BOC Family Credit Card: Is it Right for You?

BOC Family Credit Card: Is it Right for You?

ValueChampion Rating ![]()

Pros

- 10% rebate on dining & movies

- 5% w/ "Family Club" marchants

- 3% on public transport, supermarkets, hospitals bills & online spend

Cons

- Grouped categories capped at S$25/mo

- Few additional perks or privileges

- General retail earns just 0.30% cashback

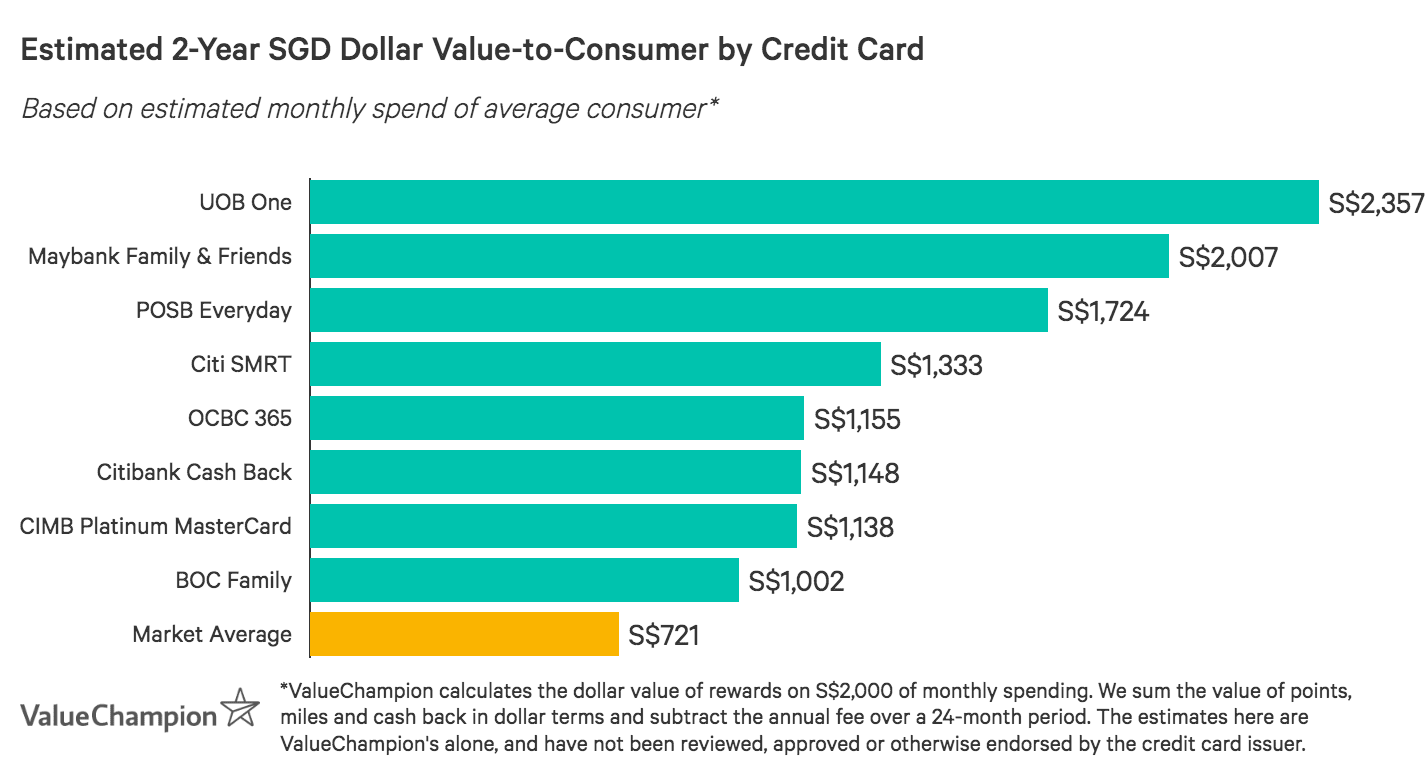

Bank of China Family Credit Card is a great option for Singaporeans with moderate, diversified budgets. Cardholders who spend at least S$800/month earn elevated cashback rates in a variety of categories. Consumers earn 10% rebate on global dining and at movie theaters, 5% with select Family Club merchants (like Watsons & POPULAR Bookstore), 3% on contactless public transport transactions, and 3% on supermarket, hospital and online retail spend. Cardholders can earn up to S$25/month from each of these four groupings, for a potential total of up to S$100/month in earnings. While this rewards cap is quite competitive, cardholders would need to consciously distribute their budgets across all categories to maximise their earnings. Nonetheless, everyday consumers with considerable practical spend may be able to earn more cashback with BOC Family Card than with similar alternatives.

