Citi Rewards Credit Card: Best Miles Card for Online & Shopping

Citi Rewards Credit Card: Best Miles Card for Online & Shopping

ValueChampion Rating ![]()

Pros

- Great for online & offline shopping

- Beneficial for frequent travellers

Cons

- Less valuable for infrequent shoppers

- Foreign transaction fees apply

If you enjoy shopping to keep up with the latest fashion trends and often spend online, Citi Rewards Card offers the best way to maximise rewards for your purchases. Cardholders earn 10X rewards points or 4 miles per S$1 spend on online and shopping purchases, rides with Grab and Gojek, online food delivery as well as ordering groceries online. Both local and overseas spend are rewards-eligible, making Citi Rewards Card one of the most versatile shopping cards on the market. In fact, no competitor offers such high rates for online purchases. Additional perks include free travel insurance and access to Citi World Privileges’ dining & lifestyle discounts. Overall, if you want flexible rewards for online and fashion spend, you may want to consider Citi Rewards Card.

Citi Rewards Credit Card Features and Benefits

|

|---|

Key Features:

|

| Promotions:

|

What Makes Citi Rewards Credit Card Stand Out

Citi Rewards Card is an extraordinary option for frequent fashion shoppers who also enjoy making purchases online. In fact, it’s the only shopper card offering high, flexible rates for both fashion and online spend. Cardholders earn 4 miles per S$1 on clothing, bags, shoes (& more) both locally and overseas, which makes it easy to earn wherever you are. Even more, this same rate applies to nearly all online transactions (excluding travel bookings and mobile wallet pay).

Competitor cards aren’t nearly as flexible. Some, like DBS Woman's World Card, prioritize online spend while minimizing rewards for offline fashion. OCBC Titanium Rewards Card, on the other end of the spectrum, rewards all kinds of fashion spend, but limits online rewards to specific merchants. Citi Rewards Card stands out for top miles rates for both online and fashion spend.

