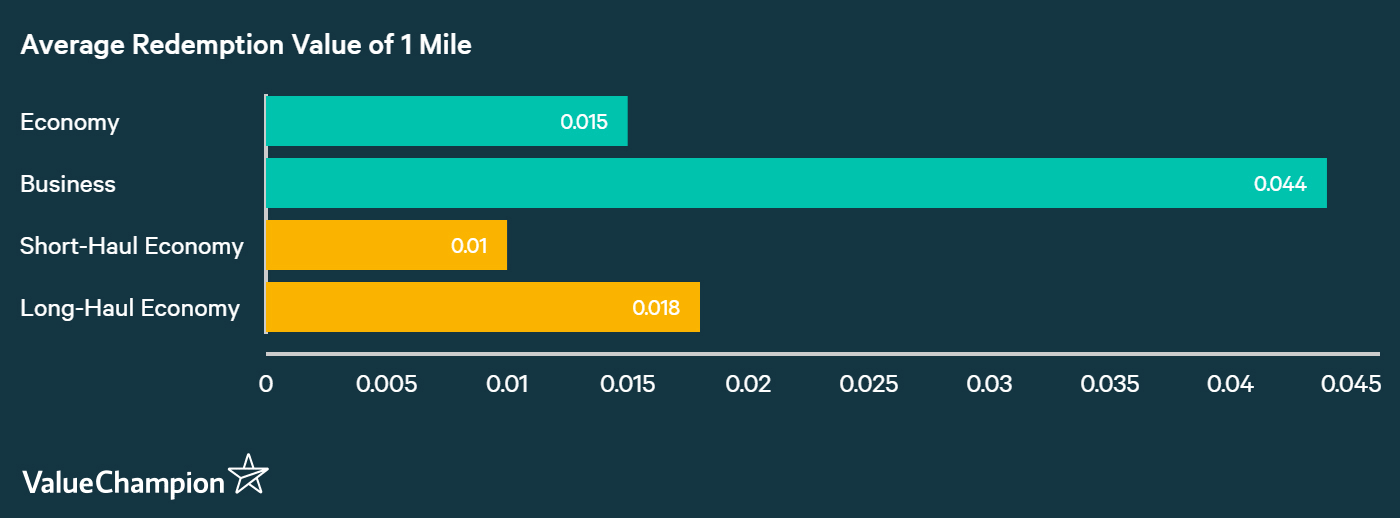

This is especially the case if they travel frequently on business class or on long haul flights. While ValueChampion's study generally assumes the value of 1 Krisflyer mile at S$0.01, we also found that a mile can be worth 2-4x higher if you redeem it for long haul flights or for business class tickets, which could increase the value of an air miles card significantly higher compared to that of a cashback card.

Conclusion

Most Singaporeans should opt for cash-back rewards, but there are always exceptions. If you spend more than S$8,000 on travel per year, if you use travel benefits like free lounge access or travel insurance, an air miles credit card can be way more valuable than a cash rebate card. Otherwise, cash back will result in higher rewards rates that are also more flexible — rewards that can be used for anything, including travel. You can read more about how cash back and miles compare in our guide at the link.

Methodology

To calculate how much one can earn in terms of cash back or miles by using a particular credit card, we assumed a monthly spending of S$2,000 of an average consumer, spread out across expenditure categories like travel, dining and groceries. Then to calculate the value of a Krisflyer mile, we collected real air fares of economy and business class tickets from Singapore to 13 other regions across the world. By comparing these costs to the number of miles required to redeem for a free ticket to these 13 regions, we were able to calculate the value of 1 Krisflyer Mile. When a card provided points, we converted them into miles according to the bank and the card's specific conversion rates. By adding up all the values of cash rebate and miles (including bonus rebates and mile awards) minus the annual fee over 2 years, we were able to calculate how much value a card could generate for its user.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.