BOC Family Credit Card Features and Benefits

|

|---|

Key Features:

|

What Makes BOC Family Credit Card Stand Out

BOC Family Card is a great everyday option for functional spenders–especially those with regular transit and medical spend. Cardholders who spend at least S$800/month are eligible for boosted rewards in a variety of categories: 10% rebate on global dining & at movie theaters, 5% with select "Family Club" merchants, 3% on contactless public transport spend and another 3% on supermarket, hospital & online retail spend. These categories cover an impressive breadth of expense areas, allowing consumers–especially those shopping for their family–to earn cashback on many of key purchases.

| Category | Eligible Transactions | Rebate Rate | Category Cap | Total Cap |

|---|---|---|---|---|

| Dining | Restaurants, cafes, fast food restaurants & other eating establishments worldwide | 10% | S$25 | S$100/mo |

| Movies | Transactions at any movie theatre in Singapore | |||

| Family Club Merchants | Best Denki, POPULAR Bookstore, Unity Pharmacy, Watsons, Welcia-BHG (subj. to change) | 5% | S$25 | |

| Public Transport | Contactless card transit transactions on MRT Trains & SBS/SMRT Busses via TransitLink ABT System | 3% | S$25 | |

| Supermarkets | Transactions at major supermarkets & hypermarkets | 3% | S$25 | |

| Online | Retail transactions made via the internet (exc. apply) | |||

| Hospital Bills | On-site transactions made at hospitals in Singapore |

BOC Family Card especially stands out by rewarding public transit and hospital spend. Both categories rarely earn boosted cashback–in fact, many competitor cards do not reward transit or medical spend at all. Both of BOC Family Card's categories are quite broad, however. Contactless card transit transactions on MRT Trains and SBS/SMRT Buses (via the TransitLink ABT system) and on-site transactions made at hospitals in Singapore are both eligible for 3% rebate. As a result, BOC Family Card is a great option for people seeking rewards for functional spending.

Still, BOC Family Card does have a few drawbacks. To begin with, category groupings (dining & movies; Family Club merchants; public transit and supermarkets, hospital & online spend) are each capped at S$25/month. While it's possible to earn up to S$100/month–which is quite competitive–cardholders would need to carefully track their spending to do so. Because rates vary between categories, consumers would also need to skew their spending in order to max out each cap. People with focused budgets or those with big dining budgets may not earn to their full potential with BOC Family Card.

Monthly Spend Required to Max Out Each Rewards Category

| Rewards Category Group | Rate | Cap | Spend to Cap |

|---|---|---|---|

| Dining & Movies | 10% | S$25 | S$250 |

| Family Club Merchants | 5% | S$25 | S$500 |

| Public Transport | 3% | S$25 | S$833 |

| Supermarkets, Online, Hospitals | 3% | S$25 | S$833 |

| Total Amount | S$100 | S$2,416 |

Nonetheless, BOC Family Card is still a great option for everyday household spenders looking to earn cashback on diversified spend. While there's a S$203.3 fee, it's waived the first year, allowing consumers to fully focus on earning and maxing out their rewards.

How Does BOC Family Credit Card's Rewards Program Work?

Use our quick guide below to learn how you can redeem BOC Family Card's rewards.

- Spend from principal and supplementary cardholders is combined when calculating rewards total (both count towards the same monthly earnings cap)

- Cashback is credited to the card account in the subsequent billing cycle

- Cashback can only be used to offset card transactions; it cannot be converted to or exchanged for cash, transferred or paid towards any cardmember liabilities

- Cashback is valid for 2 years and then subsequently expires

BOC Family Credit Card's Rewards Exclusions

How does BOC Family Credit Card Compare to Other Cards?

