DBS Woman's World Credit Card Review: Shopping Miles Rewards in Singapore and Overseas

DBS Woman's World Credit Card Review: Shopping Miles Rewards in Singapore and Overseas

ValueChampion Rating ![]()

Pros

- 0% interest payment plans available

- Good rewards for online shopping

- Online purchase protection

Cons

- Lacks travel perks

- Limited rewards categories

DBS Woman's World Card maximises rewards for online shoppers and is perfect for consumers who prefer to pay for their purchases in instalments. Cardholders earn 10X DBS points or 20 miles per S$5 online shopping spend. The card also offers consumers discounts and gifts in beauty, wellness, and fashion. However, one of its best attributes is the 0% Interest Payment Plans, which allows shoppers to pay for purchases over 6 months with 0% interest.

While cardholders can also enjoy benefits like discounts on rental cars, DBS Woman's World Card is less valuable for non-shoppers. Local spend earns just 1X DBS points or 2 miles per S$5, and overseas spend earns 3X DBS points or 6 miles. Nonetheless, the annual fee of S$194.4 is waived the first year and is subsequently waived with every annual spend of S$25,000. This means that for the average spender, DBS Woman's World Card may easily become a no-fee card. Shoppers who can meet this annual spend and who prefer to pay for purchases over instalments might find DBS Woman's World Card to be a great fit for their lifestyle.

DBS Woman's World Credit Card Features and Benefits

|

|---|

Key Features:

|

What Makes DBS Woman's World Card Stand Out

DBS Woman's World Card offers frequent online shoppers a great way to maximise rewards for their spend and pay for purchases in flexible, interest-free instalments over up to 24 months. Online spend is rewarded with 10X DBS points (or 20 miles) per S$5. In addition, cardholders have access to complimentary gifts and discounts of up to 20% on select beauty, wellness and fashion merchants. Consumers can also enjoy up to 10% cashback on Booking.com accomodation bookings.

One of the card's most unique features, however, is the 0% Interest Payment Plan, which splits purchases into 0% interest instalments for up to 24 months. This feature is particularly great for shoppers who tend to overspend or who prefer to pay over time. However, there are a few things to keep in mind about this payment plan. Purchases must be made from their list of merchant offers, which may vary in terms and conditions. In addition, such purchases are not eligible to earn rewards. Also, cancellation of this card would result in termination and immediate payment for all on-going instalment plans financed by the card. Each terminated instalment plan will have a early termination fee off S$150. Overall, the plan is best for shoppers who can pay back their purchase within the 6 months.

There are a few drawbacks to DBS Woman's World Credit Card. First, its upsized shopping rewards are limited only to online, while competitors reward online, offline, local, and overseas purchases. Secondly, its general rewards rates are low at 0.4 miles for S$1 local spend and 1.2 miles for overseas spend. Also, while the card does have several benefits, it lacks travel perks and privileges that might be important to some consumers. Travel insurance, airport lounge access, limo transfers, golfing privileges are more are among the privileges not included. The card also has a high salary requirement of S$80,000 per year which limits accessibility.

Overall, however, DBS Woman's World Card offers online shoppers and spenders seeking payment by instalments a great option to both earn rewards and save money. With an annual fee of S$194.4 which is waived the first year, and thereafter with an annual spend of S$25,000, the card might even be considered no-fee for the average consumer. While consumers who mostly shop in-store or who are more focused on everyday spend or overseas spend might not be the best fit for this card, consumers with high online spend and who can avoid the annual fee will benefit from DBS Woman's World Card.

How Does DBS Woman's World Credit Card's Rewards Program Work?

Use our quick and easy-to-read guide below to learn how you you can redeem DBS Woman's World Card rewards.

- Spend rewarded in DBS Points (redeemable as rewards vouchers, instant-redemption at select merchants, miles, and as payment for annual fee)

- Cardholder can redeem points for KrisFlyer Miles or Asia Miles, Qantas points of Air Asia Big points in blocks of 5,000 DBS Points for 10,000 air miles through DBS Rewards Frequent Flyer Programme. Administrative fee of S$27.00 applies for each miles redemption.

- Cardholder can automatically convert points to KrisFlyer Miles on the 10th day of each quarter (January, April, July and October) through DBS KrisFlyer Miles Auto Conversion Programme. Points are converted in blocks of 500 DBS Points for 1,000 KrisFlyer Miles. Administrative fee for miles redemption does not apply, but participants must pay an annual fee of S$43.20.

