Maybank Platinum Visa Credit Card: Who Should Get It?

Maybank Platinum Visa Credit Card: Who Should Get It?

ValueChampion Rating ![]()

Pros

- Great starter card for young adults

- Good fit for budgets between S$300 and S$500/month

- S$80 annual fee

Cons

- Few extra perks

- Doesn't award specialised spend (ie dining, shopping)

Maybank Platinum Visa Card is by far the best cashback card for lower spenders. Cardholders can earn 3.33% rebate with as little as S$300 monthly spend, up to S$30/quarter. At this spend level, most cards offer just 0.3% base cashback. In addition, spending S$1,000/month earns S$100/quarter. Cardholders also receive useful perks like free travel insurance. Finally, the S$20.0 quarterly service fee is waived simply with card use, making Maybank Platinum Visa Card an easy, maintenance-free way for low spenders to maximise their cashback.

Maybank Platinum Visa Credit Card Features and Benefits

|

|---|

Key Features:

|

What Makes Maybank Platinum Visa Credit Card Stand Out

Maybank Platinum Visa Card offers low spenders an easy way to earn rewards for nearly all of their purchases without paying a fee. Cardholders earn 3.33% rebate on local and overseas purchases, as long as they’ve spent at least S$300 per month across a calendar quarter. Spending at least S$300/month earns S$30/quarter, and S$1,000/month earns S$100/quarter. In addition, there are no category or merchant-based restrictions, which makes earning easy.

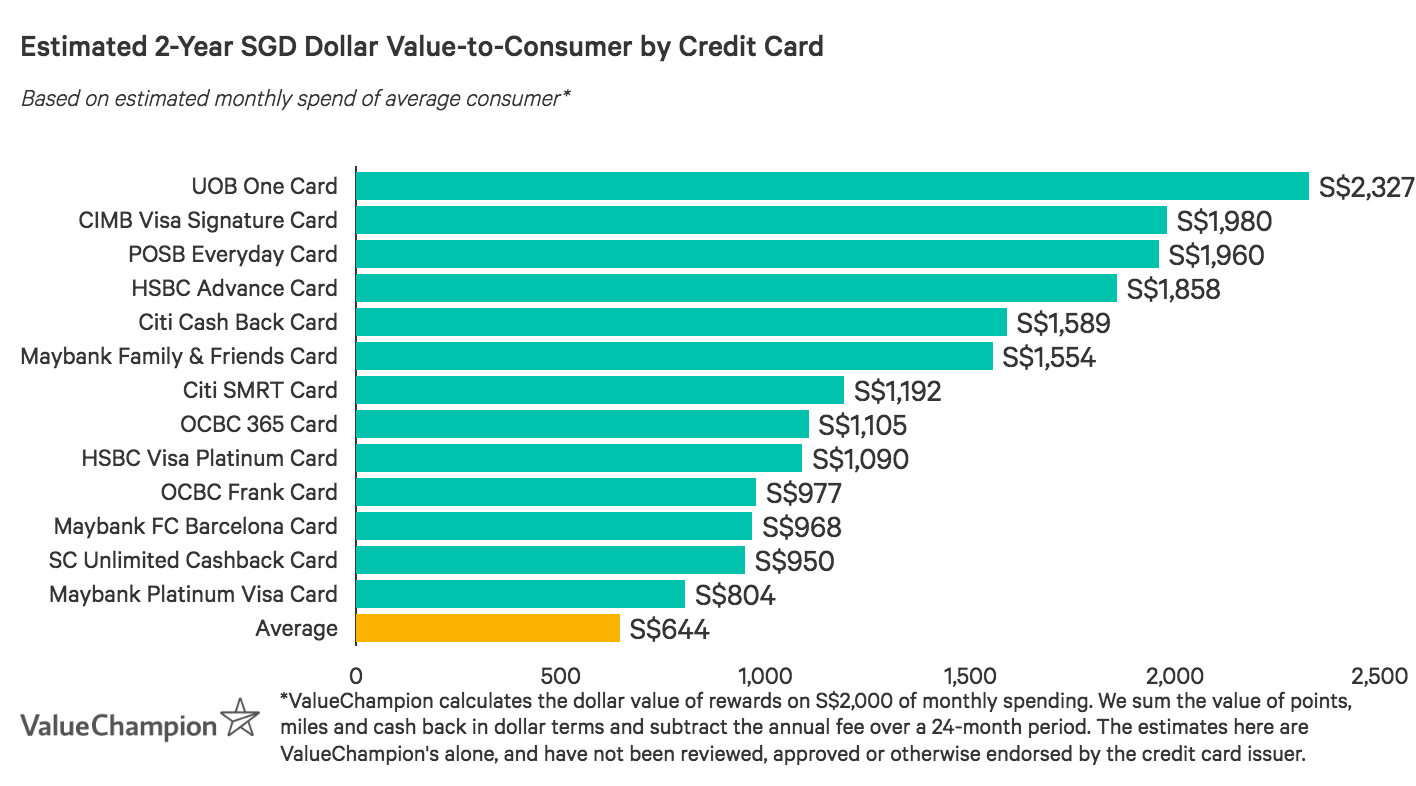

Low spenders, primarily with S$300-S$500 monthly budgets, are especially likely to benefit from Maybank Platinum Visa Card. The 3.33% rebate is one of the highest offered after just S$300 minimum spend, and with only S$1,200 annual spend cardholders can earn S$120. Many cards have minimum spends of at least S$500, and have base rates as low as 0.2% cashback.