Read our comparisons of BOC Family Card with other cards and learn what makes each card unique in their own way. We compare and contrast each card to highlight its uniqueness to help you identify the card that you need.

| BOC Family Credit Card v. OCBC 365 Card | |

|---|---|

| |

| OCBC 365 Card is another great "everyday" option that even comes with a spend-based fee waiver. Cardholders who spend at least S$800/month can earn up to 6% on dining & online food delivery, 3% on groceries, land transport, online travel bookings & recurring bill-pay and 0.3% on EZ-Link and Transitlink spend. While OCBC 365 Card does not reward medical spend and offers a much lower cashback rate on public transit, it does provide competitive cashback for bill-pay. Additionally, OCBC 365 Card's S$80/month rewards cap applies to total earnings, which allows consumers to spend more fluidly without excessive category tracking. OCBC 365 Card also stands out by offering an easy fee-waiver. Consumers who spend S$10k/year are exempt from the S$192.6 annual fee. Overall, OCBC 365 Card is a more affordable everyday option for household spenders whose budgets may vary slightly from month to month. | |

| BOC Family Credit Card v. Maybank Family & Friends Card | |

|---|---|

| |

| If you're a household spender that primarily shops in Singapore and Malaysia, you may want to consider Maybank Family & Friends Mastercard. Cardholders earn 5% cashback in these regions on fast food & food delivery, groceries, transport, data communications & online TV streaming all after just S$500 minimum spend. This is one of the most competitive rates on the market for lower spenders. However–even better–those who spend at least S$800/month earn 8% rebate in all of these categories, up to S$80/month in rewards. Given the extent of rewards-eligible spend, it's fairly easy for a family spender to achieve this minimum.

| |

| BOC Family Credit Card v. CIMB Platinum Mastercard | |

|---|---|

|

|

| Read Our Full Review allows cardholders to earn up to 10% cashback in a variety of categories without ever having to pay an annual fee. In fact, consumers who spend at least S$800/month earn 10% rebate on global dining, travel spend in foreign currency, transport & petrol, medical spend and with select local electronics & furnishings merchants. While many of these categories overlap with BOC Family Card's, it's important to point out that "transport" excludes EZ-Link & Transitlink and "medical" excludes government hospitals and polyclinics.

| |

| BOC Family Credit Card v. OCBC 365 |

|---|

|

| OCBC 365 Card is another great "everyday" option that even comes with a spend-based fee waiver. Cardholders who spend at least S$800/month can earn up to 6% on dining & online food delivery, 3% on groceries, land transport, online travel bookings & recurring bill-pay and 0.3% on EZ-Link and Transitlink spend. While OCBC 365 Card does not reward medical spend and offers a much lower cashback rate on public transit, it does provide competitive cashback for bill-pay. Additionally, OCBC 365 Card's S$80/month rewards cap applies to total earnings, which allows consumers to spend more fluidly without excessive category tracking. OCBC 365 Card also stands out by offering an easy fee-waiver. Consumers who spend S$10k/year are exempt from the S$192.6 annual fee. Overall, OCBC 365 Card is a more affordable everyday option for household spenders whose budgets may vary slightly from month to month. |

| BOC Family Credit Card v. Maybank Family & Friends |

|---|

|

| If you're a household spender that primarily shops in Singapore and Malaysia, you may want to consider Maybank Family & Friends Mastercard. Cardholders earn 5% cashback in these regions on fast food & food delivery, groceries, transport, data communications & online TV streaming all after just S$500 minimum spend. This is one of the most competitive rates on the market for lower spenders. However–even better–those who spend at least S$800/month earn 8% rebate in all of these categories, up to S$80/month in rewards. Given the extent of rewards-eligible spend, it's fairly easy for a family spender to achieve this minimum.

|

| BOC Family Credit Card v. CIMB Platinum Mastercard |

|---|

|

|

|

| Read Our Full Review allows cardholders to earn up to 10% cashback in a variety of categories without ever having to pay an annual fee. In fact, consumers who spend at least S$800/month earn 10% rebate on global dining, travel spend in foreign currency, transport & petrol, medical spend and with select local electronics & furnishings merchants. While many of these categories overlap with BOC Family Card's, it's important to point out that "transport" excludes EZ-Link & Transitlink and "medical" excludes government hospitals and polyclinics.

|

Read Also:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.