- DBS Points earned through DBS Woman's World Card expire one year from the quarterly period in which they were earned

DBS Woman's World Credit Card Rewards Exclusions

Some credit card expenditures are ineligible for cash back or rebate. We identify these exclusions in the table below.

| Exclusion Category | Description |

|---|---|

| Bank Fees | Instalment payment plan purchases, preferred payment plans, balance transfer, fund transfer, cash advances, annual fees, interest, late payment charges, all fees charged by Bank, miscellaneous charges imposed by Bank (unless otherwise stated in writing by Bank), payments made via online banking* |

| Transfers & Bill Payments | Any top-ups or payment of funds to payment service providers, prepaid cards and any prepaid accounts (including EZ-Link, NETS FlashPay, Singtel Dash and Transit Link); payments done via AXS, SAM, eNETS; payments made to CardUp, iPaymy, and Mileslife*; payments made via telephone or mail order*; payments to utility bill companies*; transactions related to crypto currencies* |

| Institutional Payments | Payments to educational institutions, government institutions and services (court cases, fines, bail and bonds, tax payment, postal services, parking lots and garages, intra-government purchases and any other government services not classified here), insurance companies (sales, underwriting, and premiums), financial institutions (including banks and brokerages), non-profit organisations, hospitals*, professional service providers (accounting, auditing, bookkeeping services, advertising services, funeral service and legal services and attorneys)* |

| Betting or Gambling | Betting (including lottery tickets, casino gaming chips, off-track betting, and wagers at race tracks) through any channel |

How does DBS Woman's World Credit Card Compare Against Other Cards?

Read our comparisons of DBS Woman's World Card with other cards and learn what makes each card unique in their own way. We compare and contrast each card to highlight its uniqueness to help you identify the card that you need.

DBS Woman's World Credit Card v. Citi Rewards Card

- Pros

- Great for online & offline shopping

- Beneficial for frequent travellers

- Cons

- Less valuable for infrequent shoppers

- Foreign transaction fees apply

Shoppers looking to maximise rewards for online and fashion spend might want to consider Citi Rewards Card. While cardholders earn only 0.4 miles per S$1 on general spend, they receive 4 miles per S$1 spend on online transactions as well as on clothes, bags, or shoes–both locally and overseas.

DBS Woman's World Credit Card limits rewards-eligible purchases to online only. However, travel bookings are rewarded; Citi Rewards Card excludes online bookings from earning rewards. Citi Rewards Card also caps monthly rewards at 4,000/month, while DBS Woman's World Card sets its cap at 8,000. Finally, Citi Rewards Card has an annual fee of S$192.6 which is only waived the first year, while DBS Woman's World offers a waiver. Overall, shoppers who want rewards for spend both online and offline may prefer Citi Rewards Card.

DBS Woman's World Credit Card v. OCBC Titanium Rewards Card

- Pros

- 10 pts (4 miles) per S$1 on fashion & select retail (Qoo10, Amazon, & more)

- Fee waiver with S$10,000 annual spend

- Cons

- 1 pt (0.4 miles) per S$1 other spend

- Earnings capped at 48,000 miles per year (worth S$480)

Shoppers who spend on fashion but want to avoid an annual fee might consider OCBC Titanium Rewards Card. Like a few other cards on the market, OCBC Titanium Rewards Card offers 4 miles per S$1 spend on clothes, shoes, bags, and more online and offline, locally and overseas. However, OCBC Titanium Rewards Card is different in that its annual fee of S$192.6 is waived for two years, then subsequently with every annual spend of S$10,000. DBS Woman's World Card also offers an easily waivable annual fee, but only rewards online purchases. Another difference is that OCBC Titanium Rewards Card caps shopping rewards at 4,000 miles, while DBS Woman's World Card rewards up to 8,000 per month. Ultimately, consumers looking to avoid an annual fee should consider OCBC Titanium Rewards Card if they mostly spend on fashion. If they spend more in general, and mostly spend online, DBS Woman's World Card is a better fit..

