DBS Black Visa Credit Card: The Best Shopping Card in Singapore?

DBS Black Visa Credit Card: The Best Shopping Card in Singapore?

ValueChampion Rating ![]()

Pros

- Great for earning miles for contactless spend

- Rewards on local shoppinh

- People who make big purchases & pay in instalments

Cons

- Limited online & overseas rewards

- Limited rewards categories

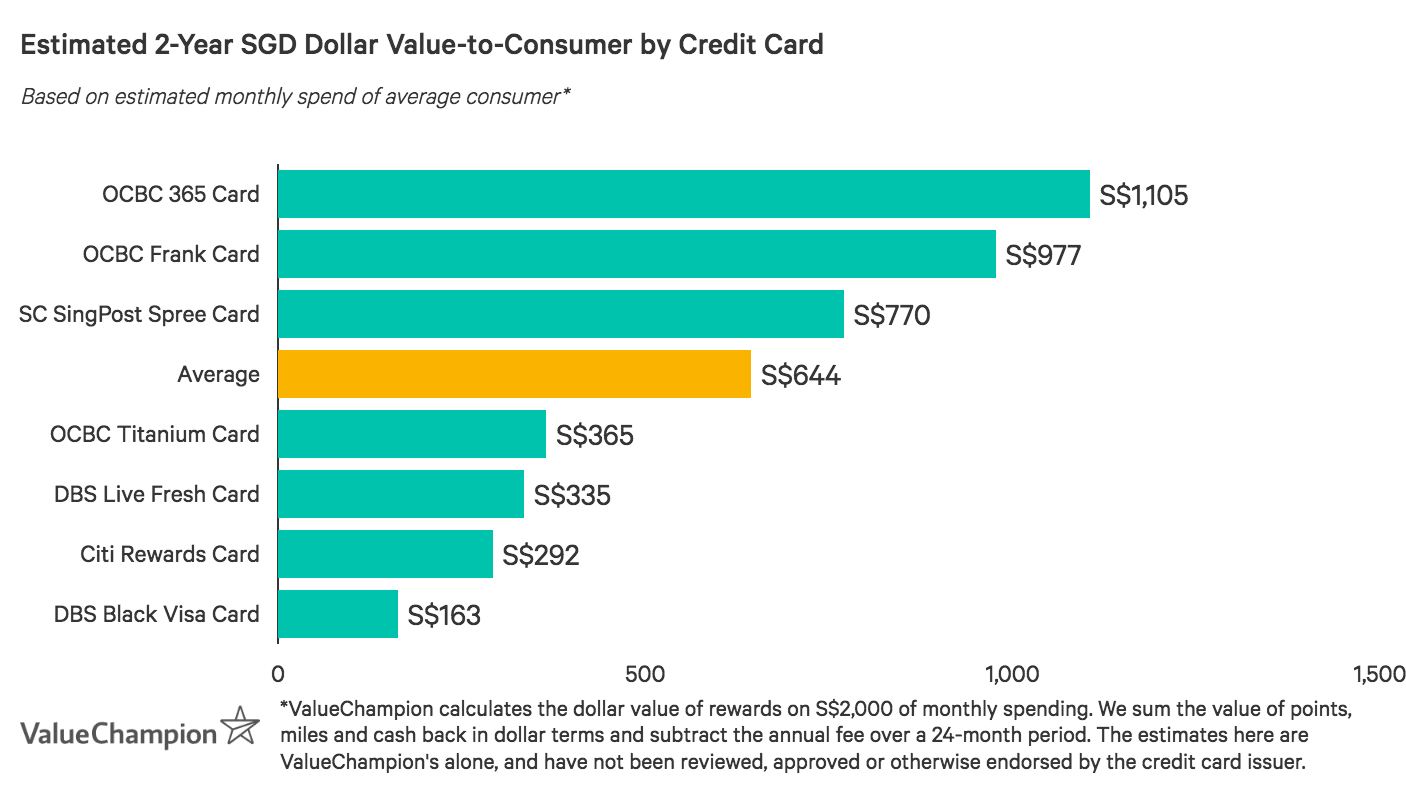

Local shoppers who prefer to pay in instalments and are comfortable with Visa payWave may be interested in DBS Black Visa Card. Cardholders earn extra miles from local purchases using a mobile wallet and receive discounts of up to 15% off select merchants. Those who make big purchases they'd prefer to pay off over time can enjoy the card's 0% interest instalment plan with no processing fee for over 6 months. However, this card's rewards are generally lower than other options while its S$192.6 annual fee is waived only the first year, reducing its ultimate value even further.

DBS Black Visa Credit Card Features and Benefits

|

|---|

Key Features:

|

What Makes DBS Black Visa Credit Card Stand Out

DBS Black Visa Card rewards local shoppers who like to pay over instalments and who are comfortable using contactless payment methods. Cardholders earn 1.2 miles per S$1 spend on local Visa payWave purchases (using Google Pay, Apple Pay, or Samsung Pay), which isn't great considering there are many cards that offer the same amount of miles for every local transaction. All other spend, including overseas, earn just 0.4 miles per S$1 spend.

The most stand-out feature is the card's 0% interest instalment plan with payments over 3, 6, or 12 months with no processing fee. Consumers can apply for the plan before making purchases of at least S$100 to avoid added costs during repayment. Purchases spread over 18 or 24 months are not eligible, however, and have a processing fee of 6% and interest rates of 7.86% and 5.98%, respectively. Otherwise, DBS Black Visa cardholders can easily pay back large purchases over time without added costs.