Despite these advantages, Maybank Platinum Visa Card has a few drawbacks. While the 3.33% flat rebate is relatively high, it’s lower than category rates offered by specialised cards (8% for dining, for example). Additionally, consumers who spend S$500+/month can benefit more from other cards, like UOB One Card, which have higher earnings caps. Finally, while cardholders receive free travel insurance, there are few other perks.

Quarterly Rebate by Spend Level

| Min. Monthly Spend | Maybank Platinum | UOB One |

|---|---|---|

| S$300 | S$30 | - |

| S$500 | S$30 | S$50 |

| S$1,000 | S$100 | S$100 |

| S$2,000 | S$100 | S$300 |

Even still, Maybank Platinum Visa Card is excellent for individuals with lower budgets and offers easy convenience with its flat rewards rate. It has no annual fee, and its S$20 quarterly service fee is waived as long as the card is used once every 3 months. Essentially, the card is a maintenance-free way to earn on nearly all spend. Altogether, Maybank Platinum Visa Card is worth considering for easy rebates without high spend.

How Does Maybank Platinum Visa Credit Card’s Rewards Program Work?

Use our quick and easy-to-read guide below to learn how you you can redeem card rewards.

- Every 1 dollar of cash rebate earned is equal to S$1

- Quarterly rebate is based on fixed-quarter spending (January-March, April-June, July-September, October-December)

- Quarterly rebates may only be used to offset transactions on the Principal card

- Cash rebates earned will be credited to the card by the following month

Maybank Platinum Visa Credit Card Rewards Exclusions

Some credit card expenditures are ineligible for earning rewards. We identify these exclusions below.

How does Maybank Platinum Visa Credit Card Compare Against Other Cards?

- Pros

- Great starter card for young adults

- Good fit for budgets between S$300 and S$500/month

- S$80 annual fee

- Cons

- Few extra perks

- Doesn't award specialised spend (ie dining, shopping)

Read our comparisons of Maybank Platinum Visa Card with other cards and learn what makes each card unique in their own way. We compare and contrast each card to highlight its uniqueness to help you identify the card that you need.

Maybank Platinum Visa Credit Card v. UOB One Card

- Pros

- Good fit for budgets of at least S$2,000 per month

- Easy cashback on daily spend

- Gives rebates for paying bills

- Cons

- Doesn't fit inconsistent budgets

- Annual fee

UOB One Card is an excellent flat cashback card for consumers consistently spending S$2,000+/month. Like Maybank Platinum Card, UOB One Card uses a tiered quarterly rebate system that rewards cardholders based on their minimum spend, and offers 3.33% rebates for consistent S$500 and S$1,000/month spends and 5% for S$2,000/month spends. While there's a S$500 minimum, caps are higher (S$50, S$100, S$300/quarter, respectively). Maybank Platinum Card is better for lower spenders who cannot consistently meet a S$500/month minimum.

Maybank Platinum Visa Card v. Citi SMRT Card

- Pros

- Good rewards rates for modest budgets

- SMRT$ rewards on EZ-Reload transactions

- Cons

- Not suitable for higher budgets

- Lacks travel and overseas rewards

Cardholders on a modest budget can access elevated cashback rates without a minimum spend requirement with Citi SMRT Card. Consumers earn 5% rebates on fast food dining, cafes, groceries, and cinemas, 3% for online spend, and 2% on health and beauty. The card also has EZ-Link functionality and earns 2% rebate on Top-Ups. However, rewards-eligible merchants are limited, and general spend earns just 0.3%. Commuters who spend in these categories may prefer Citi SMRT Card, but Maybank Platinum Visa Card offers those with limited budgets a lower-maintenance option.

Maybank Platinum Visa Credit Card v. OCBC 365 Card

- Pros

- 6% rebate on dining, 3% on groceries, transport, utilities, online travel

- Fee waiver with S$10,000 annual spend

- Up to 22.1% fuel savings at Caltex, 20.2% at Esso

- Cons

- 0.3% rebate on general spend

- High S$800 minimum spend requirement

OCBC 365 Card is great for average consumers looking for everyday cashback on essentials. Cardholders earn 6% rebate on dining, 3% on groceries, transport, utilities and online travel spend and up to 23% fuel savings. While these rates allow consumers to earn quickly in key categories, there’s a S$800 minimum spend requirement and cashback is capped at S$80/month. Average spenders with a diversified budget could benefit from this card, but lower spenders seeking a simple, flat rate card might prefer Maybank Platinum Visa Card.

Maybank Platinum Visa Credit Card v. HSBC Revolution Card

- Pros

- Great rewards on local dining and entertainment

- Online shopping perks

- No-fee card

- Cons

- Lacks rewards for frequent travellers who spend large amounts overseas

- Not suitable for low budgets

Social spenders can maximise rewards for local dining, entertainment and online spend with HSBC Revolution Card. Cardholders earn 2 miles per S$1 spend (equal to about 2% rebate) in each of these categories, with no spend requirement or earnings cap. Overseas spend earns just 0.4 miles per S$1 (about 0.4%). While these features make the card great for local spenders with low or variable budgets, HSBC Revolution Card’s S$160.5 fee is waived with S$12,500 spend–consumers who can reach this are more likely to benefit than very low spenders, who may prefer Maybank Platinum Visa Card.

To view the best cashback credit cards available in Singapore, check over here for more!

Read Also:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.