DBS Woman's World Credit Card v. CIMB Visa Signature Card

- Pros

- Rewards online shopping, groceries and beauty spend

- Rewards pet spend and cruises

- No annual fee credit card

- Cons

- Lacks discounts on transport & petrol

- Speciliazed spend

- Doesn't fit frequent travellers

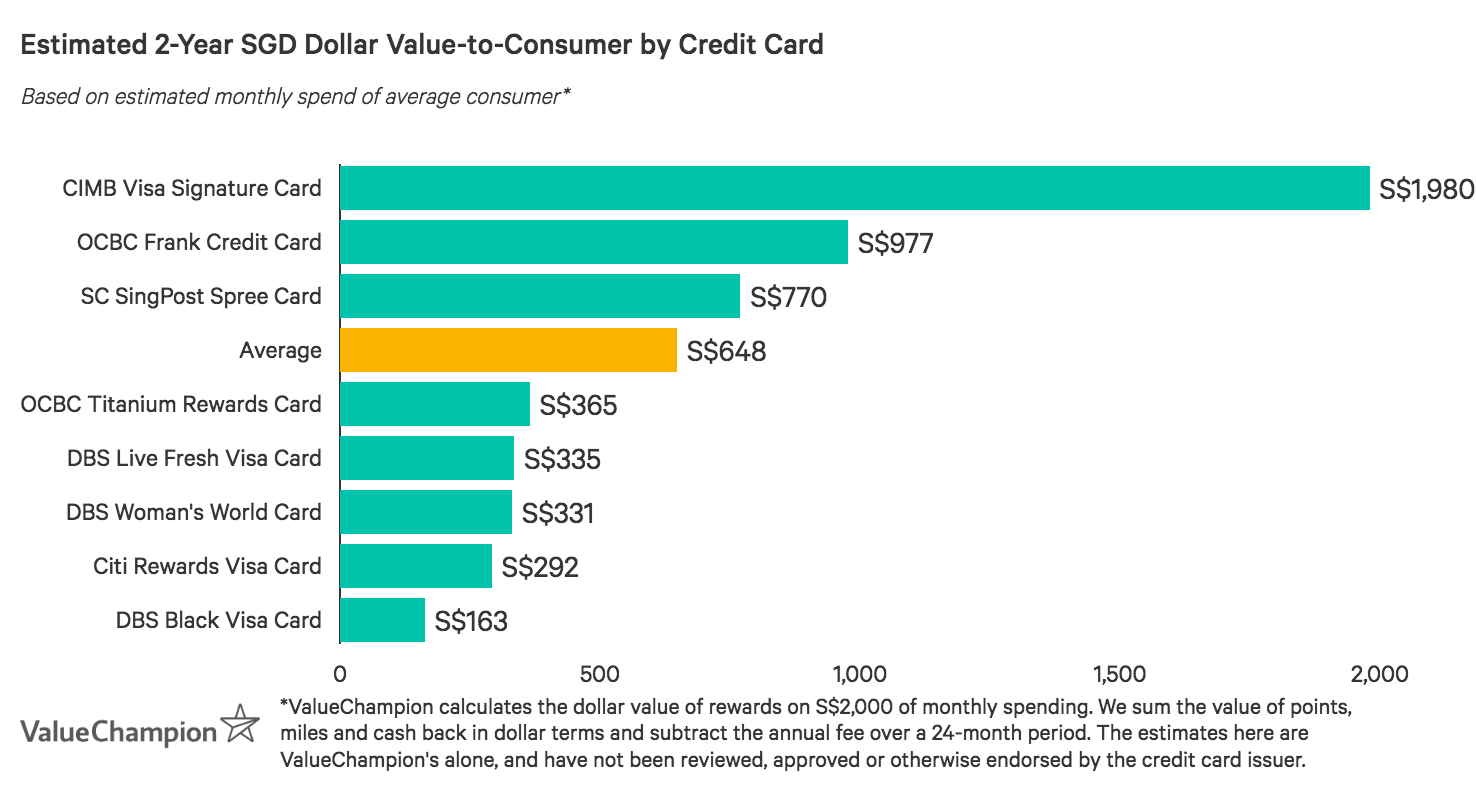

Consumers looking to earn no-fee cashback on beauty, wellness and online shopping should consider CIMB Visa Signature Card. With cashback of 10% in both of these categories–as well as for groceries, pet care, and cruise bookings–consumers earn a cash rebate equivalent of 10 miles per S$1 spend–a market-leading rate for shopper cards. In addition, cashback is cumulatively capped at S$100 per month, or about 10,000 miles. While there's a minimum spend of S$800 to unlock this rate, the card has no annual fee, making it easy to earn rewards without any maintenance. Compared to DBS Woman's World Credit Card, CIMB Visa Signature might be a better option for those seeking cashback as well as unique rewards outside of shopping.

DBS Woman's World Credit Card v. DBS Live Fresh Visa Card

- Pros

- Great rewards on contactless payment methods (Visa payWave)

- Green cashback on eco-eateries and retailers

- Various entertainment discounts and promotions

- Cons

- Lacks travel and overseas spend rewards

- Not suitable for low budgets

DBS Live Fresh Card is a great cashback card for online shoppers who frequently pay with Visa payWave. The card offers 5% cashback on purchases in these categories (rate capped at S$40), with all other spend earning 0.3% (capped at S$20). Considering 1 mile equals roughly S$0.01 in value-to-consumer, these rates translate to 5 miles per S$1 for online and Visa payWave spend and 0.3 miles per S$1 general spend. Compared to shopper cards offering miles, DBS Live Fresh Visa Card offers a higher rewards rate for online spending but a lower rate for general spend. Ultimately, however, DBS Live Fresh Visa Card requires a minimum spend of S$600 to unlock the higher rate and its S$128.4 annual fee is only waived the first year. Consumers who don't mind paying an annual fee and mostly spend online or through mobile transactions could benefit from DBS Live Fresh Visa Card. Those who would rather avoid a fee and earn mile rewards from online spend might instead consider DBS Woman's World Credit Card.

Read Also:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.