DBS Black Visa Card has drawbacks, however. Only a very limited range of expenditures qualify for the higher rewards rate, while most purchases–including all overseas transactions–can only earn 0.4 miles per S$1 spend. Most travel cards offer similar or significantly higher rewards rates for local and overseas spend, while some cashback cards offer higher cashback for online/mobile spend. DBS Black Visa Card also charges a S$192.6 annual fee, waived only the first year, detracting further from the card's value.

Consumers who aren't likely to use the 0% interest instalment plan might instead consider DBS Altitude Visa Card for better miles and travel perks, or OCBC Frank Card or OCBC 365 Card which reward mobile, online, and offline spend with high cashback rates.

How Does DBS Black Visa Credit Card's Rewards Program Work?

Use our quick and easy-to-read guide below to learn how you can redeem DBS Black Visa Card rewards.

- Spend rewarded in DBS Points (redeemable as rewards vouchers, instant-redemption at select merchants, miles, and as payment for annual fee)

- Cardholder can redeem points for KrisFlyer Miles or Asia Miles in blocks of 5,000 DBS Points for 10,000 air miles through DBS Rewards Frequent Flyer Programme. Administrative fee of S$26.75 applies for each miles redemption.

- Cardholder can automatically convert points to KrisFlyer Miles on the 10th day of each quarter (January, April, July and October) through DBS KrisFlyer Miles Auto Conversion Programme. Points are converted in blocks of 500 DBS Points for 1,000 KrisFlyer Miles. Administrative fee for miles redemption does not apply, but participants must pay an annual fee of S$42.8.

- DBS Points earned through DBS Black Visa Card expire one year from the quarterly period in which they were earned

DBS Black Visa Credit Card Rewards Exclusions

Some credit card expenditures are ineligible for cash back or rebate. We identify these exclusions in the table below.

How does DBS Black Visa Credit Card Compare Against Other Cards?

Read our comparisons of DBS Black Visa Card with other cards and learn what makes each card unique in their own way. We compare and contrast each card to highlight its uniqueness to help you identify the card that you need.