| Spend & Details | Citi Rewards | DBS Woman’s World | OCBC Titanium |

|---|---|---|---|

| Online–General Spend | 4.0mi/S$1 | 4.0mi/S$1 | 0.4mi/S$1 * |

| Offline–Fashion Spend | 4.0mi/S$1 | 0.4mi/S$1 | 4.0mi/S$1 |

| Monthly Rewards Cap | 4,000mi | 8,000mi | 4,000mi |

| Fee-Waiver Option | N/A | YES | YES |

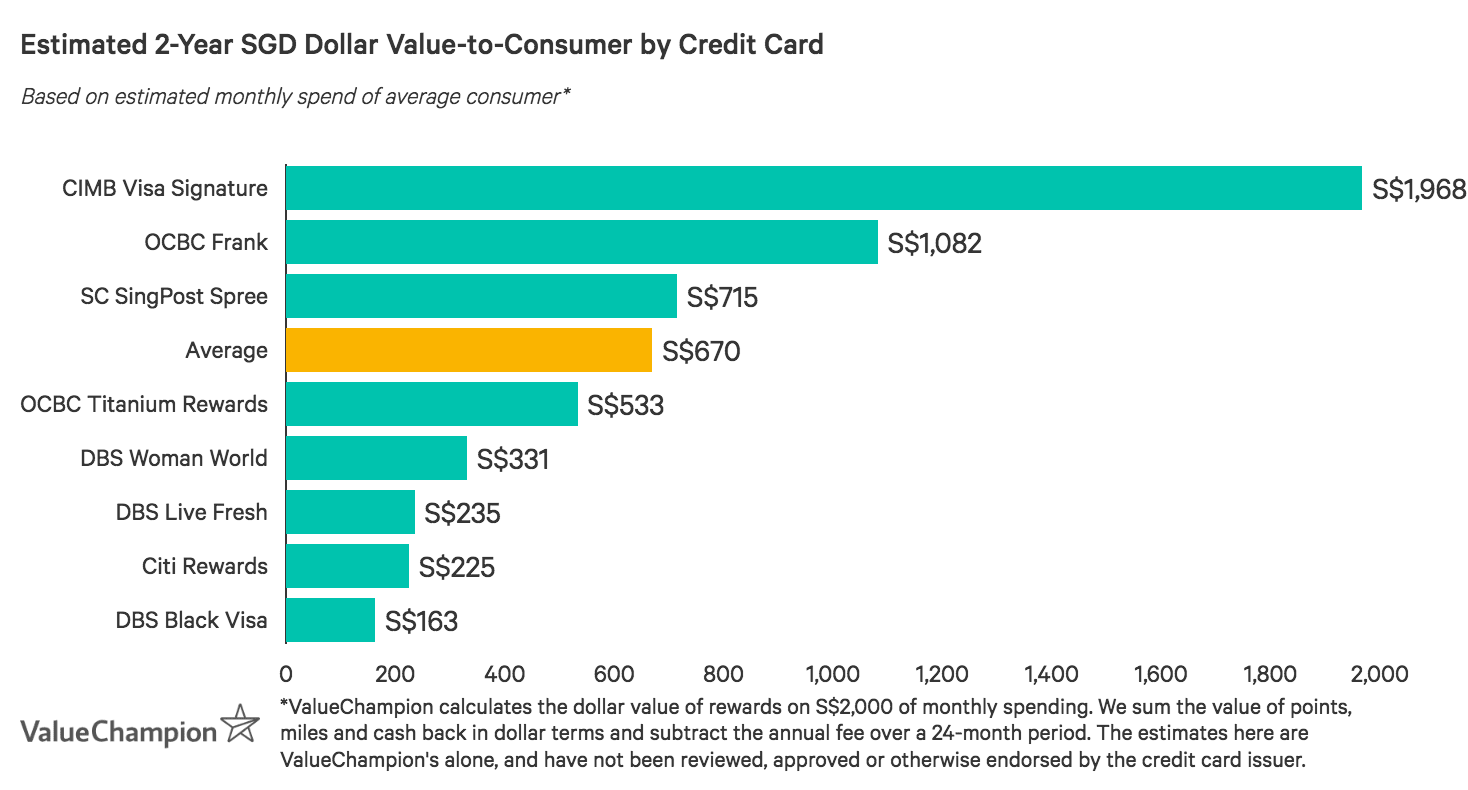

It’s worth mentioning, however, that Citi Rewards Card has a few drawbacks. General spend earns just 0.4 miles per S$1 spend, which means the card is less valuable for infrequent shoppers. On the other hand, monthly rewards are capped at 4,000 miles, which has a relatively low S$40 value-to-consumer. Higher fashion & online spenders may feel limited by this cap. Finally, the S$194.40 fee is waived just the 1st year, and is ineligible for a waiver after that. Those hoping to avoid an annual fee may prefer alternative shopper cards.

Nonetheless, Citi Rewards Cardholders enjoy added perks like free travel insurance, access to Citi World Privileges, and up to 14% fuel savings with Shell and Esso. Cardholders can also earn rewards for paying their taxes, rent, condominium management fees, school fees, and electricity bills through Citi PayAll (though there's a 1-5–2% fee for this service). These benefits significantly extend the card's benefits. Ultimately, Citi Rewards Card is the best shopper card on the market if you frequently spend both online and on fashion.

How Does Citi Rewards Credit Card's Rewards Program Work?

Use our quick guide below to learn how you can actually redeem Citi Rewards Card's rewards.

- Citi Rewards points are valid for 5 years

- Points balance appears on cardholder's monthly statement

- Points can be redeemed for merchandise, vouchers, cash rebates or miles

- Miles conversion rate is 25,000 points to 10,000 miles with loyalty program affiliate

- There is an administrative fee of S$25 per point transfer

Citi Rewards Credit Card's Rewards Exclusions

The following credit card expenditures are ineligible for cash back or rebate.

How does the Citi Rewards Credit Card Compare Against Other Cards?

- Pros

- Great for online & offline shopping

- Beneficial for frequent travellers

- Cons

- Less valuable for infrequent shoppers

- Foreign transaction fees apply

Read our comparisons of Citi Rewards Card with other cards and learn what makes each card unique in their own way. We compare and contrast each card to highlight its uniqueness to help you identify the card that you need.

Citi Rewards Card v. OCBC Titanium Rewards Card

- Pros

- 10 pts (4 miles) per S$1 on fashion & select retail (Qoo10, Amazon, & more)

- Fee waiver with S$10,000 annual spend

- Cons

- 1 pt (0.4 miles) per S$1 other spend

- Earnings capped at 48,000 miles per year (worth S$480)

OCBC Titanium Rewards Card offers an excellent way for frequent shoppers to earn miles from all purchases without paying an annual fee. As with Citi Rewards Card, fashion spend earns 4 miles per S$1 locally and overseas, online or offline. Cardholders also earn at this rate for spend with select retail merchants like Amazon, Shopee, Qoo10 and Lazada. This is different than Citi Rewards Card, which offers miles for online spend without merchant restrictions.

Unlike Citi Rewards Card, however, OCBC Titanium offers a fee-waiver. Cardholders are exempt from the S$192.6 fee with just S$10,000 annual spend. Cardholders also enjoy unique perks like access to airport lounges & JetQuay Quayside. Citi Reward Card’s offerings are a bit more limited. Overall, if you’re a frequent retail shopper looking for a no-fee miles card, OCBC Titanium Rewards may be a better option for you.

Citi Rewards Card v. Citi PremierMiles Card

- Pros

- Frequent traveler perks

- Low fees

- Flexible miles redemption

- Cons

- Lacks luxury perks

- Not suitable for occasional travel

Citi PremierMiles Card is a great card for consumers looking to earn miles from daily spend while also benefiting from frequent bonuses and promotions. The earn rate for miles with Citi PM is fairly standard with S$1 spend earning 1.2 Citi Miles for local transactions and 2 miles for overseas purchases. However, consumers receive added value through welcome gifts and travel perks. New cardholders might expect to earn 45,000 Citi miles after making their first annual payment and spend a minimum of S$9,000. Cardmembers also receive travel insurance and access to airport lounges worldwide. Travellers looking to earn miles on a diversified set of expenditure would benefit from Citi PremierMiles Card. Consumers who are interested in earning miles but spend primarily on shopping would benefit more so from Citi Rewards Card.

