What's the Best Way for YOU to Save Money?

Whether you have money to spare or are living on a tight budget, there are many ways to save money (or at least to offset your current bills). In addition, learning to successfully manage your personal finances can set you up for a better tomorrow and provide extra stability. Below, we've identified 3 different ways to save, providing insight into how you can build up your finances in a way best-suited to your needs.

Set It & Forget It: Fixed Deposits

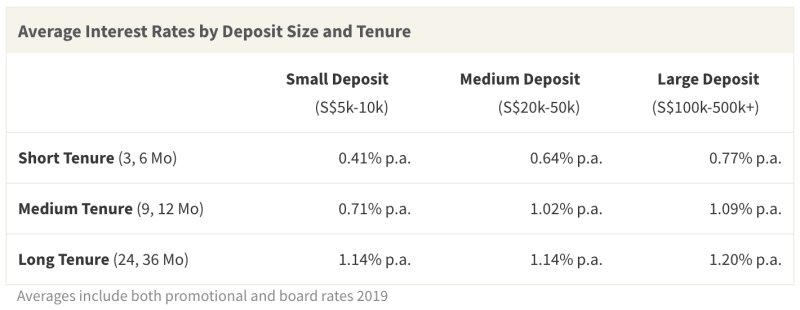

If you have a bit of extra money you can put aside for a while–without the need or temptation to touch it–a SGD fixed deposit may offer the best way for you to earn a great deal of interest. Essentially, your deposit is "locked up" for a set period of time and earns at a predetermined interest rate, based on the size of your deposit and the deposit tenure. While withdrawing your funds early often means forfeiting interest earned, those that can refrain earn at rates higher than base rates offered by most savings accounts.

Fixed deposits are also risk-free and maintenance-free. While earning high rates often requires large deposits (starting at S$5k+) and lengthy tenures, there are no extra fees or expenses, even if you do opt to close your account prematurely.

Ultimately, the value of a fixed deposit is primarily driven by its promotional rates. Rates can range up to 3% p.a. or higher under select circumstances. Nonetheless, promotions change quite frequently and can vary substantially from bank to bank. If you're looking for an easy "set it and forget it" way to save, definitely consider fixed deposits, and be sure to review the current promotions on the market.

Track & Manage to Maximise: Savings Accounts

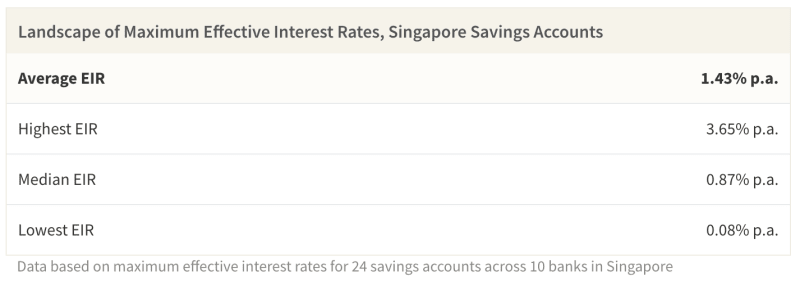

Perhaps you're looking for a more fluid way to save, and don't mind keeping tabs on your personal finances and spending behaviour. In this case, you may want to consider a high-engagement savings account that rewards consumer involvement. Several accounts in Singapore elevate rates for those who credit their salaries, consistently grow their balance, and engage with bank financial products (credit cards, loans, investments and more). In fact, while the average effective interest rate for savings accounts in Singapore is 1.43% p.a., the effective rate of more complex accounts can reach as high as 3.65% p.a.

Savings accounts also offer a bit more fluidity than fixed deposits. In most cases, consumers continue to earn interest–at least at a base rate–even on months when they make withdrawals. Nonetheless, account holders usually need to maintain a minimum balance in order to avoid "fall-below" fees. Rates for simpler accounts requiring lesser maintenance often offer very low interest rates. If you're financially savvy and can save consistently, however, opening a savings account may be a great option for you.

Save on Your Spending: Rewards Credit Cards

Actively putting aside money to save can be quite challenging, especially with the high cost of living in Singapore. If you're looking to save money but can't commit to making a fixed deposit or contributing monthly to a savings account, you can still benefit substantially from a rewards credit card. While not a traditional means of saving, using the right credit card can allow you to earn cashback that offsets your next month's bill, or miles that can be applied to your next trip, lessening your vacation costs.

Essentially, using a credit card is like applying a discount to all purchases within the rewarded categories, which are typically for very common expenses (dining, groceries, shopping, transport and many more). While there are often minimum spend requirements to access rewards rates, many are quite reasonable for the average consumer. Additionally, several credit cards have no annual fees or offer fee-waivers. If you are interested in offsetting your bills with a rewards credit card, however, be careful to spend responsibly and make payments on time in order to avoid penalties.

Ultimately, even if you're considering a fixed deposit or savings account, you may want to consider opening a new credit card as well–especially given the frequent promotions awarded to new cardholders.