DBS Black Visa Card v. DBS Altitude Visa Card

- Pros

- Great for online travel bookings

- Cons

- Those willing to pay an annual fee for more bonus miles

- Affluent travellers who are willing to pay a high fee for luxury travel perks

Average spenders seeking miles and travel perks for both local and overseas spend, all with a no-fee card, might be interested in DBS Altitude Visa Card. Consumers receive 1.2 miles per S$1 local spend, 2 miles for overseas spend, and 3 miles for online travel spend–rates that greatly exceed those offered by DBS Black Visa Card for overseas and travel spend. While DBS Altitude Visa Card does not have an instalment plan, it offers perks like free airport lounge visits and travel insurance and has an easily waivable annual fee of S$192.6 (waived with each annual spend of S$25,000).

Consumers, in general, can earn more miles with DBS Altitude Visa Card while also enjoying travel perks and an easily waivable annual fee.

DBS Black Visa Card v. DBS Woman's World Card

- Pros

- 0% interest payment plans available

- Good rewards for online shopping

- Online purchase protection

- Cons

- Lacks travel perks

- Limited rewards categories

Shoppers who mostly spend online and who like to pay for purchases over instalments may benefit from DBS Woman's World Card. Unlike DBS Black Visa Card which rewards local mobile pay, this card rewards online shopping with 4 miles per S$1 spend. Both cards offer 0% interest instalment plans, but DBS Woman's World Card is essentially no fee–the S$192.6 cost is waived with each annual spend of S$25,000. Ultimately, DBS Woman's World Card is better for consumers who shop mostly online and prefer to avoid an annual fee, while DBS Black Visa Card caters to local spenders who make mobile payments.

DBS Black Visa Card v. OCBC Titanium Rewards Card

- Pros

- 10 pts (4 miles) per S$1 on fashion & select retail (Qoo10, Amazon, & more)

- Fee waiver with S$10,000 annual spend

- Cons

- 1 pt (0.4 miles) per S$1 other spend

- Earnings capped at 48,000 miles per year (worth S$480)

OCBC Titanium Rewards Card is great for shoppers who spend on fashion and want to avoid an annual fee. Cardholders receive 4 miles per S$1 spend on fashion retail and electronics online, offline, locally and overseas–a much higher rate than what DBS Black Visa cardholders can earn. And, while OCBC Titanium Rewards Card does not have an instalment plan, its S$192.6 fee is easily waived with each S$10,000 annual spend. OCBC Titanium Rewards Card is a great fit for avid fashion shoppers looking to avoid an annual fee.

DBS Black Visa Card v. Standard Chartered SingPost Spree Card

- Pros

- Great for monthly budgets below S$500

- Rewards overseas retailer shopping

- Cons

- Not suitable for monthly budgets of S$500+

- Lacks local shopping rewards

Online shoppers who spend and ship overseas can earn rewards from Standard Chartered SingPost Spree Card. Cardholders earn 2% on local and 3% on overseas online shopping, with another 3% cashback for vPost transactions. Even though there's a S$60/month cap, overall earning potential is much higher than with DBS Black Visa Card, which earns an equivalent of 1.2% for local mobile pay and 0.4% for general spend. SC SingPost Spree Card is better for transport as it offers 15% cashback on Grab rides, and can provide more value to shoppers than DBS Black Visa Card overall.

DBS Black Visa Card v. Citi Rewards Card

- Pros

- Great for online & offline shopping

- Beneficial for frequent travellers

- Cons

- Less valuable for infrequent shoppers

- Foreign transaction fees apply

Citi Rewards Card is a great miles-earning card for consumers who frequently shop fashion retail online, offline, locally and overseas. Cardholders earn 4 miles per S$1 spend wherever they purchase shoes, clothes, bags, or other accessories, which is nearly 4x higher than the shopping rate offered by DBS Black Visa Card. While Citi Rewards Card does not offer a 0% interest instalment plan, it does include overseas spending in its rewards rate whereas DBS Black Visa Card does not.

While DBS Black Visa Card's instalment plan may be a plus, consumers who rarely defer payments can better maximise rewards from fashion retail spend with Citi Rewards Card.

Read Also:

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.