Citi Rewards Card v. Citi Prestige MasterCard

- Pros

- Great luxury benefits

- Ideal for higher budgets

- Great golfing and travel perks

- Cons

- Very high annual fees

- Unsuitable for moderate budgets

Citi Prestige MasterCard is best fit for affluent consumers–especially Citibank customers with Citigold status–who seek luxury travel perks to go along with high rates for miles earned. To begin with, Citi Prestige MasterCard is intended for affluent consumers. The annual fee is a substantial S$535 (non-waivable) and consumers must earn at least S$120,000 per year in order to qualify. However, for those who meet these requirements and spend at least S$4k–S$5k per month, Citi Prestige MasterCard offers extravagant and worthwhile perks. For instance, cardholders receive unlimited airport lounge access, complimentary hotel and resort stays, complimentary limousine transfers, golf privileges, and more. In addition, Citigold status customers receive additional miles with every purchase. Those who prioritize travel benefits and are willing to pay for luxury privileges may be a fit for Citi Prestige MasterCard. Those who prioritize shopping in their spending and are willing to forego exclusive perks might consider Citi Rewards Card instead.

Citi Rewards Card v. OCBC Frank Card

- Pros

- 6% rebate on online, mobile contactless, and FX spend

- Fee waiver with S$10,000 annual spend

- Cons

- 0.3% rebate on general purchases

- Annual fee after 2 years

- Capped cashback at S$75

OCBC Frank Card is a top-notch cashback option for young adults or lower spenders who frequently shop online and use mobile payment methods. OCBC Frank Card rewards expenditures in both of these areas with 6% cashback. While total cashback is capped S$60 total per month, the annual fee of S$80 is waived for the first two years (and in subsequent years for those who spend S$10,000 per year), making the card maintenance-free. Other benefits include a 5% entertainment rebate and 3% rebate on cardholders' first two NETS FlashPay Auto Top-Ups. In general, OCBC Frank Card is a great option for lower spending young adults who shop online, while Citi Rewards Card is a better fit for average to above average spending adults who shop through a variety of channels.

Citi Rewards Card v. Standard Chartered SingPost Spree Card

- Pros

- Great for monthly budgets below S$500

- Rewards overseas retailer shopping

- Cons

- Not suitable for monthly budgets of S$500+

- Lacks local shopping rewards

The Standard Chartered SingPost Spree Credit Card is a great cashback card for online shoppers who frequently buy from overseas vendors. With rebates up to 3% on all online spend in foreign currency and vPost spend, SC SingPost Spree offers great rewards potential for consumers who shop with overseas vendors through Amazon or Taobao. There's no minimum spend and the annual fee of S$192.60 is waived for two years, making the card easy and accessible. However, because of its limited rewards scope and a monthly cap of S$60, SC SingPost Spree would not be as beneficial to diversified spenders with a higher budget. Citi Rewards Card is a great fit for average to above average spenders who shop through a variety of channels.

Citi Rewards Card v. DBS Woman's World Card

- Pros

- 0% interest payment plans available

- Good rewards for online shopping

- Online purchase protection

- Cons

- Lacks travel perks

- Limited rewards categories

DBS Woman's World Card is a great shopping card for consumers who spend online and may need to pay back larger purchases in instalments. The card is similar to Citi Rewards Card in prioritizing shopping but focuses further on online purchases, awarding consumers 4 miles per every S$1 online spend. Earnings for overseas and general retail are relatively low at 1.2 miles per S$1 overseas and 0.4 miles per S$1 general local spend.

However, what makes DBS Woman's World Card stand out is its 0% interest free payment plan which offers flexible payments across 3, 6, 12, 18 or 24 months, with no processing fee for up to 12 months. Because of its savings potential in the way of interest, this benefit makes DBS Woman's World Card the best option for consumers who overspend, or prefer to pay for larger purchases over time. However, we should note that purchases made on the 0% instalment plan are ineligible for mile rewards. Citi Rewards Card is a better bet for consumers who shop overseas and offline, and who pay for purchases in one instalment.

Citi Rewards Card v. CIMB Visa Signature Card

- Pros

- Rewards online shopping, groceries and beauty spend

- Rewards pet spend and cruises

- No annual fee credit card

- Cons

- Lacks discounts on transport & petrol

- Speciliazed spend

- Doesn't fit frequent travellers

For consumers looking to earn cashback on online shopping spend, CIMB Visa Signature Card is worth considering. This card has no annual fee and offers 10% cashback on online shopping after a minimum qualifying spend of S$800 per month, which is accessible to average spenders. In addition, CIMB Visa Signature also offers 10% cashback on beauty expenses, groceries, pet care and cruise bookings. Consumers looking to earn cashback without maintenance may want to consider CIMB Visa Signature. Consumers who primarily shop offline and prefer miles to cashback would be a better match for Citi Rewards Card.

To view the best rewards credit cards available in Singapore, check over here for more!

Read Also:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.